Top 15 US VCs Leading Series A Rounds for Startups in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

I've watched hundreds of Series A data rooms flow through Peony — here are the 15 US firms actually leading rounds in 2026.

Last updated: April 2026

TL;DR: Q1 2026 shattered records: global VC hit $297B (81% AI), with the US capturing $250B (Crunchbase, April 2026). Over 50% of US seed/Series A dollars went to $100M+ rounds (Crunchbase, February 2026). Median Series A pre-money valuation hit $49.3M in Q3 2025 — highest ever — with AI commanding a 38% premium (Carta, February 2026). Total round count fell to a six-year low: fewer companies raising, much bigger checks. Time from seed to A has stretched to ~22 months. The mega-fund arms race accelerated: a16z raised $15B, Lightspeed $9B, Kleiner $3.5B, and Founders Fund is nearing $6B — all in a 4-month window. The 15 firms below are actively leading rounds, with fresh Q1 2026 deals and fund closes for each.

A Series A round is the first major institutional venture capital financing a startup raises after its seed stage, typically ranging from $10M to $35M in exchange for 15-25% ownership. Series A is where the story stops being potential and starts being performance. In 2026, US Series A investing has shifted toward capital efficiency — investors want proof that your GTM engine is repeatable, not just that users love the product. The bar is higher than it was two years ago: median time from seed to Series A has stretched to 24-26 months, and investors expect founders to arrive with clean unit economics, not just growth curves.

Choosing the right Series A partner is half the outcome. The wrong firm gives you capital; the right firm gives you distribution, hiring networks, and board-level operating help that compounds for 5-7 years. This guide covers the 15 US firms that are actively leading rounds, what moves each of them, and exactly how to approach them.

1) How to Pick the Right Series A Investors (Quick but Accurate)

-

Start with your constraint. Do you need distribution, hiring, pricing/packaging help, or industrialization? Pick partners with proof they've solved that exact issue for companies like yours.

-

Partner-market fit beats brand. Filter for firms that have led 2 or more Series A rounds in your category in the last 24 months. Read their public theses and "why we invested" posts; mirror the way they frame value.

-

Ownership and reserves. Ask about target ownership at A (often 15-25%), how much they reserve for follow-ons, and whether they routinely lead pro-rata at B/C. This is what protects momentum later.

-

Process honesty. Who is the true decision maker? What's the typical timeline from partner meeting to term sheet? You want predictable pacing.

-

Board operating style. Do reference calls on how they coach, how they handle misses, and how they help recruit execs. You're picking a multi-year collaborator, not a logo.

Organize your materials in a secure data room to demonstrate professionalism and make it easy for investors to review your pitch deck and technical documentation.

How Peony Helps Series A Fundraising

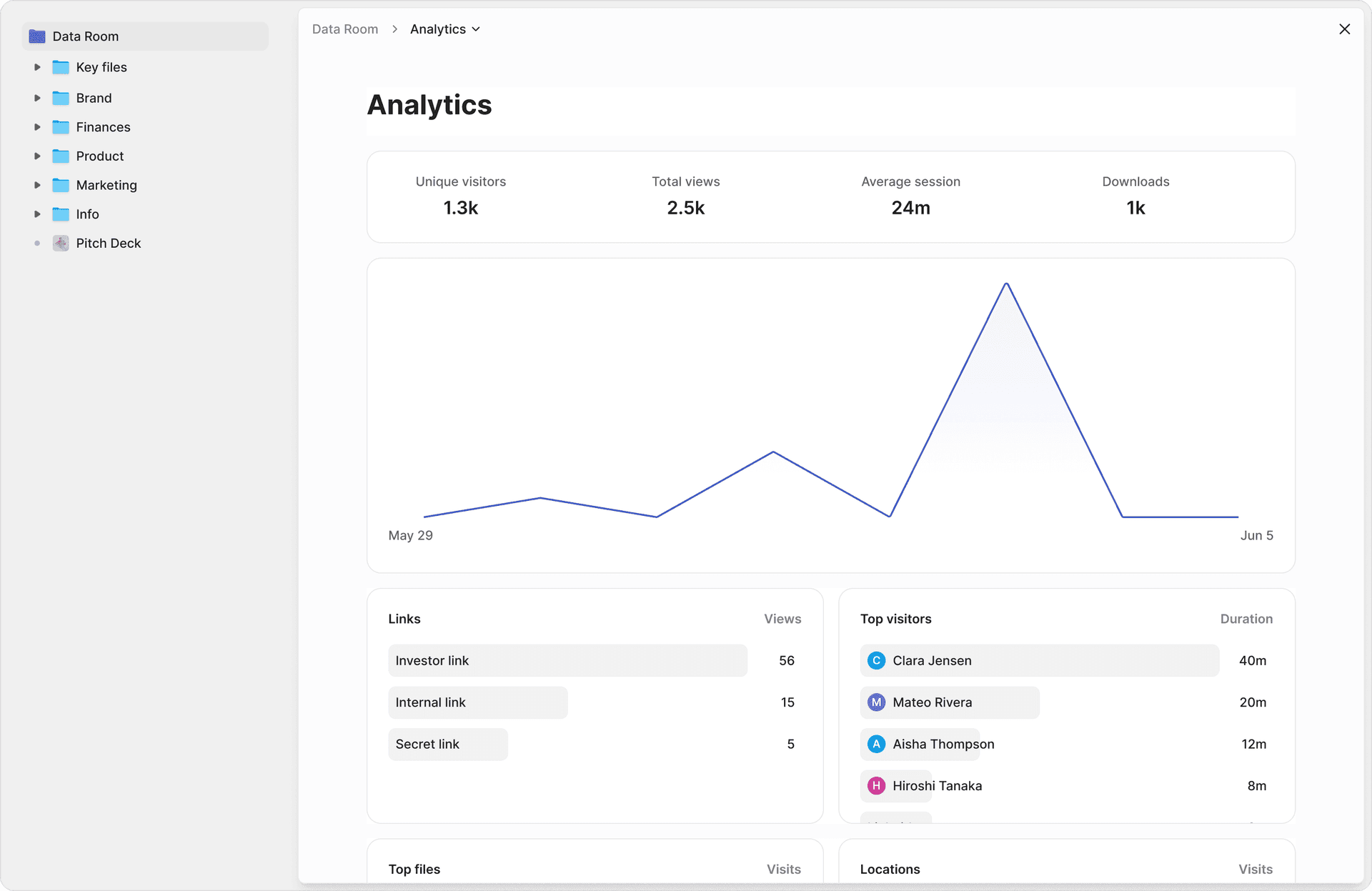

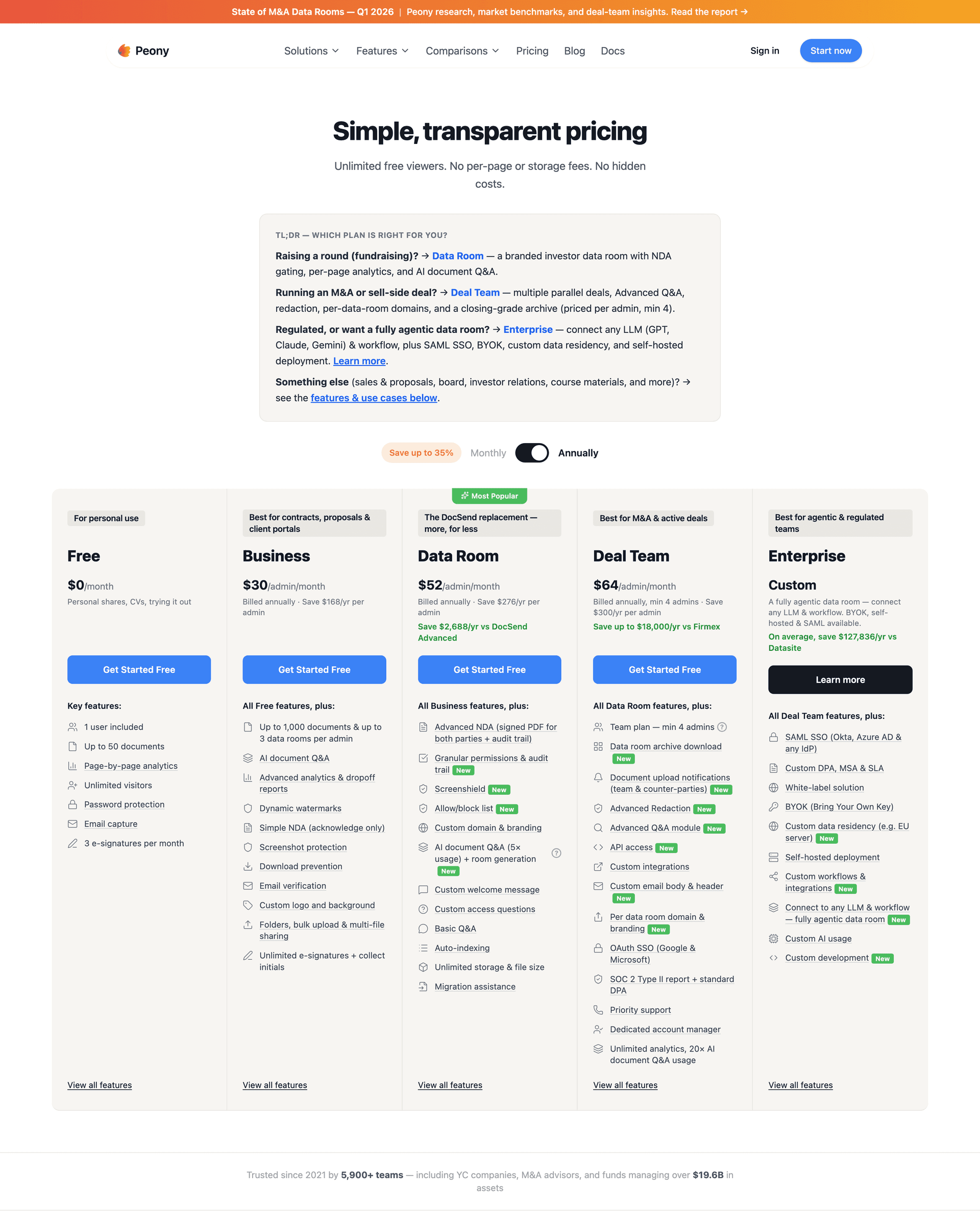

Peony Business ($30/admin/month) shows you which partners spent 40 minutes on your NRR analysis vs 2 minutes on the team slide — page-level intelligence that Google Drive and Dropbox cannot provide.

Here is what that looks like in practice for a Series A process:

- AI auto-indexing: Upload your financial models, cohort analyses, cap table, and customer contracts — Peony organizes everything into a professional data room structure in under 3 minutes. No manual folder dragging.

- Page-level analytics: See exactly which investors reviewed your gross margin analysis, how long they spent on your NRR waterfall, and whether they skipped your product roadmap entirely. Time your follow-ups based on actual engagement, not guesswork.

- Screenshot protection for financial models: Peony blocks and logs screenshot attempts on sensitive documents. When you share 18-month financial projections with 10 firms simultaneously, you need to know if anyone tries to capture your data.

- Dynamic watermarks: Every document page displays the viewer's identity, so forwarded documents are always traceable.

- NDA gates: Require investors to sign your NDA before accessing sensitive financials — built into the data room flow, not a separate DocuSign step.

Start your Series A data room with Peony — secure, AI-powered data rooms built for founders raising capital.

2) 15 Top Series A Investors in the United States (2026)

For each firm you'll get: Center of gravity, Typical Series A check, Will they lead?, What moves them, What they scrutinize, Great ways to approach. (Check sizes are indicative ranges; markets shift.)

1) Sequoia Capital (U.S. and Europe)

- Center of gravity: Multi-stage; category-defining software, fintech, dev tools, infra, AI, consumer platforms.

- Typical Series A check: ~$10-30M.

- Lead? Yes — frequently.

- What moves them: Category narratives with huge upside, world-class teams, early evidence of product-channel fit.

- They scrutinize: Unit economics trendlines, founder-market fit, speed/quality of execution, path to defensibility.

- 2026 signal: New leadership — Alfred Lin and Pat Grady named co-stewards after Roelof Botha stepped down (November 2025). Raised $950M ($750M Series A fund + $200M seed fund, October 2025). Led Edra's $23.8M Series A (March 2026, enterprise automation — TechCrunch). Co-led Rowspace's $50M Series A with Emergence Capital (February 2026, AI financial intelligence). Portfolio exit: Google completed $32B acquisition of Wiz (March 2026) — Sequoia invested from Series A. Ethos IPO on Nasdaq at $19/share raising $200M (January 2026).

- Approach: Warm founder-to-founder paths from portfolio companies; arrive with a crisp "why now" and a 12-18 month proof plan.

2) Andreessen Horowitz (a16z)

- Center of gravity: Full-stack tech (AI, infra, enterprise apps, consumer, bio, fintech, games).

- Typical Series A check: ~$10-35M.

- Lead? Yes.

- What moves them: Platforms with network effects or deep infra moats; top-tier technical teams.

- They scrutinize: Distribution model beyond paid, quality of technical moat, hiring velocity, data advantage.

- 2026 signal: Raised $15B in January 2026 — largest-ever VC fundraise, AUM now $90B+ (Axios). Breakdown: Growth $6.75B, Apps $1.7B, Infrastructure $1.7B, American Dynamism $1.176B, Bio+Health $700M. Co-led Anthropic's $30B round at $380B valuation (February 2026). Focus: "winning key architectures — AI and crypto — and applying to biology, health, defense, education, entertainment."

- Approach: Tie KPIs to a big platform shift (AI, compute, new interfaces). Bring a clean "land then expand" motion.

3) Benchmark

- Center of gravity: High-conviction, concentrated early-stage; enterprise + breakout consumer.

- Typical Series A check: ~$12-25M (concentrated ownership).

- Lead? Yes — classic A-lead.

- What moves them: Exceptional product tempo and word-of-mouth pull; markets that look small but explode.

- They scrutinize: Product quality, founder taste, signal from early users more than noisy growth hacks.

- 2026 signal: Raised $225M in two special "Benchmark Infrastructure" vehicles to double down on Cerebras's $1B round at $23B valuation (February 2026 — TechCrunch). Benchmark first led Cerebras's $27M Series A in 2016. Cerebras targeting Q2 2026 Nasdaq IPO at $22-25B, raising ~$2B. Deliberately keeps fund sizes under $450M. Partners: Puttagunta, Tavel, Lazarte, Fenton, Vishria.

- Approach: Short deck, real product. Founder references matter more than polish.

4) Greylock Partners

- Center of gravity: Enterprise software, AI/ML, data, developer tools; selective consumer bets.

- Typical Series A check: ~$10-25M.

- Lead? Yes.

- What moves them: Technical insight that creates durable workflow lock-in; repeatable top-down or bottoms-up sales.

- They scrutinize: Pipeline math, sales cycle compression, early NRR, and gross margin path.

- 2026 signal: Co-invested $54M with Bessemer in Axiamatic (March 2026, agentic enterprise transformation). Backed Cogent Security's $42M Series A (February 2026, AI autonomous vulnerability remediation for Fortune 500 — PR Newswire). Backed Cylake's $45M launch (March 2026, AI-native data sovereignty). 8 new investments in trailing 12 months.

- Approach: Show how your wedge becomes the system of record or the indispensable layer in the stack.

5) General Catalyst

- Center of gravity: Multi-stage platform; enterprise apps, fintech, health, AI-enabled services.

- Typical Series A check: ~$10-30M.

- Lead? Frequently.

- What moves them: Mission + markets where GC's network opens doors (health systems, financial services).

- They scrutinize: Go-to-market repeatability, leadership maturity, and the "journey to durable economics."

- 2026 signal: Raising ~$10B in new funding (Bloomberg, March 2026). Acquired Janus Henderson for $7.4B with Trian Fund Management (announced December 2025, increased offer to $52/share in March 2026). Led Xflow's $16.6M Series A (February 2026, India B2B cross-border payments). 113 new investments in trailing 12 months; 266 lifetime Series A investments averaging $27.7M. CEO Hemant Taneja describes GC as "strategic conglomerate with VC at its core."

- Approach: Pair story with a measured operating plan (hiring, payback, burn multiple).

6) Accel (U.S.)

- Center of gravity: Enterprise software, security, data/infra, product-led apps; occasional consumer.

- Typical Series A check: ~$8-25M.

- Lead? Yes.

- What moves them: PLG traction or crisp enterprise wedge with short time-to-value.

- They scrutinize: Activation/engagement cohorts, expansion drivers, and what kills churn.

- 2026 signal: Raised $650M Accel XVI US early-stage fund (January 2026) and seeking $4B+ for latest growth fund. Led Knight FinTech's $23.6M Series A (January 2026, banking software — SiliconANGLE). Portfolio company Ethos IPO on Nasdaq (January 2026) — Accel did not sell shares. 65 new investments in trailing 12 months.

- Approach: Show bottoms-up love + a scalable top-down motion (partner channels, ecosystems).

7) Lightspeed Venture Partners (U.S.)

- Center of gravity: Enterprise, data/AI, cybersecurity, fintech, infra; selective consumer.

- Typical Series A check: ~$10-30M.

- Lead? Yes.

- What moves them: Clear "system of record" or "system of intelligence" positioning; big adjacency map.

- They scrutinize: Sales efficiency, partner attach rates, pricing/packaging discipline.

- 2026 signal: Raised $9B in December 2025 — largest fundraise in firm history across 6 vehicles, AUM now over $40B (BusinessWire). 165 AI-native companies backed, $5.5B+ invested in AI. Led Nexthop AI's $500M Series B at $4.2B valuation (March 2026, AI data center networking). 42 investments already in 2026 as of March.

- Approach: Bring a partner-led GTM angle (cloud marketplaces, SI channels) and proof it's repeatable.

8) Bessemer Venture Partners (BVP)

- Center of gravity: Cloud, AI, cybersecurity, fintech, vertical SaaS; rigorous benchmarking culture.

- Typical Series A check: ~$10-25M.

- Lead? Yes.

- What moves them: Metrics-honest stories that line up with BVP's Cloud/AI benchmarks.

- They scrutinize: NRR quality, gross margin glidepath, sales productivity, and category definition.

- 2026 signal: Led Converge Bio's $25M Series A (January 2026, AI drug discovery — TechCrunch). Led NODA AI's $25M Series A (February 2026, AI defense/autonomous systems for DoD and UK MoD). Co-invested $54M with Greylock in Axiamatic (March 2026). Published State of Health AI 2026 and AI Infrastructure Roadmap 2026 reports. 69 new investments in trailing 12 months.

- Approach: Use their public benchmarks to frame your efficiency and growth — meet them in their language.

9) Khosla Ventures

- Center of gravity: Bold tech across software, AI, deep tech, climate/bio with commercial routes.

- Typical Series A check: ~$8-20M.

- Lead? Yes.

- What moves them: Audacious technical advantage with a credible path to margin.

- They scrutinize: Physics/econ of the moat, time-to-product truth, and how you cross from R&D to revenue.

- 2026 signal: Led Comp's $17.25M Series A (February 2026) — first-ever Khosla investment in Brazil, AI HR platform with Nubank and QuintoAndar as clients, 400% growth in 2025 (TechCrunch). Participated in Swarm Aero's $35M Series A (March 2026, large-drone defense swarms). 58 new investments in trailing 12 months.

- Approach: Pair ambition with evidence. One page on cost curve + milestones earns trust.

10) Founders Fund

- Center of gravity: Audacious companies across software/AI, defense, frontier, fintech.

- Typical Series A check: ~$10-30M.

- Lead? Yes.

- What moves them: Non-obvious insight, speed to dominance, contrarian GTM that works.

- They scrutinize: Proof over polish: hard before/after ROI, velocity, hiring bar.

- 2026 signal: Growth Fund IV nearing $6B close (March 2026), $1.5B from partners (TechCrunch). Co-led Anthropic's $30B round at $380B valuation (February 2026). Led Nominal's $80M acceleration round at $1B valuation (March 2026, defense hardware testing — 4 of 5 largest US defense contractors as customers). Total Nominal raised: $155M in 10 months.

- Approach: Big swing + crisp evidence; outline what "winning hard" looks like in 24 months.

11) Menlo Ventures

- Center of gravity: Enterprise software, cybersecurity, fintech, AI-enabled applications; occasional frontier.

- Typical Series A check: ~$10-25M.

- Lead? Often.

- What moves them: Clear buyer who urgently pays; pragmatic GTM plans.

- They scrutinize: Payback, win/loss reasons, and ICP tightness.

- 2026 signal: Targeting $1.5B across two new funds — Menlo Inflection IV ($800M) + Menlo Ventures XVII ($700M). Led Axiom's $200M Series A at $1.6B valuation (March 2026, "verified AI" — scored perfect 12/12 on Putnam math exam and proved a 20-year-old open number theory conjecture — SiliconANGLE). $100M joint fund with Anthropic — first 18 startups backed (December 2025). 31 new investments in trailing 12 months.

- Approach: Bring 3 design-partner stories with quantified before/after.

12) Index Ventures (U.S.)

- Center of gravity: U.S.-EU bridge; enterprise apps, dev tools, fintech, productivity; consumer marketplaces.

- Typical Series A check: ~$10-25M.

- Lead? Yes.

- What moves them: Ambitious cross-border scale narratives and product taste.

- They scrutinize: Early internationalization readiness, pricing discipline, channel leverage.

- 2026 signal: Bloomberg reported 1,100% fund returns (January 2026). $2M Figma investment turned into $2.2B stake after IPO. Led Kindred's $85M Series C (February 2026, home-swapping platform with 300K members — PR Newswire). Current funds: $800M venture + $1.5B growth + $300M Origin seed ($2.6B total, raised July 2024). Danny Rimer thinking about retirement; firm priming next-gen leaders.

- Approach: If you plan to scale across U.S. and EU, show the sequencing and the first two hires you'll make.

13) Union Square Ventures (USV)

- Center of gravity: Thesis-driven investor (networks, protocols, climate/health data, enabling infra).

- Typical Series A check: ~$5-15M.

- Lead? Frequently at A with strong theses fit.

- What moves them: Network effects and protocols with real usage; mission clarity.

- They scrutinize: Community/creator dynamics, governance, and sustainable economics.

- 2026 signal: Participated in Efficient Computer's $60M Series A (February 2026, energy-efficient AI edge processors — Rebecca Kaden: "enable new applications long constrained by power" — PR Newswire). Hiring an "AI Lead" to reimagine how a venture firm develops theses and finds companies. 14 new investments in trailing 12 months.

- Approach: Map directly to an active USV thesis; bring evidence of bottoms-up community pull.

14) Emergence Capital

- Center of gravity: Pure B2B SaaS; "industry-transforming" workflows, often the system of record.

- Typical Series A check: ~$10-20M.

- Lead? Yes — classic enterprise A.

- What moves them: Narrow wedge that becomes a category; customer-obvious ROI.

- They scrutinize: Time-to-value, champion playbook, deployment friction, and mid-market to enterprise path.

- 2026 signal: Closed $1B Fund VII in March 2025 — first raise in ~4 years. Co-led Rowspace's $50M Series A with Sequoia (February 2026, AI financial intelligence). Led Harper's combined $46.8M seed + Series A (2026, AI insurance brokerage, Y Combinator-backed). 7 investments in 2026 as of February; 63 lifetime Series A investments averaging $14.9M.

- Approach: One slide on how you turn pilots into line items in 2-3 quarters.

15) Kleiner Perkins

- Center of gravity: AI/infra/dev tools, climate/industrial software, consumer.

- Typical Series A check: ~$10-25M.

- Lead? Yes.

- What moves them: Category creation and compound founders.

- They scrutinize: Hiring velocity, early enterprise validation, platform adjacency.

- 2026 signal: Raised $3.5B — KP22 ($1B early-stage) + KP Select IV ($2.5B growth) in March 2026 (TechCrunch). John Doerr personally championed Eridu's $200M Series A (March 2026, AI networking infrastructure). Fortune profile (January 2026) credits turnaround to Mamoon Hamid (who led Figma's $25M Series B — now a $19.3B public company). Focus areas: professional services, healthcare, autonomy, cybersecurity, financial services, physical economy. 18 investments in 2026 as of March; 231 lifetime Series A investments averaging $17.1M.

- Approach: Map the 24-month category blueprint and your unfair distribution.

3) Five Quick Tips for Pitching Series A Investors (2026)

-

Lead with evidence, not adjectives. One page with NRR, gross margin, CAC payback, burn multiple, and 3 customer before/after stories. Use your startup data room to organize these materials clearly.

-

Show a repeatable motion. Diagram your GTM engine (channels, quotas, ramp time, partner attach) and what you've already proven.

-

Make the category inevitable. Name the enemy (status quo), show the wedge, and sketch how you own the blueprint 12-24 months from now.

-

Use-of-proceeds mapped to proof. "With $X we will achieve Y proofs in 12-18 months" (e.g., enterprise NRR above 120%, 3 SI partners live, gross margin +8-12 pts).

-

Run a clean process. Tight data room, clear timeline, back-channel references teed up, and a crisp answer to "why now / why you." Use Peony to organize your fundraising materials and track investor engagement with page-level analytics.

Frequently Asked Questions

We hit $2M ARR with 130% NRR — which US VCs actually lead Series A rounds at this stage in 2026?

At $2M ARR with 130% NRR, you are in range for Sequoia, Benchmark, Accel, and Greylock — all of which actively lead $10-25M Series A rounds for B2B companies showing efficient growth. Bessemer is another strong fit because their published cloud benchmarks let you frame your metrics in their language. For a 25-person SaaS team running a competitive Series A process with 8-10 firms, Peony Business ($30/admin/month) gives you page-level analytics showing which partners spent the most time on your NRR analysis versus your product roadmap — intelligence that Dropbox or Google Drive simply cannot provide.

I'm a solo technical founder with $800K ARR in vertical SaaS — is that enough to attract top-tier US Series A firms?

Yes, $800K ARR in vertical SaaS can attract top-tier firms if your net retention exceeds 120% and your gross margins sit above 70%. Khosla Ventures and Emergence Capital both actively seek narrow-wedge vertical plays at this stage, typically writing $8-20M checks. For a solo founder managing investor conversations across 6-8 firms simultaneously, Peony Data Room ($52/admin/month) includes AI auto-indexing that organizes your financial models, cohort data, and customer contracts in under 3 minutes — a professionalism signal that manual folder structures on Google Drive or Dropbox cannot match.

Our fintech startup has 40% month-over-month growth but only $1.5M ARR — should we wait or start talking to Series A VCs now?

Start conversations now. At 40% MoM growth, firms like a16z, General Catalyst, and Lightspeed will take meetings because trajectory matters more than absolute ARR at this velocity. Most US Series A rounds in 2026 close between $10-30M, and investors want to see 2-3 quarters of sustained growth before committing. Build your data room early so materials are ready when a partner asks for diligence. Peony Business ($30/admin/month) lets you set NDA gates on sensitive financials so only serious partners access your burn rate and unit economics — screenshot protection blocks and logs any attempt to capture your proprietary data, a safeguard that Google Drive and Dropbox do not offer at all.

We're raising a $15M Series A and have 12 VCs in our pipeline — how do I figure out which ones are actually serious versus just taking meetings?

The single best signal is time spent in your data room. Firms doing real diligence spend 30-60 minutes reviewing financial models and customer references, while tire-kickers skim the deck in under 5 minutes. With 12 firms in parallel, you need engagement data to prioritize your follow-ups. Peony Business ($30/admin/month) shows you exactly which pages each partner reviewed and for how long — if a Sequoia associate spent 45 minutes on your NRR waterfall but skipped the team slide, that tells you exactly what to address in your next conversation. Google Drive and Dropbox give you download counts at best, with no visibility into which pages were actually read.

My co-founder and I are based in Austin — do these top 15 VCs only fund Bay Area startups, or do they invest outside SF?

All 15 firms on this list actively fund companies outside San Francisco. Post-2020, geographic constraints have largely disappeared for Series A — Benchmark, Founders Fund, and General Catalyst have all led $10-25M rounds for distributed teams. What matters is your ability to run a professional process regardless of location. For a two-person founding team in Austin running diligence with coastal VCs, the Peony Data Room plan ($52/admin/month) provides dynamic watermarks with viewer identity on every document page, so you know exactly who accessed your materials even when decks get forwarded internally at a firm — traceability that Box and Google Drive watermark workarounds cannot replicate.

We're a health-tech company at $3M ARR and want to raise Series A — which of these VCs have actual health-tech expertise?

General Catalyst and Khosla Ventures are your strongest fits for health-tech at $3M ARR. General Catalyst runs a dedicated health assurance practice and has direct relationships with health systems that accelerate enterprise sales. Khosla backs bold health-tech with commercial routes, typically writing $8-20M Series A checks. For a health-tech company sharing HIPAA-sensitive patient outcome data during diligence, Peony Data Room ($52/admin/month) includes multi-level access gating so clinical data is only visible to partners who have signed your NDA — a compliance layer that Google Drive and Dropbox lack entirely — neither supports NDA gates or document-level permission tiers.

I got a term sheet from one of these firms but the valuation feels low at $50M pre — how do I use competing interest to negotiate?

A $50M pre-money on a $15M Series A implies 23% dilution, which is within the typical 15-25% ownership range these firms target. To negotiate, you need concrete proof of competing interest — not just verbal signals. Run a tight 3-week process with 4-5 firms in parallel and let engagement data do the talking. Peony Business ($30/admin/month) gives you timestamped page-level analytics showing that three other firms spent 2-plus hours in your data room this week — real leverage for a negotiation conversation that Google Drive view counts or Dropbox download logs cannot provide.

We're pre-revenue but have a working AI product with 5,000 weekly active users — can we still get a Series A from these firms?

Pre-revenue Series A rounds are rare but possible in 2026 if your engagement metrics are exceptional. Founders Fund and a16z are the most open to pre-revenue deals, especially in AI where usage growth can proxy for revenue. You will need to show weekly active user retention curves, feature adoption depth, and a credible monetization plan. For an AI startup sharing proprietary model performance data with investors, Peony Business ($30/admin/month) offers AI-powered Q&A where investors can ask questions about your documents and get cited answers with page numbers — eliminating back-and-forth emails while keeping sensitive training data behind access controls that Box and Google Drive cannot enforce at the document level.

Final Thoughts

Series A fundraising in 2026 requires precision, preparation, and professional presentation. The investors listed above are actively deploying capital, but they expect founders to come prepared with clear unit economics, realistic growth plans, and evidence of product-market fit.

Series A investors evaluate not just your traction, but your ability to execute on scaling, manage operations, and build category-defining companies. Organize your startup data room, track investor engagement, and demonstrate operational maturity from day one.

Get started with Peony for your Series A fundraising — secure, AI-powered data rooms built for founders raising capital.

Related Resources

- 15 Best US Seed Investors

- Startup Data Room Checklist

- Series A Data Room: The Step-Change Round — how to build the room these leads will grade

- SPV Data Room for Syndicate Leads — running a co-investment SPV into a Series A deal

- Startup Fundraising Strategy

- How to Send Pitch Deck to Investors

- Track Pitch Deck Engagement

- Virtual Data Room Providers Compared

- Peony vs Google Drive

- Peony vs Dropbox

- Fundraising Data Room Solutions

- Venture Capital Solutions

You might also like

Mar 26, 2026

Who's Still Writing Seed Checks? 15 Best US Based Investors in 2026

Apr 15, 2025

Top 5 Series A Investors in Mexico (2025): Complete Founder's Guide to Raising Your Next Round

Feb 15, 2025

Top 5 Series A Investors in Chile (2025): Complete Guide to Raising Growth Capital