Due Diligence Report (2026): 8-Section IC Template + RAG Scoring

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

Due Diligence Report (2026): 8-Section IC Template + RAG Scoring

By Deqian Jia, co-founder of Peony · Last updated May 2026

I'm Deqian Jia, co-founder of Peony — a virtual data room platform used by 6,800+ customers. I sit downstream of an absurd number of due diligence reports every quarter. Buy-side associates pulling all-nighters before Monday IC. PE VPs trying to translate 14 workstream memos into one 32-page synthesis their partner can defend to LPs. M&A counsel reviewing the Conditions section against the negotiated SPA. R&W underwriters reading the Risk Register to price the policy retention.

The question that defines this work in 2026: what structure makes a due diligence report defensible to the investment committee, the R&W underwriter, and the post-close litigation discovery — all three at once?

Quick answer: A due diligence report is the synthesis document the investment committee, board, lender, and R&W insurer rely on to make the proceed-or-walk decision. The 8-Section IC-Ready DD Report Template covers Executive Summary, Strategic Rationale, Financial Findings, Commercial Findings, Operational Findings, Legal/Regulatory/IP Findings, Risk Register, and Conditions plus R&W. Each section gets a Weighted RAG Scoring (Financial 25%, Commercial 20%, Operational 15%, Legal/Reg/IP 10%, Risk Register 10%, Executive Summary 10%, Strategic Rationale 5%, Conditions/R&W 5%). The weighted sum drops into the 4-Outcome Decision Tree — Pass (above 70 + no red sections), Pass-with-conditions (60-70), Repricing-required (50-60), Walk (under 50 or red core section). Anchor references: ABA 2025 Private Target Deal Points Study (RWI on 63% of deals, reps non-survival on 41%), SRS Acquiom 2026 M&A Deal Terms Study (escrow sizes rising; No Undisclosed Liabilities claims surging), and the Edwards v. GigAcquisitions2 (July 25, 2025) Chancery decision that doubled down on diligence as the fraud-statute-of-limitations gate.

This post is the DD Report anchor — the report artifact, not the question artifact (see the due diligence questionnaire guide) and not the file inventory (see the 174-document M&A DD checklist).

TL;DR — three proprietary frames anchor this post:

- Frame A — the 8-Section IC-Ready DD Report Template. Executive Summary, Strategic Rationale, Financial, Commercial, Operational, Legal/Reg/IP, Risk Register, Conditions/R&W. Each section has a target page count, an owner, and a fixed scoring weight.

- Frame B — Weighted RAG Scoring. Each section weighted (Financial 25% / Commercial 20% / Operational 15% / Legal-Reg-IP 10% / Risk Register 10% / Executive Summary 10% / Strategic Rationale 5% / Conditions-R&W 5%); RAG-scored 0-100; weighted sum drops into the decision tree.

- Frame C — the 4-Outcome Decision Tree. Pass / Pass-with-conditions / Repricing-required / Walk. Asymmetric: a single red core section vetoes a high total.

Anchor data: ABA 2025 Deal Points Study (RWI 63%, reps non-survival 41%), Marsh R&W premium update Spring 2025 (rates +16% YoY North America, retentions as low as 0.5% EV), SRS Acquiom 2026 Deal Terms Study (2,300+ deals, $569B aggregate), Bain Global PE Report 2026 (inflated seller expectations and DD red flags named the two most common 2025 deal-killers). The HSR threshold is $133.9M for 2026 (FTC).

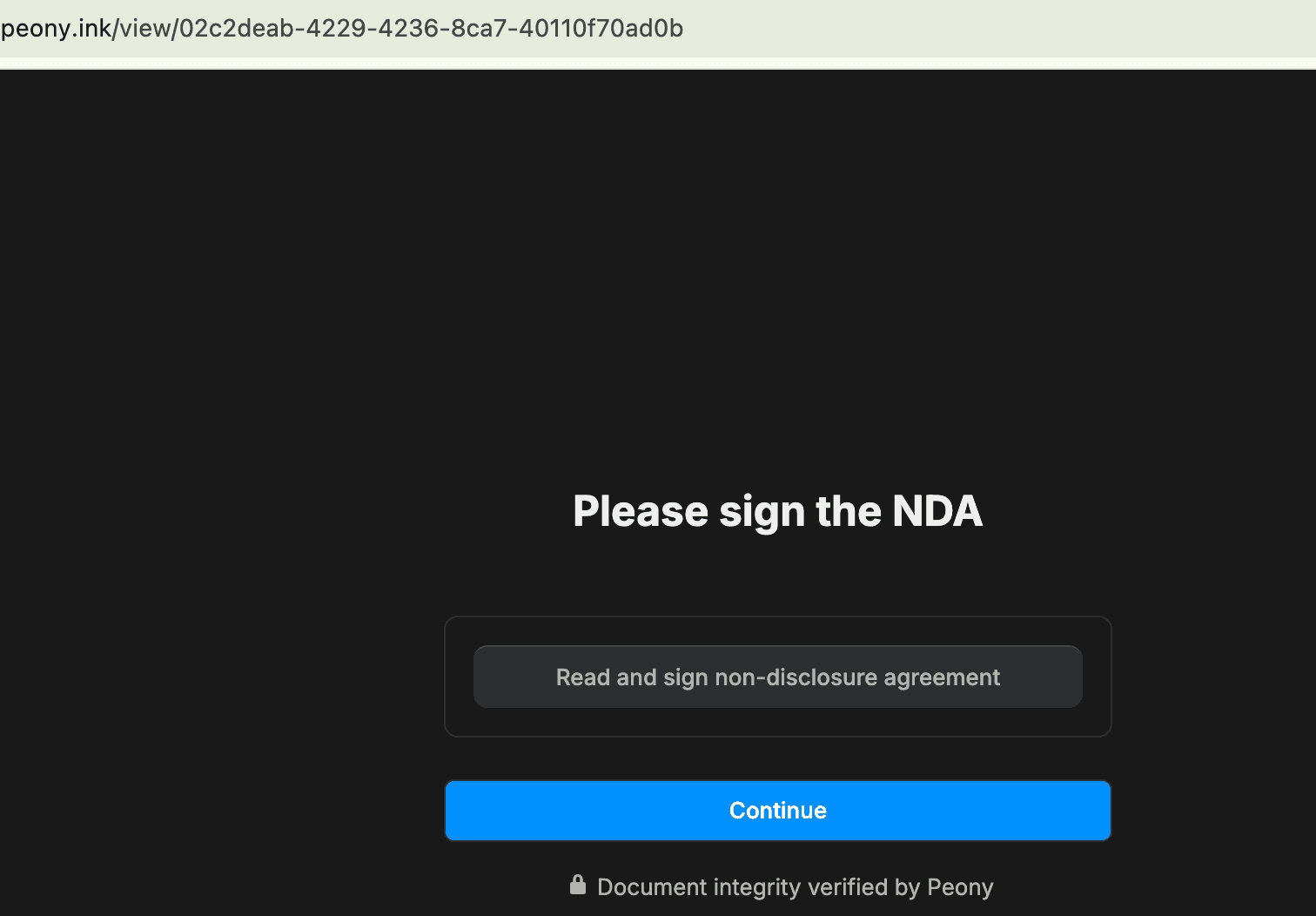

The Peony spine: NDA gates before report-relevant data room sections open, visitor groups so the report drafter, the IC counsel, and the R&W underwriter each see their own view of the data room, page-level analytics tracking which target documents each reviewer actually opened, dynamic watermarks on every page the report cites, and auto-indexing catalogs the data room into the 8-section taxonomy that the report mirrors. Peony Data Room at $52/admin/month handles the full DD-report drafting cycle — visitor groups, auto-indexing, and unlimited rooms — without per-page or per-storage upcharges.

What is a due diligence report and who reads it?

A due diligence report is the written synthesis of every diligence workstream that the investment committee, deal partner, board, lender, and R&W insurer rely on to make the proceed-or-walk decision. It is distinct from a due diligence questionnaire (the question artifact issued to the seller) and from a DD checklist (the document inventory the seller assembles). The report is the analytical artifact: it takes the QofE memo, the commercial study, the operational findings, the legal red flags, the IP register, the regulatory map, and the IT diligence, and binds them into a single 30-to-80 page document with a recommendation. Readers are the investment committee (PE), the corporate development executive committee or board (strategic), the LP advisory committee (continuation funds), the syndication bank (LBO debt), and the R&W insurance underwriter pricing the policy. In 2026 the report is also where post-close litigation discovery starts — the Edwards v. GigAcquisitions2 (July 25, 2025) Delaware Chancery decision dismissed fraud claims in part because the court judged the buyer's diligence process limited, refusing to toll the fraud statute of limitations.

Readers in order of consequence:

| Reader | What they read first | What they decide |

|---|---|---|

| Investment committee (PE) | Executive Summary + recommendation | Approve / reject capital deployment |

| Deal partner (PE) | Risk Register + Conditions | Sign the IC memo |

| Board / CEO (strategic) | Strategic Rationale + Financial | Approve TEV and structure |

| Syndication bank (LBO debt) | Financial + Risk Register | Underwrite the bank book |

| R&W underwriter | Conditions/R&W + Risk Register | Price policy retention + premium |

| LP advisory committee (CV) | Strategic Rationale + fairness opinion | Vote on CV terms |

| Post-close litigation discovery | All sections — especially Risk Register and what it omits | Whether to grant or refuse statute-of-limitations tolling |

The last reader is the one most deal teams underestimate. The Edwards v. GigAcquisitions2 (Delaware Chancery, July 25, 2025) decision dismissed Cloudbreak's fraud-induced-de-SPAC claims in part because the court judged the buyer's diligence process limited and refused to toll the fraud statute of limitations. The court's reasoning: a party that runs limited diligence cannot later argue it could not have discovered the fraud earlier. In 2026 the DD report is the single most important defensive artifact a buyer has when something surfaces post-close.

Which 8 sections must every IC-ready DD report contain?

The 8-Section IC-Ready DD Report Template covers: (1) Executive Summary plus Recommendation, (2) Deal Strategic Rationale, (3) Financial Findings (QoE, working capital, debt-like items), (4) Commercial Findings (market, TAM, NRR, customer concentration), (5) Operational Findings (mapped to the 8-System ODD audit summary, with cross-link), (6) Legal, Regulatory, and IP Findings, (7) Risk Register (top 10 with severity scores), and (8) Conditions plus Recommended Reps & Warranties. The taxonomy maps 1:1 to how the investment committee, R&W insurer, and post-close litigation discovery will navigate the document. Every section gets a Weighted RAG score, and every section drops into the 4-Outcome Decision Tree. Skipping a section is a V1-veto-grade quality miss because the IC will ask the question anyway and your analyst will improvise the answer in the room.

Section breakdown with target page count and ownership:

| # | Section | Target pages | Owner | Weight | Typical 0-100 score range |

|---|---|---|---|---|---|

| 1 | Executive Summary + Recommendation | 1.5-2 | Deal lead (PE: VP+) | 10% | 60-95 |

| 2 | Strategic Rationale | 1-2 | Deal lead / corp dev head | 5% | 50-95 |

| 3 | Financial Findings (QoE, NWC, debt-like) | 5-12 | Financial DD lead | 25% | 40-90 |

| 4 | Commercial Findings (market, TAM, NRR, concentration) | 4-8 | Commercial DD lead | 20% | 35-90 |

| 5 | Operational Findings (8-System ODD summary) | 3-6 | ODD lead | 15% | 40-85 |

| 6 | Legal / Regulatory / IP Findings | 3-8 | M&A counsel | 10% | 40-90 |

| 7 | Risk Register (top 10) | 2-4 | Deal lead, signed by counsel | 10% | 30-80 |

| 8 | Conditions + Recommended R&W | 2-4 | M&A counsel | 5% | 60-95 |

The 8-Section IC-Ready DD Report Template is not an arbitrary list. The weights reflect the empirical pattern across mid-market private deals: financial and commercial findings drive ~45% of the score because the IC questions concentrate there, operational and legal/IP split the next ~25%, and the synthesis sections (Executive Summary, Strategic Rationale, Risk Register, Conditions) split the remaining ~30%. Skipping a section is a V1-veto-grade quality miss — the IC asks the question regardless, and the analyst improvises in the room.

For the operational section, the 8-System ODD Audit framework is the source taxonomy. For the AI-specific overlay, the 5-Layer AI Target Audit populates Sections 5, 6, and 7. For the question-side artifact that drives the report's findings, the due diligence questionnaire guide covers the 5-Persona DDQ Template Library.

How do you score sections with the Weighted RAG framework?

The Weighted RAG Scoring framework assigns each of the 8 sections a fixed weight, scores each section 0-100, and produces a single weighted-sum score that drops into the 4-Outcome Decision Tree. The exact weights: Executive Summary 10%, Strategic Rationale 5%, Financial 25%, Commercial 20%, Operational 15%, Legal/Regulatory/IP 10%, Risk Register 10%, Conditions plus R&W 5% (total 100%). Section scoring bands: 70-100 Green (no material issues), 50-69 Amber (issues identified, mitigable), 0-49 Red (deal-killer category absent mitigation). The weighted sum produces an overall score in the same 0-100 band: 70-100 Green proceed, 50-69 Amber proceed-with-conditions or repricing, 0-49 Red walk. This exact weighted-RAG formula is not findable on Google — it is the spine of how we structure IC-ready synthesis across the deals we sit downstream of, and it makes the 30-page report defensible because every paragraph rolls up to a single number the IC can debate.

The Weighted RAG Scoring works because every section is on the same axis. A Financial section at 75 (Amber-to-Green) contributes 75 × 25% = 18.75 weighted points. A Legal section at 45 (Red) contributes 45 × 10% = 4.5 weighted points but also veto-triggers the 4-Outcome Decision Tree's red-core rule.

Worked example — hypothetical $200M SaaS target across all 8 sections:

| Section | Weight | Section finding | Score (0-100) | Weighted contribution |

|---|---|---|---|---|

| Executive Summary | 10% | Clean recommendation drafted | 80 | 8.0 |

| Strategic Rationale | 5% | Buy-and-build thesis, anchor add-on | 85 | 4.25 |

| Financial | 25% | QoE adj: $1.8M EBITDA reversal (ASC 606) | 65 | 16.25 |

| Commercial | 20% | NRR 118%, top customer 22% of ARR | 70 | 14.0 |

| Operational | 15% | ODD score 18/25 (clean) | 78 | 11.7 |

| Legal/Reg/IP | 10% | Contractor IP gap, ~8% of code base | 42 | 4.2 |

| Risk Register | 10% | 3 items above remediation band | 60 | 6.0 |

| Conditions/R&W | 5% | $4M special indemnity + 1% retention RWI | 75 | 3.75 |

| Total | 100% | 68.15 |

The weighted total of 68.15 lands in Amber (Pass-with-conditions). But the Legal/Reg/IP score of 42 is Red. Because IP is a core category, the 4-Outcome Decision Tree veto rule triggers: the deal does not Pass-with-conditions; it routes to Repricing-required with the IP cure as the explicit repricing trigger. The report's Section 8 Conditions then names the contractor IP assignment as the closing condition with a $3-5M repricing math.

The Weighted RAG Scoring removes the classic IC failure mode where an analyst stitches a narrative around a buried red flag. The number on the page either passes the threshold or doesn't, and the asymmetric red-veto in the decision tree catches the cases where it shouldn't pass even when the number passes.

How does the 4-Outcome Decision Tree work?

The 4-Outcome Decision Tree converts the Weighted RAG Scoring output into one of four explicit deal actions. Outcome 1 — Pass: weighted score above 70 AND no red sections in any core financial, commercial, or legal category. Outcome 2 — Pass-with-conditions: weighted score 60-70 AND specific conditions identified (e.g., escrow above standard, key-person retention, regulatory consent). Outcome 3 — Repricing-required: weighted score 50-60 AND the repricing math is calculable (typically 5-15% equity reduction or 10-30% TEV haircut). Outcome 4 — Walk: weighted score below 50 OR any red section in financial, commercial, or legal core categories regardless of weighted total. The asymmetric structure (a single red core section vetoes a high total) prevents the classic IC failure mode where a high-scoring report with a buried red flag in IP assignment or revenue recognition still passes because the rest of the report looks clean.

The exact thresholds:

| Outcome | Weighted score | Section conditions | What the report concludes |

|---|---|---|---|

| Pass | >70 | No red sections in Financial, Commercial, or Legal/Reg/IP | Recommendation to proceed; SPA per term sheet |

| Pass-with-conditions | 60-70 | Conditions identified; no red core | Proceed with named closing conditions (escrow above standard, key-person retention, regulatory consent) |

| Repricing-required | 50-60 OR red core section with mitigable cure | Repricing math calculable | Proceed with repricing (typically 5-15% equity reduction or 10-30% TEV haircut) |

| Walk | Under 50 OR any red section in Financial, Commercial, or Legal core | No calculable cure | Recommend walk; preserve relationship for re-engagement |

The asymmetric veto matters. A target can score 73 weighted (above the Pass threshold) but have a Legal/Reg/IP section at 42 (Red) — and the 4-Outcome Decision Tree routes it to Repricing-required, not Pass. The veto rule prevents the classic discovery hazard where a high overall score masks a category-specific deal-killer.

The 4-Outcome Decision Tree pairs with each section as follows:

- Financial Red (below 50): revenue recognition dispute, QoE adjustment > 15% of stated EBITDA, working-capital gap > 5% of TEV, debt-like items not in disclosure schedule. Walk or Repricing.

- Commercial Red: top customer above 30% of revenue (the classic mid-market deal-killer the DDQ guide flags); NRR below 90%; churn gradient negative for 3+ quarters.

- Legal/Reg/IP Red: IP assignment chain gaps for contractor code, undisclosed litigation, HSR second request expected with > 60-day delay, CFIUS mandatory filing not previously scoped.

The Bain Global Private Equity Report 2026 names inflated seller expectations and diligence red flags (poor earnings quality, customer churn, etc.) as the two most common 2025 deal-killers — both Financial and Commercial in our taxonomy. The 4-Outcome Decision Tree treats them as veto categories explicitly.

How do you write the IC-ready executive summary in under 2 pages?

The executive summary is the most-read and least-written section of the 8-Section IC-Ready DD Report Template. It must be under 2 pages, must lead with the Weighted RAG Scoring overall score and the 4-Outcome Decision Tree recommendation, and must end with the top 3 risks plus the top 3 mitigants. Specifically: paragraph 1 names the target, deal size, hold strategy, and the explicit recommendation (Pass, Pass-with-conditions, Repricing-required, or Walk) with the weighted score. Paragraph 2 names the strategic rationale in one sentence and the unit economics in three numbers (revenue, EBITDA margin, growth rate). Paragraph 3 names the top 3 findings driving the recommendation. Paragraph 4 names the top 3 risks and the mitigants. The IC will read this in 90 seconds and decide whether to read further. If the executive summary cannot stand on its own as the decision artifact, the report has failed its primary job.

The four-paragraph spine I use:

- Paragraph 1 (recommendation): Name the target, deal size, hold strategy, and the explicit recommendation (Pass / Pass-with-conditions / Repricing-required / Walk) with the weighted score. Example: "Recommendation: Pass-with-conditions. Target: Pinetree SaaS Inc., $200M TEV, buy-and-build platform. Weighted DD score: 68.15. Conditions: contractor IP cure, top-customer retention term."

- Paragraph 2 (unit economics): Strategic rationale in one sentence; revenue, EBITDA margin, growth rate in three numbers. Example: "Buy-and-build anchor for the workflow-software vertical. $48M ARR, 27% EBITDA margin, 22% YoY growth, 118% NRR."

- Paragraph 3 (top 3 findings): The three findings driving the recommendation. Each one cites the source section.

- Paragraph 4 (top 3 risks + mitigants): From the Risk Register. Each risk paired with a mitigant or a Conditions/R&W line.

The IC reads this in 90 seconds. If they read further, they ask three questions in the meeting:

- What's the weighted score, and what's the lowest section score?

- What does the Risk Register say about post-close exposure?

- What's in Section 8 Conditions?

A well-written executive summary answers all three questions in the first half-page. Per the ABA 2025 Private Target Deal Points Study, 63% of deals reference RWI (up from 55%), which means the executive summary in 2026 also lands on the R&W underwriter's desk — the second reader after the IC. Write the executive summary as if the R&W underwriter is reading it cold, because they often are.

What goes in the Risk Register and how do you score severity?

The Risk Register is Section 7 of the 8-Section IC-Ready DD Report Template and is the single most-cited section in post-close litigation discovery. It lists the top 10 risks with three scores each: likelihood (1-5), impact in dollar terms (low / medium / high / extreme), and remediability (the inverse of how fixable the finding is in 12 months). Each risk maps to a specific source section finding, an owner for post-close monitoring, and a mitigation status (open / mitigated / accepted). The top 10 are surfaced from the section scoring — any finding that took a section to Amber or Red appears in the Risk Register. Per SRS Acquiom's 2026 M&A Deal Terms Study analyzing 2,300+ private-target acquisitions valued at $569 billion, claims for breach of the No Undisclosed Liabilities representation are way up, which means the Risk Register is the most legally consequential section in the entire report.

The Risk Register row anatomy:

| Risk | Source section | Likelihood (1-5) | Impact $ | Remediability (1-5) | Owner | Status | Mitigant |

|---|---|---|---|---|---|---|---|

| Top-customer renewal at 22% of ARR | Commercial | 3 | High ($8-12M ARR exposure) | 3 | VP Sales | Open | Pre-close retention call + change-of-control waiver |

| Contractor IP assignment gap | Legal/IP | 5 | High ($3-5M cure) | 4 | GC | Open | Pre-close contractor sign-offs + escrow holdback |

| QoE adj: $1.8M reversal (ASC 606) | Financial | 4 | Medium ($1.8M EBITDA) | 2 | CFO | Mitigated | Working-capital peg adjusts |

| Key-person dependency (CTO) | Operational | 3 | High (12-month re-hire) | 4 | CEO | Open | Retention bonus + 24-month non-compete |

The Risk Register is what the R&W underwriter reads first — it tells them what known risks have been carved out of the policy, what unknown risks the policy will need to cover, and what retention level to price. The 2025-2026 R&W market saw premiums rise ~16% year-over-year in North America per Marsh and WTW, with rates at 2.5-3% of policy limit and retentions as low as 0.5% of EV. A well-built Risk Register is what gets a deal team to the lower retention band.

The Risk Register is also what post-close litigation discovery reads first. Per SRS Acquiom's 2026 Deal Terms Study analyzing 2,300+ deals valued at $569B, claims for breach of the No Undisclosed Liabilities representation are way up. Every risk that should have been on the register and wasn't becomes evidence in indemnification discovery. The Bain Capital / PowerSchool ruling (US District Court, March 18, 2026) — where the court allowed plaintiffs' claims to proceed based on conduct before Bain's October 2024 acquisition — turned in part on what was and wasn't documented in pre-close cybersecurity diligence.

The Risk Register threshold I use: any finding scored above 12 on the 3-Axis ODD Severity Matrix (likelihood × impact × remediability ÷ 5) goes on the Risk Register. Any finding above 18 goes to the top of the Risk Register and requires either a special indemnity outside the R&W policy or a separate escrow line in Section 8 Conditions.

What DD report mistakes triggered post-close litigation 2024-2026?

Six DD report failure modes drove post-close litigation 2024-2026. (1) Limited-scope diligence — Edwards v. GigAcquisitions2 (Delaware Chancery, July 25, 2025) dismissed fraud-induced-de-SPAC claims in part because the court judged Cloudbreak's diligence process limited, refusing to toll the fraud statute of limitations. (2) Pre-close operational control liability — the Bain Capital / PowerSchool ruling (US District Court, March 18, 2026) allowed plaintiffs' claims to proceed based on conduct before Bain's October 2024 acquisition close, including Bain's pre-close veto rights over capital expenditures above $5M and cybersecurity layoffs. (3) Customer-concentration under-disclosure — the recurring 2025-2026 mid-market failure mode where sellers omit a top-customer share above 30% and the buyer surfaces it weeks later. (4) IP assignment gaps for contractor-built code — the surviving cause of action in startup acquisitions. (5) Inflated seller QofE add-backs not flagged in financial findings — Bain's 2026 Global Private Equity Report names inflated seller expectations as one of the two most common deal-killers. (6) Reps-and-warranties survival gaps — per the ABA 2025 Private Target Deal Points Study, 41% of deals now have reps not surviving closing (up from 30%), making the Conditions/R&W section in the report the single most consequential drafting decision. RWI was used on 63% of deals in the 2025 study (up from 55% in 2023).

The six failure modes mapped to the 8-Section IC-Ready DD Report Template:

1. Limited-scope diligence — Edwards v. GigAcquisitions2 (July 25, 2025). The Delaware Court of Chancery dismissed Cloudbreak's fraud-induced-de-SPAC claims in part because the court judged the diligence process limited and refused to toll the fraud statute of limitations. The lesson: a thinly-scoped report is a forfeit of the discovery-rule defense. Every section of the 8-Section IC-Ready DD Report Template should record what was investigated and what was deliberately scoped out.

2. Pre-close operational control liability — Bain Capital / PowerSchool (March 18, 2026). The US District Court allowed plaintiffs' claims to proceed based on conduct before Bain's October 2024 acquisition close. Bain held pre-close veto rights over capital expenditures above $5M and required cybersecurity layoffs as a closing condition. The "disclaimer of control" clause in the acquisition agreement did not insulate Bain from cybersecurity liability. The lesson: pre-close operational control creates pre-close liability, and the DD report's Operational Findings section must capture cybersecurity layoffs or staffing reductions as a documented buyer-driven decision.

3. Customer-concentration under-disclosure. The recurring 2025-2026 mid-market failure mode where the seller omits a top-customer share above 30% from the initial DDQ response and the buyer surfaces it weeks later in commercial DD. Deal failure rates spike and valuation compression of 15-30% becomes standard. The Commercial Findings section of the DD report is where the buyer documents the gap — and where post-close litigation begins if the report was wrong.

4. IP assignment gaps for contractor-built code. The most common surviving cause of action in startup acquisitions per indemnification claims data. Contractor work-for-hire chains that aren't documented become breach-of-warranty claims under the IP rep. The Legal/IP section of the report must flag this explicitly, and the Conditions section must name the contractor sign-off as a closing condition or escrow holdback. For the IP-specific deep dive see the IP due diligence guide.

5. Inflated seller QofE add-backs not flagged. The Bain Global Private Equity Report 2026 names inflated seller expectations as one of the two most common 2025 deal-killers. The Financial Findings section of the DD report must reconcile every seller add-back to GAAP and ASC 606 — silent acceptance is evidence of negligence in post-close indemnification discovery.

6. Reps-and-warranties survival gaps. Per the ABA 2025 Private Target Deal Points Study, 41% of deals now have reps not surviving closing (up from 30% in the prior study). RWI was used on 63% of deals (up from 55%). The Conditions/R&W section of the report is the single most consequential drafting decision in the document — the survival period, the materiality scrape, and the indemnification cap all depend on how Section 8 reads.

The Weighted RAG Scoring would have caught five of these six (Edwards, customer concentration, IP gaps, QoE add-backs, R&W survival) at Amber or Red in the relevant section. The PowerSchool case is the harder one — pre-close operational control is a structural issue the DD report itself doesn't typically score, but the Risk Register can flag "buyer pre-close operational decisions create pre-close liability exposure" as a deal-team red flag.

How does the DD report feed the SPA reps and escrow design?

The DD report feeds the SPA reps and escrow design through Section 8 of the 8-Section IC-Ready DD Report Template, which translates findings into recommended representations, indemnification carve-outs, and escrow size. Specific mechanics: every Risk Register item scored above 12 (the deal-stopper band) requires either a special indemnity outside the R&W policy or an escrow line item; every Amber-scored section translates into a rep-and-warranty with a tighter materiality scrape or a longer survival period; the Conditions section names the closing conditions, the working-capital peg, and the carve-outs for known liabilities. Per the SRS Acquiom 2026 Deal Terms Study, escrow size (median and average) increased from 2024 to 2025 across nearly all deal categories, and RWI was identified on approximately 46% of deals. R&W insurance premiums rose ~16% year-over-year in North America in 2025 per Marsh, with rates at approximately 2.5-3% of policy limit and retentions as low as 0.5% of enterprise value. The report's Conditions section is what the R&W underwriter reads first.

Section 8 has four sub-sections:

- 8a. Closing conditions. Specific to the deal — top-customer retention waiver, key-person retention, regulatory consent (HSR, CFIUS, FCC, state insurance), third-party assignment consents, contractor IP sign-offs, audit opinion delivery, MAC walk-rights.

- 8b. Recommended representations. Targeted reps that respond to specific risks in the Risk Register. Examples: IP assignment rep with a 36-month survival, no-undisclosed-liabilities rep with a $100K basket, cyber rep with a fundamental classification.

- 8c. Indemnification structure. Cap (typically 10-15% of TEV for non-fundamental; 100% for fundamentals), basket (typically 0.5-1.0% TEV), de minimis (typically $25-50K), survival periods, special indemnities outside the R&W policy.

- 8d. Recommended R&W policy. Limit (typically 10-15% of TEV), retention (~0.5-1% of EV per Marsh 2025), premium budget (2.5-3% of policy limit), known-issue exclusions, special-indemnity carve-outs.

The mechanics per the SRS Acquiom 2026 Deal Terms Study (2,300+ deals, $569B aggregate):

- Escrow size (median and average) increased from 2024 to 2025 across nearly all deal categories.

- RWI was identified on ~46% of deals in the SRS Acquiom Study (up from prior years).

- Claims for breach of the No Undisclosed Liabilities representation are way up — a direct read on how often the DD report's Financial and Legal sections missed something.

The R&W market mechanics in 2025-2026 per Marsh and WTW:

- North America primary R&W premium rates rose ~16% YoY in 2025 (reversing the 14% decline in 2024)

- Asia premium rates rose 8% YoY (vs. 24% average decline in 2024)

- Rates: ~2.5-3% of policy limit (down from ~5% in early 2022)

- Retentions: as low as 0.5% of EV (down from historical 1%) on early-2025 deals

- Claims frequency and severity rose globally in 2025; UK hit historic notification levels

The clearest reading: the R&W market has firmed, but the underwriters are still competing on rate and retention if the DD report's Risk Register is well-built. A weak Section 7 (Risk Register) and Section 8 (Conditions/R&W) costs the buyer 50-100 bps on premium and 25-50 bps on retention.

How should you stage DD report drafting against the data room timeline?

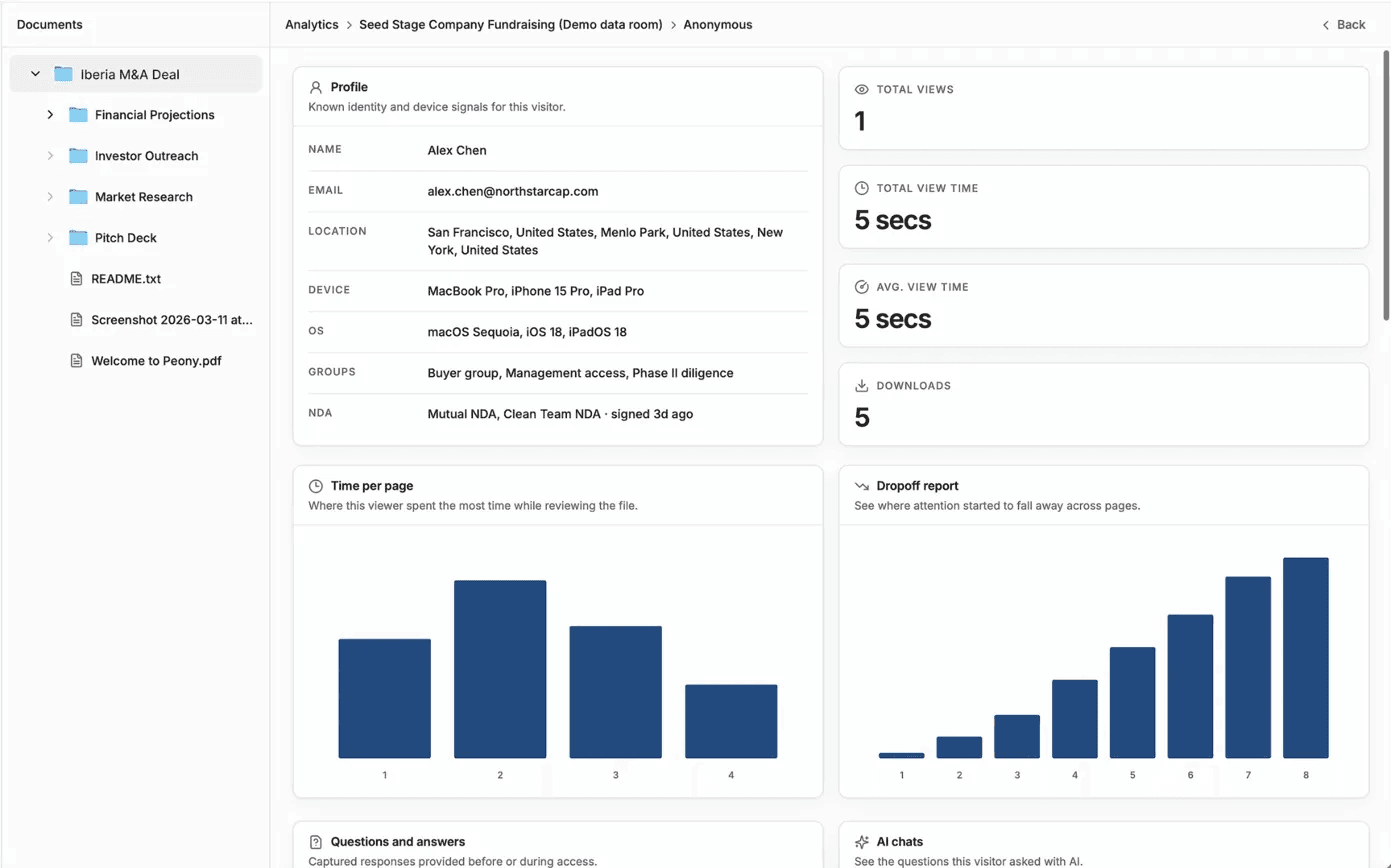

Drafting the DD report against the data room timeline maps to four stages of access: Stage 1 (teaser / CIM, weeks 0-2) — the report scaffold is created with executive summary placeholder, strategic rationale, and known-public findings. Stage 2 (Round 1 NDA-gated, weeks 2-6) — financial QofE preliminary findings, commercial market scan, and legal red flags populate Sections 3, 4, and 6; Risk Register starts. Stage 3 (Round 2 final-bidder, weeks 6-12) — operational findings (Section 5), full QofE, IP register, customer reference calls, and IT deep dive populate; Section 7 Risk Register reaches top 10; Section 8 begins drafting. Stage 4 (confirmatory plus SPA, weeks 12-16) — every section reaches final score, executive summary is rewritten, recommendation locks. The Peony spine: NDA gates control which sections of the data room open at each stage, visitor groups isolate workstream-specific reviewers (financial vs commercial vs operational), and page-level analytics show which target documents each reviewer actually opened — the engagement signal that tells the report drafter where to weight the report.

The four stages mapped to the data room:

| Stage | Weeks | Data room access | Report drafting state |

|---|---|---|---|

| Stage 1 — Teaser / CIM | 0-2 | Public teaser; NDA-gated CIM | Scaffold + executive summary placeholder + strategic rationale |

| Stage 2 — Round 1 NDA | 2-6 | Tier 1 docs (overview, historical financials, redacted contracts) | Financial Findings draft 1; Commercial scan; Legal red flags; Risk Register starts |

| Stage 3 — Round 2 final bidder | 6-12 | Tier 2 docs (full financials, customer schedules, IP register, audited reports) | All 8 sections populated; Risk Register reaches top 10; Conditions drafting begins |

| Stage 4 — Confirmatory + SPA | 12-16 | Tier 3 docs (sensitive schedules, employee-level, side letters) | Executive summary rewritten; recommendation locks; Conditions finalized |

The Peony product spine that carries the drafter through these stages:

- NDA gates — Section-relevant data room folders open only after the bidder signs the NDA matching the access tier

- Programmatic visitor groups — the financial DD lead, the operational DD lead, the IP counsel, and the R&W underwriter each see their own view of the data room without the seller managing duplicate folders

- Page-level analytics — the seller's advisor sees which target documents each reviewer actually opened, which is the leading indicator of which findings are about to surface in the buyer's report

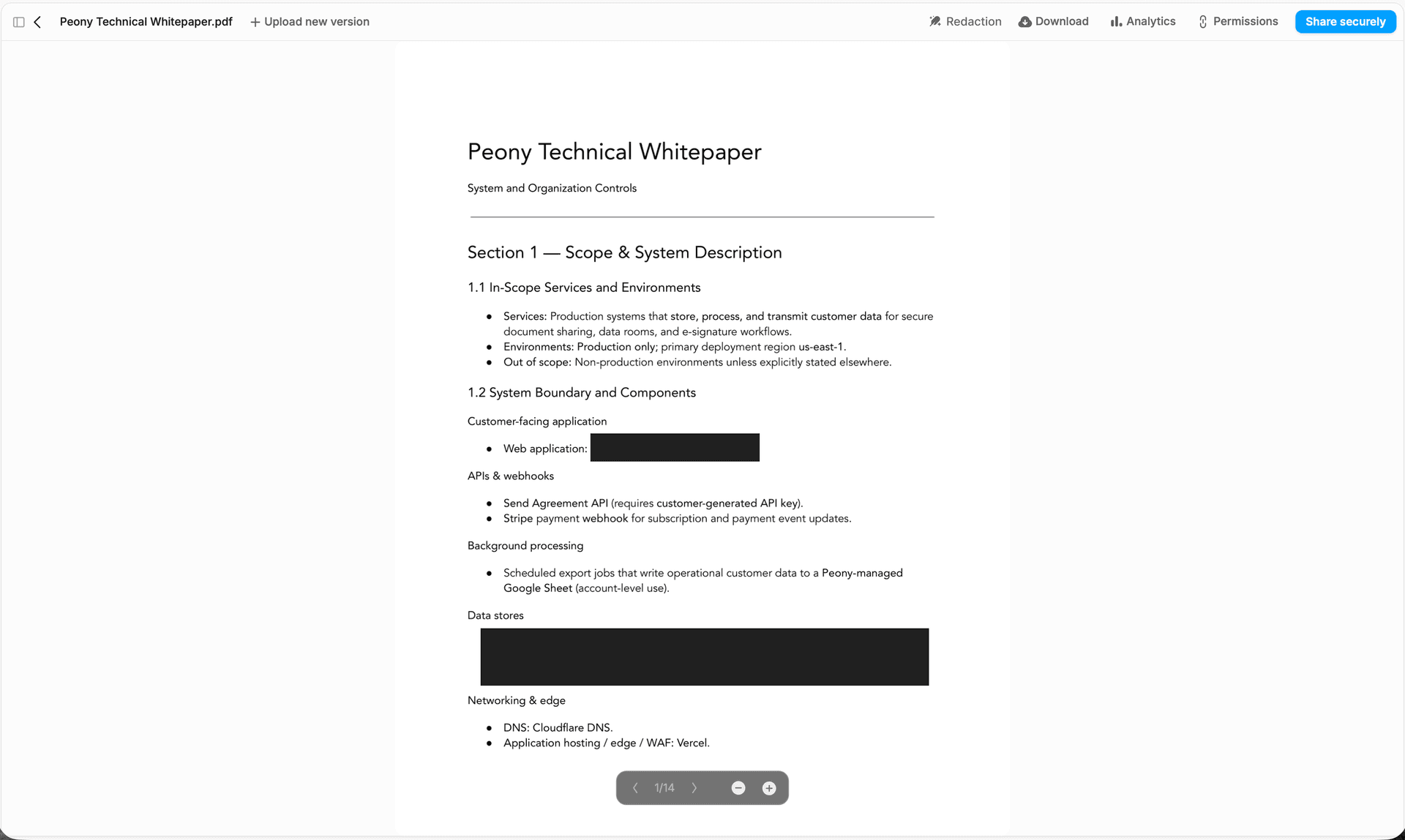

- Dynamic watermarks — every document the report cites carries a per-reviewer watermark; leaked excerpts trace to the leak source

- Screenshot protection — blocks system-level capture on sensitive schedules in Stage 4

- Auto-indexing — the data room catalogs into the 8-section taxonomy the report mirrors; the financial folder maps to Section 3, the commercial folder to Section 4, the operational folder to Section 5

- Smart Q&A — every Q&A round routes through a 4-step approval workflow; the responses become evidence cited in the report's section findings

- Manage links — the deal team shares Section 8 R&W exhibits with the underwriter via expiring links; revocation is one click if the carrier swaps

- AI extraction — clause-extraction pulls customer change-of-control, IP assignment, and MFN clauses across hundreds of contracts in minutes, populating the Commercial and Legal sections directly

Peony Data Room at $52/admin/month carries the full 12-16 week DD cycle, with unlimited rooms, auto-indexing, and visitor-group isolation. Per-admin pricing means a $200M deal and a $50M deal cost the same on the data room axis — the advisor at the sell-side runs both rooms on the same plan. Pricing is flat at $52/admin/month regardless of storage or page count.

For the seller-side document inventory that lands in the data room and answers the buyer's DD report sections, see the 174-document M&A DD checklist. For the AI-using-target overlay that adds five layers to Sections 5, 6, and 7, see the AI due diligence guide. For the PE hold-strategy-conditional weighting that adjusts the 8-Section weights by deal type, see the private equity due diligence playbook. For the operational engine that populates Section 5 directly, see the operational due diligence guide. For the deeper commercial market analysis that drives Section 4, see the commercial due diligence guide. For the IP-specific deep dive into contractor assignment gaps, see the IP due diligence guide. For the question artifact that initiates the diligence cycle, see the due diligence questionnaire guide. The M&A due diligence process hub is the 6-phase corporate playbook that the 4-stage report drafting timeline overlays on.

Related resources

- M&A due diligence process guide — the 6-phase corporate DD playbook

- Due diligence questionnaire (DDQ): 5 templates + scoring — the question artifact that drives the report's findings

- 174-document M&A DD checklist — the seller-side document inventory

- Operational due diligence: 8-System ODD audit — the source taxonomy for Section 5

- Private equity due diligence: 6-strategy playbook — the hold-strategy-conditional weighting of the 8 sections

- AI due diligence: 5-Layer audit + EU AI Act map — the AI-using-target overlay on Sections 5, 6, and 7

- Commercial due diligence — the market scan and TAM analysis feeding Section 4

- IP due diligence guide — the IP register and contractor assignment chain workstream

- Peony Data Room pricing — flat $52/admin/month for the full DD cycle

- Data room solutions for due diligence — platform spine for the report-drafting cycle

- Data room solutions for M&A — the M&A buyer and seller workflow

Frequently asked questions

What is a due diligence report and who reads it?

A due diligence report is the written synthesis of every diligence workstream that the investment committee, deal partner, board, lender, and R&W insurer rely on to make the proceed-or-walk decision. It is distinct from a due diligence questionnaire (the question artifact issued to the seller) and from a DD checklist (the document inventory the seller assembles). The report is the analytical artifact: it takes the QofE memo, the commercial study, the operational findings, the legal red flags, the IP register, the regulatory map, and the IT diligence, and binds them into a single 30-to-80 page document with a recommendation. Readers are the investment committee (PE), the corporate development executive committee or board (strategic), the LP advisory committee (continuation funds), the syndication bank (LBO debt), and the R&W insurance underwriter pricing the policy. In 2026 the report is also where post-close litigation discovery starts — the Edwards v. GigAcquisitions2 (July 25, 2025) Delaware Chancery decision dismissed fraud claims in part because the court judged the buyer's diligence process limited, refusing to toll the fraud statute of limitations.

Which 8 sections must every IC-ready DD report contain?

The 8-Section IC-Ready DD Report Template covers: (1) Executive Summary plus Recommendation, (2) Deal Strategic Rationale, (3) Financial Findings (QoE, working capital, debt-like items), (4) Commercial Findings (market, TAM, NRR, customer concentration), (5) Operational Findings (mapped to the 8-System ODD audit summary, with cross-link), (6) Legal, Regulatory, and IP Findings, (7) Risk Register (top 10 with severity scores), and (8) Conditions plus Recommended Reps & Warranties. The taxonomy maps 1:1 to how the investment committee, R&W insurer, and post-close litigation discovery will navigate the document. Every section gets a Weighted RAG score, and every section drops into the 4-Outcome Decision Tree. Skipping a section is a V1-veto-grade quality miss because the IC will ask the question anyway and your analyst will improvise the answer in the room.

How do you score sections with the Weighted RAG framework?

The Weighted RAG Scoring framework assigns each of the 8 sections a fixed weight, scores each section 0-100, and produces a single weighted-sum score that drops into the 4-Outcome Decision Tree. The exact weights: Executive Summary 10%, Strategic Rationale 5%, Financial 25%, Commercial 20%, Operational 15%, Legal/Regulatory/IP 10%, Risk Register 10%, Conditions plus R&W 5% (total 100%). Section scoring bands: 70-100 Green (no material issues), 50-69 Amber (issues identified, mitigable), 0-49 Red (deal-killer category absent mitigation). The weighted sum produces an overall score in the same 0-100 band: 70-100 Green proceed, 50-69 Amber proceed-with-conditions or repricing, 0-49 Red walk. This exact weighted-RAG formula is not findable on Google — it is the spine of how we structure IC-ready synthesis across the deals we sit downstream of, and it makes the 30-page report defensible because every paragraph rolls up to a single number the IC can debate.

How does the 4-Outcome Decision Tree work?

The 4-Outcome Decision Tree converts the Weighted RAG Scoring output into one of four explicit deal actions. Outcome 1 — Pass: weighted score above 70 AND no red sections in any core financial, commercial, or legal category. Outcome 2 — Pass-with-conditions: weighted score 60-70 AND specific conditions identified (e.g., escrow above standard, key-person retention, regulatory consent). Outcome 3 — Repricing-required: weighted score 50-60 AND the repricing math is calculable (typically 5-15% equity reduction or 10-30% TEV haircut). Outcome 4 — Walk: weighted score below 50 OR any red section in financial, commercial, or legal core categories regardless of weighted total. The asymmetric structure (a single red core section vetoes a high total) prevents the classic IC failure mode where a high-scoring report with a buried red flag in IP assignment or revenue recognition still passes because the rest of the report looks clean.

How do you write the IC-ready executive summary in under 2 pages?

The executive summary is the most-read and least-written section of the 8-Section IC-Ready DD Report Template. It must be under 2 pages, must lead with the Weighted RAG Scoring overall score and the 4-Outcome Decision Tree recommendation, and must end with the top 3 risks plus the top 3 mitigants. Specifically: paragraph 1 names the target, deal size, hold strategy, and the explicit recommendation (Pass, Pass-with-conditions, Repricing-required, or Walk) with the weighted score. Paragraph 2 names the strategic rationale in one sentence and the unit economics in three numbers (revenue, EBITDA margin, growth rate). Paragraph 3 names the top 3 findings driving the recommendation. Paragraph 4 names the top 3 risks and the mitigants. The IC will read this in 90 seconds and decide whether to read further. If the executive summary cannot stand on its own as the decision artifact, the report has failed its primary job.

What goes in the Risk Register and how do you score severity?

The Risk Register is Section 7 of the 8-Section IC-Ready DD Report Template and is the single most-cited section in post-close litigation discovery. It lists the top 10 risks with three scores each: likelihood (1-5), impact in dollar terms (low / medium / high / extreme), and remediability (the inverse of how fixable the finding is in 12 months). Each risk maps to a specific source section finding, an owner for post-close monitoring, and a mitigation status (open / mitigated / accepted). The top 10 are surfaced from the section scoring — any finding that took a section to Amber or Red appears in the Risk Register. Per SRS Acquiom's 2026 M&A Deal Terms Study analyzing 2,300+ private-target acquisitions valued at $569 billion, claims for breach of the No Undisclosed Liabilities representation are way up, which means the Risk Register is the most legally consequential section in the entire report.

What DD report mistakes triggered post-close litigation 2024-2026?

Six DD report failure modes drove post-close litigation 2024-2026. (1) Limited-scope diligence — Edwards v. GigAcquisitions2 (Delaware Chancery, July 25, 2025) dismissed fraud-induced-de-SPAC claims in part because the court judged Cloudbreak's diligence process limited, refusing to toll the fraud statute of limitations. (2) Pre-close operational control liability — the Bain Capital / PowerSchool ruling (US District Court, March 18, 2026) allowed plaintiffs' claims to proceed based on conduct before Bain's October 2024 acquisition close, including Bain's pre-close veto rights over capital expenditures above $5M and cybersecurity layoffs. (3) Customer-concentration under-disclosure — the recurring 2025-2026 mid-market failure mode where sellers omit a top-customer share above 30% and the buyer surfaces it weeks later. (4) IP assignment gaps for contractor-built code — the surviving cause of action in startup acquisitions. (5) Inflated seller QofE add-backs not flagged in financial findings — Bain's 2026 Global Private Equity Report names inflated seller expectations as one of the two most common deal-killers. (6) Reps-and-warranties survival gaps — per the ABA 2025 Private Target Deal Points Study, 41% of deals now have reps not surviving closing (up from 30%), making the Conditions/R&W section in the report the single most consequential drafting decision. RWI was used on 63% of deals in the 2025 study (up from 55% in 2023).

How does the DD report feed the SPA reps and escrow design?

The DD report feeds the SPA reps and escrow design through Section 8 of the 8-Section IC-Ready DD Report Template, which translates findings into recommended representations, indemnification carve-outs, and escrow size. Specific mechanics: every Risk Register item scored above 12 (the deal-stopper band) requires either a special indemnity outside the R&W policy or an escrow line item; every Amber-scored section translates into a rep-and-warranty with a tighter materiality scrape or a longer survival period; the Conditions section names the closing conditions, the working-capital peg, and the carve-outs for known liabilities. Per the SRS Acquiom 2026 Deal Terms Study, escrow size (median and average) increased from 2024 to 2025 across nearly all deal categories, and RWI was identified on approximately 46% of deals. R&W insurance premiums rose ~16% year-over-year in North America in 2025 per Marsh, with rates at approximately 2.5-3% of policy limit and retentions as low as 0.5% of enterprise value. The report's Conditions section is what the R&W underwriter reads first.

How should you stage DD report drafting against the data room timeline?

Drafting the DD report against the data room timeline maps to four stages of access: Stage 1 (teaser / CIM, weeks 0-2) — the report scaffold is created with executive summary placeholder, strategic rationale, and known-public findings. Stage 2 (Round 1 NDA-gated, weeks 2-6) — financial QofE preliminary findings, commercial market scan, and legal red flags populate Sections 3, 4, and 6; Risk Register starts. Stage 3 (Round 2 final-bidder, weeks 6-12) — operational findings (Section 5), full QofE, IP register, customer reference calls, and IT deep dive populate; Section 7 Risk Register reaches top 10; Section 8 begins drafting. Stage 4 (confirmatory plus SPA, weeks 12-16) — every section reaches final score, executive summary is rewritten, recommendation locks. The Peony spine: NDA gates control which sections of the data room open at each stage, visitor groups isolate workstream-specific reviewers (financial vs commercial vs operational), and page-level analytics show which target documents each reviewer actually opened — the engagement signal that tells the report drafter where to weight the report.

What is the difference between a DD report, a DDQ, and a DD checklist?

Three artifacts, three jobs. A due diligence questionnaire (DDQ) is the question artifact — the structured list of written questions the issuer (LP, buyer, procurement) sends the counterparty before committing capital or signing. A DD checklist is the document inventory artifact — the file list the seller assembles to populate the data room and answer the DDQ. The DD report is the analytical synthesis artifact — the report the buyer writes after receiving the seller's answers and reviewing the documents, presenting the IC-ready recommendation. The DDQ is the input (questions), the checklist is the seller's evidence pack, and the DD report is the buyer's output (analysis plus recommendation). For the DDQ artifact see the dedicated 5-template guide; for the seller-side document inventory see the 174-document M&A DD checklist; this post is about the report.

You might also like

Aug 10, 2026

Financial Due Diligence: QoE, the Working Capital Peg, and Net Debt (2026)

Aug 8, 2026

Clinic Sale Data Rooms: Sell Your Physio, Chiro, or Rehab Clinic Quietly (2026)

Aug 7, 2026

15 Best Virtual Data Room Providers & Software ($0–$200K) in August 2026