I Mapped Where Startup Talent Is Moving (Here's the Data) in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: March 2026

We run Peony, a data room platform. Our users raise capital in 40+ countries -- from seed rounds in Austin to Series C raises in Singapore to PE deals in London. When you watch thousands of fundraising processes unfold from the inside, patterns emerge that no single VC report captures.

Over the past quarter, I pulled data from PitchBook, Crunchbase, SignalFire, Startup Genome, Deel, LinkedIn, and half a dozen government sources -- combining these with proprietary Peony data on where our users are raising and which cities generate the most investor engagement -- to answer a question our founders keep asking: where should I be building, and does it actually matter?

The short answer: yes, it matters more than ever. The long answer is this 4,000-word breakdown.

TL;DR: OpenAI just raised $120B at an $850B valuation (March 24, 2026) and Anthropic closed $30B at $380B (February 12) -- together these two rounds exceed what the entire US VC market deployed in 2020. US VC hit $339.4B in 2025 (+57.6% YoY), with AI capturing 65.6% of all deal value (PitchBook-NVCA). SF + NYC employ 65% of AI engineers at VC-backed startups, reversing pandemic dispersal (SignalFire). But the most underreported shift is global: Shenzhen jumped 11 spots in the GSER 2025 rankings as hardware and robotics founders discover its unmatched supply chain -- 74,000+ robotics enterprises and a $630M government AI subsidy are pulling the smartest talent in the world toward the Pearl River Delta. The talent map is being redrawn in real time.

The Big Picture: AI Is Eating Venture Capital Alive

Let me start with what happened in the past 30 days.

On March 24, 2026, OpenAI closed a $120 billion round at an $850 billion valuation -- the largest private funding round in history (CNBC). Six weeks earlier, Anthropic closed $30 billion at $380 billion (CNBC). February 2026 alone set an all-time monthly record of $189 billion in global startup funding, with AI capturing 90 percent of it (Crunchbase).

In the first eight weeks of 2026, AI startups raised over $220 billion -- already exceeding half of everything raised in all of 2025 (Crunchbase).

Now zoom out. US VC hit $339.4 billion across 16,709 deals in 2025, up 57.6 percent from 2024 (PitchBook-NVCA Q4 2025 Venture Monitor). AI captured 65.6 percent of all US deal value -- $222 billion out of $339 billion. Globally, the OECD pegs AI's share at 61 percent of all venture capital in 2025, up from 30 percent in 2022 (OECD).

This matters for every founder reading this, even if you are not building an AI company. When one vertical absorbs two-thirds of the oxygen, everything else -- climate, fintech, health, SaaS -- is fighting over the remaining third. And when capital concentrates into a single theme, it also concentrates geographically. The cities that win at AI win at everything.

Which brings us to the map.

US Metro Rankings: Where the Money Actually Goes

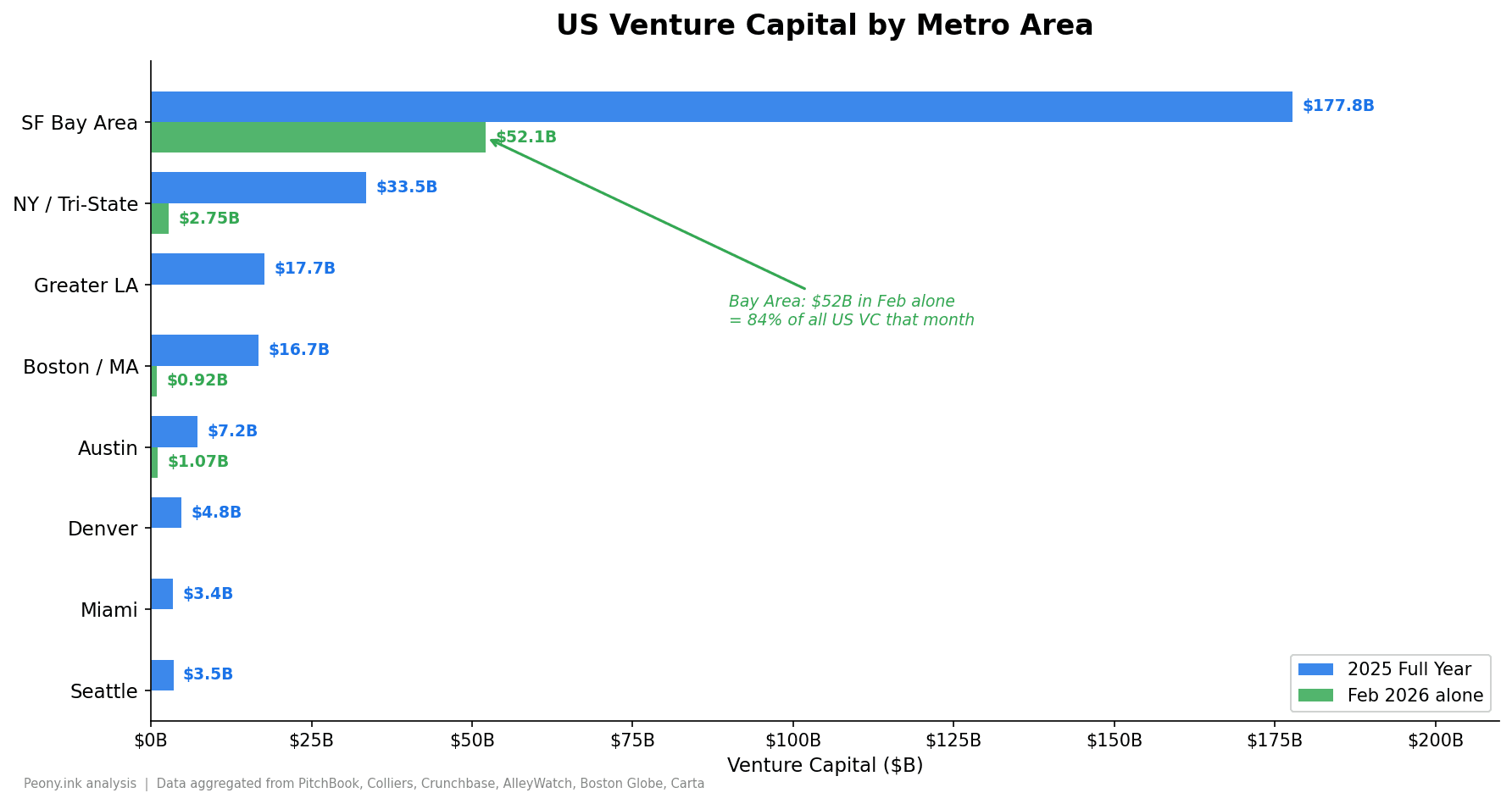

Here is the 2025 full-year VC breakdown for the top eight US metros, pieced together from PitchBook data (via Colliers), Crunchbase, Boston Globe, Refresh Miami, and Carta:

| Metro Area | 2025 VC Deal Value | 2024 | YoY Change |

|---|---|---|---|

| SF Bay Area | $177.8B | $99.4B | +79% |

| NY / Tri-State | $33.5B | $28.5B | +18% |

| Greater Los Angeles | $17.7B | $10.8B | +64% |

| Boston / Massachusetts | $16.7B | $11.6B | +44% |

| Austin-Round Rock, TX | $7.2B | $3.4B | +112% |

| Denver-Aurora, CO | ~$4.8B | $5.0B | ~Flat |

| Miami-Fort Lauderdale, FL | ~$3.4B | $3.6B | ~Flat |

| Seattle-Tacoma, WA | ~$3.5B | $4.6B | est. |

The SF Bay Area nearly doubled in a single year -- from $99.4 billion to $177.8 billion -- driven almost entirely by AI mega-rounds. Austin was the biggest surprise, more than doubling to $7.2 billion and setting an all-time record (Crunchbase).

And 2026 is accelerating even faster. Here is what February 2026 alone looked like by metro (sourced from AlleyWatch February 2026 US Venture Capital Report):

| Metro | Feb 2026 Funding | Key Deal |

|---|---|---|

| San Francisco | $33.9B | Anthropic $30B |

| Mountain View | $16.7B | Waymo $16B |

| New York | $2.75B | Vestwell $385M |

| Austin | $1.07B | Apptronik $520M |

| Sunnyvale | $1.05B | Cerebras $1B |

| Boston | ~$922M | Multiple AI/biotech |

| San Jose | $514M | Ayar Labs $500M |

The Bay Area (SF + Mountain View + Sunnyvale + San Jose) captured over $52 billion in a single month -- 84 percent of all US VC in February. Nine of the fifteen largest February rounds were Bay Area companies, accounting for 96.4 percent of top-15 capital. This is concentration at a level we have never seen before.

Let me walk through what is actually happening in each of these ecosystems.

San Francisco / Bay Area: Still the Center of Gravity

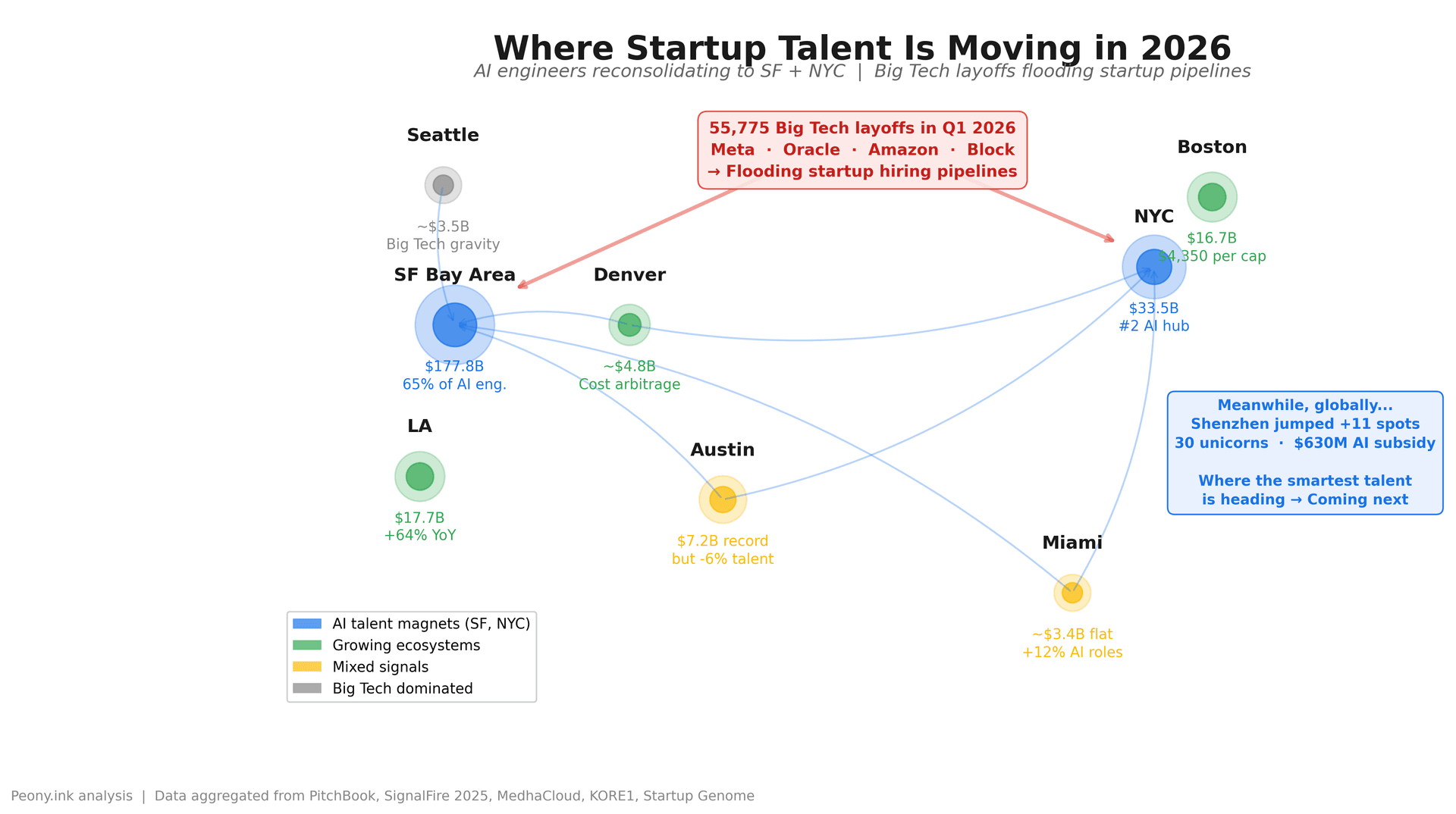

The Bay Area pulled in $177.8 billion in 2025 -- nearly doubling from $99.4 billion in 2024 (Colliers/PitchBook). It still holds the highest development score (89.5) of any ecosystem globally. That $177.8 billion in a single year is more than the next seven US metros combined.

But here is what has changed: the Bay Area's dominance is increasingly an AI story. The reconsolidation of AI engineers into SF and NYC means that 65 percent of AI engineers at VC-backed startups are concentrated in just two metros (SignalFire 2025). If you are building a foundation model, a dev tools company, or an AI-native application, SF is not optional -- it is where your employees already live and where your investors take meetings.

Only California and Washington gained VC share year-over-year in 2025 (Crunchbase). California's share climbed to 64 percent of all US VC. Think about that: nearly two-thirds of American venture capital flows into a single state.

The downside? Cost. A Series A AI startup in SF is spending $200,000-plus per engineer when you factor in salary, benefits, and the most expensive commercial real estate in the country. It is like trying to open a restaurant on the most expensive block in Manhattan -- the foot traffic is unbeatable, but the rent might kill you first.

New York City: The Second City That Does Not Want to Be Second

NYC and the tri-state area captured $33.5 billion in 2025 -- up 18 percent, but the gap with SF actually widened as AI mega-rounds concentrated on the West Coast.

What NYC does have is infrastructure diversity. Wall Street, media, advertising, fashion, and healthcare all generate startup ideas that do not exist in SF. Fintech founders in NYC have something SF founders do not: they can walk across the street and talk to the institutions they are trying to disrupt.

The AI angle is strong here too. NYC is the other half of that 65-percent AI engineer concentration. And unlike SF, New York has a commercial real estate crisis that is actually creating opportunity -- vacant office space is being converted into startup hubs at rents that would have been unthinkable in 2019.

Boston: The Per Capita King

Massachusetts raised $16.7 billion in 2025, up 12 percent year-over-year (PitchBook data via Boston Globe). That might look modest next to SF, but do the math differently and Massachusetts becomes the most interesting state in the country.

Massachusetts attracted $16.7 billion in 2025 -- roughly $2,360 per capita, among the highest in the nation (PitchBook via Boston Globe). The state has only 7 million people. That is a smaller population than the Bay Area metro alone, yet it punches far above its weight in absolute venture dollars.

The reason is two-fold: biotech and AI research. MIT, Harvard, and the cluster of research hospitals in the Longwood Medical Area create a pipeline of deep-tech startups that command massive rounds. Life sciences and enterprise AI/software dominate the deal flow, with biotech consistently accounting for over half of Massachusetts VC.

If you are building in biotech, life sciences, or AI with a research angle, Boston is arguably a better per-dollar bet than SF. The accelerator ecosystem is deep -- The Engine writes $1M-$5M checks for tough-tech companies, and MassChallenge runs the world's largest equity-free accelerator program.

Los Angeles: Where Entertainment Meets AI

Greater LA surged to $17.7 billion in 2025 (up 64 percent from $10.8 billion), with aerospace and defense accounting for over one-third of deal value (Colliers/PitchBook). The entertainment-AI convergence is real too. Studios, gaming companies, and content platforms are all investing in AI-generated content, virtual production, and personalization engines.

LA also benefits from SpaceX, which has created an aerospace-tech cluster in Hawthorne that pulls in defense and space-adjacent startups. The city has enough engineering talent in computer vision (thanks to film VFX pipelines) that AI startups can hire without competing directly with OpenAI and Anthropic for the same candidates.

The catch: LA's startup ecosystem is geographically fragmented. Santa Monica, Venice, Culver City, Pasadena, and Downtown LA are all technically "LA" but separated by some of the worst traffic in America. It is like having five small startup cities that happen to share a metro area name.

Denver/Boulder: The Quiet Climber

Denver held roughly steady at ~$4.8 billion in 2025 -- not growing as fast as the leaders, but holding its position. The Colorado accelerator scene is stronger than most people realize, and the cost-of-living arbitrage compared to SF is significant.

The Denver-Boulder corridor benefits from aerospace (Lockheed Martin, Ball Aerospace), a growing AI cluster, and a quality of life that attracts senior engineers who have burned out on Bay Area costs. It is the classic "raise in SF, build in Denver" pattern.

Seattle: Big Tech's Gravity Well

Seattle's $4.6 billion in VC comes with an asterisk: the city's startup ecosystem lives in the shadow of Amazon, Microsoft, and their combined 150,000-plus local employees. The talent pool is extraordinary, but Big Tech compensation makes it hard for startups to compete for engineers.

LinkedIn data shows Seattle had the strongest month-over-month hiring growth at +11.4 percent in January 2024 (LinkedIn Economic Graph), but much of that growth went to large tech companies, not startups. The city produces world-class engineers who eventually start companies -- but many wait until they have accumulated enough Big Tech equity to self-fund.

Miami: The Hype Reality Check

Miami's ~$3.4 billion in 2025 -- essentially flat -- tells a more complicated story than the city's boosters would like. It ranked sixth nationally for deal count (PitchBook/Refresh Miami), but the total dollar amount has plateaued. On the positive side, AI roles grew 12 percent year-over-year (SignalFire), and the zero state income tax still attracts founders from high-tax states.

On the other hand, Florida is actually losing VC share at the state level (Carta). The hype cycle of 2021-2022 -- when every crypto founder and their dog moved to Miami -- has cooled. The ecosystem lacks the deep engineering talent density of SF, NYC, or Boston. Miami is great for your tax bill and your Instagram. It is not yet great for hiring your fifth machine learning engineer.

Austin: Texas Losing Startup Talent

Austin is the most confusing data point in this entire analysis. VC deal value more than doubled to $7.19 billion in 2025 -- an all-time record, surpassing even the 2021 peak (Crunchbase). The top deals: Base Power ($1B Series C), Saronic ($600M), NinjaOne ($500M), Apptronik ($415M).

But here is the contradiction: even as capital poured in, SignalFire found that Texas is losing startup talent. Austin saw a 6 percent drop in headcount at VC-backed startups; Houston dropped 10.9 percent (SignalFire 2025). The money is flowing in but the people are flowing out. That gap cannot last.

The reality is nuanced. Austin still has a strong accelerator ecosystem, and companies like Tesla and Oracle moving their HQs brought attention. But attention and venture capital are not the same thing. When AI reconsolidated to SF and NYC, Austin lost the remote-work premium that had been driving inbound talent since 2020.

Global Hubs: The World is Not Flat

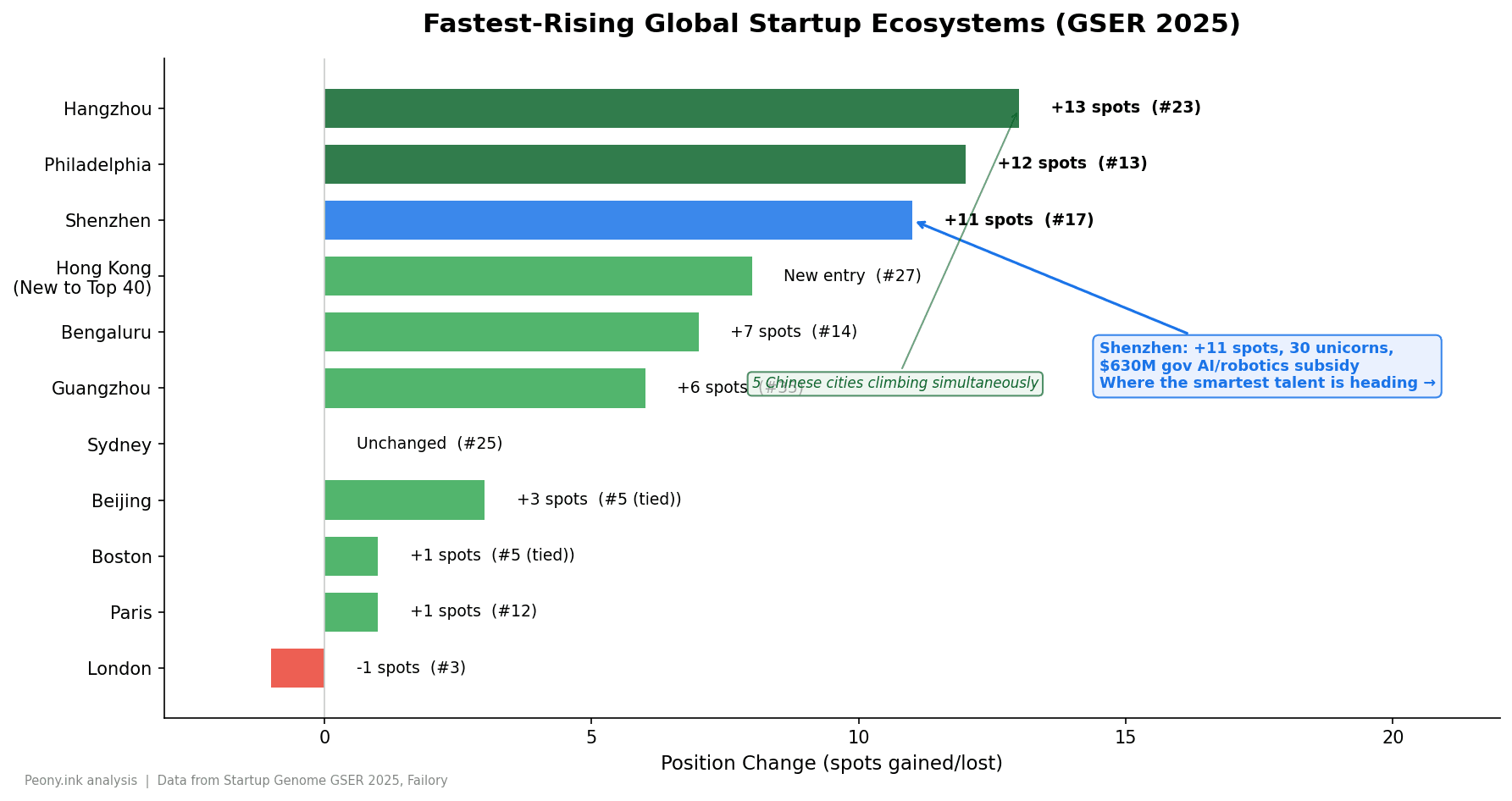

Now let us zoom out. The Startup Genome Global Startup Ecosystem Report 2025 ranks the world's top ecosystems (GSER 2025):

| Rank | City | Notable Movement |

|---|---|---|

| 1 | Silicon Valley | Unchanged since 2020 |

| 2 | New York City | Held #2 |

| 3 | London | Dropped from tied #2 |

| 4 | Tel Aviv | Per capita leader |

| 5 (tied) | Boston / Beijing | Both moved up; Beijing from #8, Boston from #6 |

| 10 | Shanghai | Edged up |

| 12 | Paris | Rising |

| 13 | Philadelphia | +12 spots |

| 14 | Bengaluru-Karnataka | +7 spots |

| 17 | Shenzhen | +11 spots |

| 23 | Hangzhou | +13 spots |

| 25 | Sydney | Oceania's top |

| 27 | Hong Kong | New to top 40 |

| 37 | Sao Paulo | LATAM's only top 40 |

Three trends jump off the page.

Chinese Cities Are Surging

Shenzhen jumped 11 spots. Hangzhou jumped 13. Guangzhou climbed 6. Hong Kong entered the top 40 for the first time. Beijing re-entered the top 5. Shanghai edged up to 10th.

This is not one city rising -- it is an entire national ecosystem accelerating simultaneously. China's government has made technology self-sufficiency a strategic priority, and the capital is following.

Shenzhen deserves its own spotlight. It jumped 11 spots to #17 globally, and the reason is structural: Shenzhen has something no other city on Earth can offer AI-hardware founders. Over 74,000 robotics enterprises, a $630 million government AI/robotics subsidy (February 2025), a $1.3 billion municipal angel investment fund, and the world's deepest electronics supply chain within a one-hour drive. If you are building anything that needs to be manufactured -- robots, sensors, drones, consumer hardware, medical devices -- Shenzhen's supply chain cuts your prototype cycle from months to weeks.

The talent signal is even more telling. Engineers and founders who previously would have gone to SF or Boston for AI roles are now looking at Shenzhen for AI-hardware convergence -- the place where software models meet physical products. With 42 unicorns already in the city and ecosystem growth of 23.2 percent in 2025, Shenzhen is not just climbing rankings. It is becoming the world's factory for intelligent machines. We will have a deep dive on the Shenzhen talent story coming next.

For VCs: if you are not sourcing deals in Chinese cities, you are ignoring the fastest-growing startup ecosystems on the planet. Cross-border deal flow between Silicon Valley and Shenzhen/Hangzhou is accelerating despite geopolitical tension.

Tel Aviv: $15.6 Billion Despite a War

This is the most remarkable data point in the entire global dataset. Israeli startups raised $15.6 billion in 2025 (Calcalist Tech) -- while the country was actively engaged in a military conflict. Cyber alone accounted for $4.4 billion across 130 rounds, a record. Seed rounds in cybersecurity surged 97 percent from 2023 levels.

Tel Aviv's ecosystem is built on something most cities cannot replicate: mandatory military service that produces a pipeline of engineers trained in signals intelligence, cryptography, and systems engineering. It is like if every 18-year-old in a city had to spend three years working at the NSA before they could start a company. That pipeline is structurally unbreakable.

Bengaluru: India's Engine Room

Bengaluru-Karnataka jumped 7 spots to 14th globally. India is the world's most underinvested large startup ecosystem relative to its engineering talent base. The city produces more software engineers per year than most countries, and the cost differential means a dollar of VC goes three to five times further than in SF.

The Indian accelerator ecosystem is maturing rapidly, and the Bengaluru-Singapore corridor is becoming the primary fundraising axis for Southeast Asian founders.

Other Notable Global Moves

Singapore continues to serve as the gateway between East and Southeast Asian capital and Western investors. Its regulatory clarity and English-language legal system make it the default incorporation jurisdiction for founders building across ASEAN markets.

Dubai/UAE attracts founders with its "zero tax" reputation, but the reality is more nuanced. Qualifying Free Zone companies get 0 percent on qualifying income, but non-qualifying income is taxed at 9 percent. Startups under AED 3 million revenue get zero taxable income until December 2026. And multinational enterprises with EUR 750 million-plus revenue face a 15 percent Domestic Minimum Top-up Tax from January 2025 (Khaleej Times, PwC Tax Summaries). The tax story is real but requires compliance homework.

London dropped from tied-second to third in global rankings. Still Europe's undisputed number one, but the gap with Tel Aviv and Beijing is narrowing. Brexit headwinds on hiring continue to bite.

Japan is emerging as an unexpected bright spot. The Japanese VC market hit $20 billion in 2024 (IMARC), with H1 2025 seeing $2.3 billion raised excluding debt. Sakana AI closed a JPY 30.1 billion Series C -- the fastest Japanese unicorn in history. The government has set a target of JPY 10 trillion per year in startup investment by FY2027, roughly 25 to 30 times the current level (Chambers & Partners). That is ambitious, but even hitting a fraction of that target would transform the ecosystem.

The Talent Flow Patterns: Where People Are Actually Moving

The capital data tells you where money goes. The talent data tells you where companies can actually be built. They are not always the same.

The AI Reconsolidation

The biggest shift in US tech talent since 2023 is the reconsolidation of AI engineers back into major hubs. During COVID, engineers dispersed to cheaper cities. Now they are moving back. SF and NYC together hold 65 percent of AI engineers at VC-backed startups (SignalFire).

This is not a general back-to-office trend. It is AI-specific. Foundation model companies need dense clusters of researchers who can whiteboard together. You cannot build GPT-5 with a fully distributed team. The physics of AI research -- fast iteration, shared compute infrastructure, constant in-person collaboration -- pulls people toward density.

For non-AI startups, the opposite is happening: distributed teams remain viable and cost-effective. But the capital follows the AI talent, which means non-AI startups in dispersed cities face a double disadvantage -- less local talent and less local capital.

Cross-Border Hiring Explosion

Deel's 2024 Global Hiring Report reveals a massive shift in how startups build teams (Deel):

- 82 percent of hires on Deel's platform were remote in 2024

- Top worker countries: US, Philippines, Argentina, India, UK

- Domestic hiring grew 104 percent; cross-border grew 42 percent

- Half of UK cross-border hires stayed within the same time zone

The most striking data point: AI trainer roles grew 283 percent cross-border in 2025, making it the fastest-growing job category in international hiring (Deel 2025). Fifty-eight percent of these trainers are in the US, 7.2 percent in India, 4.6 percent in the Philippines. The AI boom is not just creating engineering jobs -- it is creating an entirely new global job category for training and fine-tuning models.

Q1 2026: Big Tech Layoffs Are Flooding the Startup Talent Pool

This is the freshest signal in the data and arguably the most important for founders reading this right now.

In Q1 2026 alone, 55,775 tech workers were laid off across 166 companies (MedhaCloud). The biggest cuts: Oracle (20,000-30,000 planned), Meta (up to 16,000 planned), Amazon (16,000), Block (4,000), Atlassian (1,600). The pattern is consistent: companies are cutting non-AI roles to fund AI infrastructure. Meta is planning to cut up to 16,000 roles to redirect $40-50 billion into AI (InformationWeek).

Here is why this matters for the talent map: resumes from Meta, Oracle, Amazon, and Epic are flooding startup hiring pipelines at unprecedented volumes. Senior engineers with 8-10 years at top-tier companies are applying to roles they would not have considered in 2024 (KORE1).

Simultaneously, 92 percent of companies plan to hire in 2026 even as 55 percent also expect layoffs. This is not a contraction -- it is a skills rotation. The hottest role in 2026? AI Engineer, the number-one fastest-growing job according to LinkedIn (LinkedIn). Founder roles are up 69 percent year-over-year.

For startup founders: this is the best hiring window since 2009. World-class engineers who were locked into golden handcuffs at Big Tech companies are suddenly available. If you are building and can move fast, Q1-Q2 2026 is your moment.

The Fractional C-Suite

Another pattern from SignalFire's data: fractional C-suite roles are thriving. CMOs, CFOs, and CTOs working as consultants across multiple startups simultaneously.

A seed-stage company does not need a full-time CFO -- but it does need someone who can set up financial reporting, prep for a data room audit, and talk to investors. Fractional executives give startups access to senior talent at a fraction of the cost.

Meanwhile, new grad hiring collapsed 50 percent (SignalFire 2025). The entry ramp into startup life has gotten steeper for juniors -- but the pipeline of senior talent has never been richer.

What This Means for Founders

Let me translate this data into practical advice for founders deciding where to build and raise.

Where to Raise by Stage

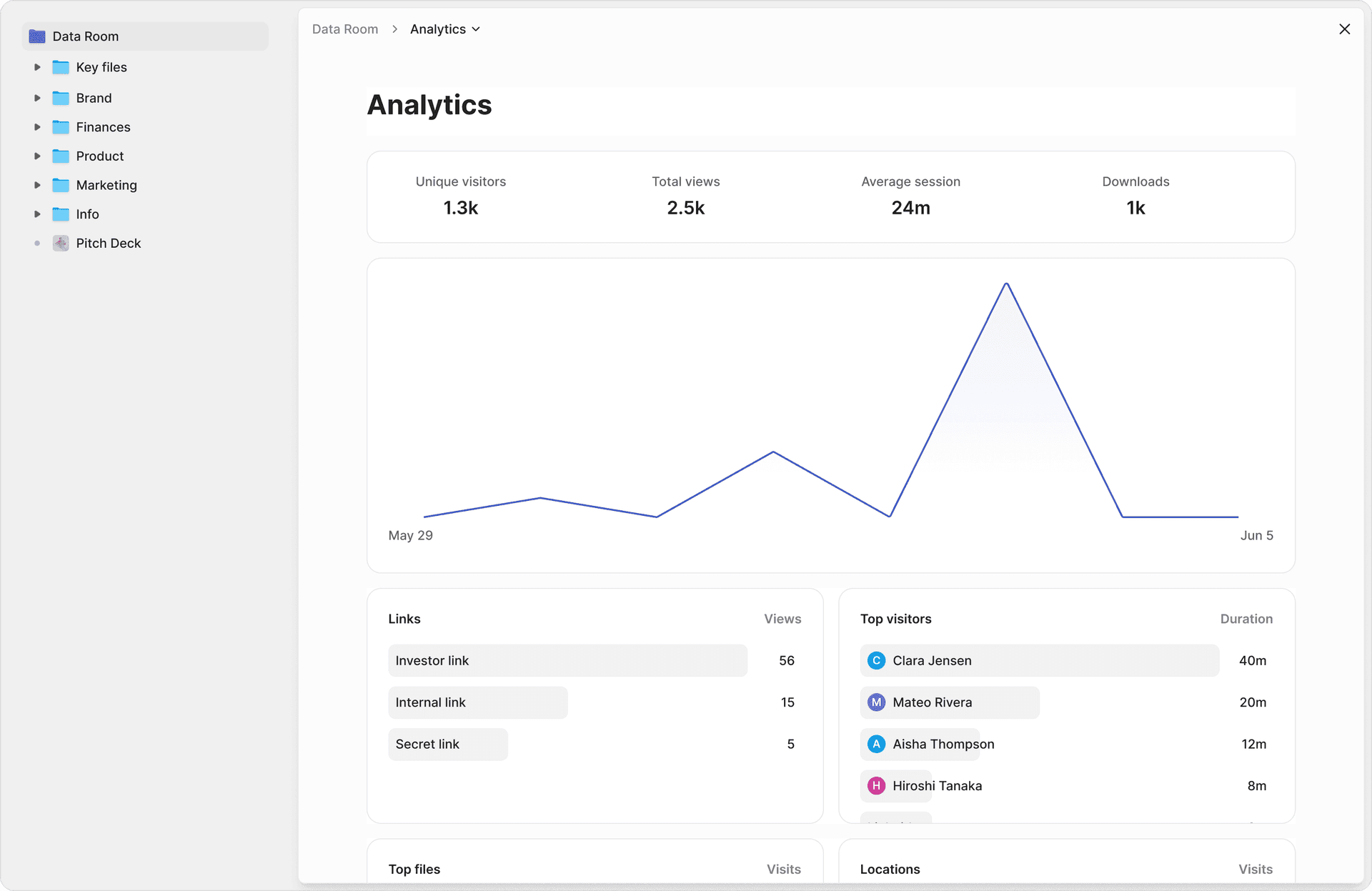

Pre-seed and seed: Geography matters less. Investors are comfortable writing sub-$3M checks over Zoom based on a pitch deck and a data room. Set up your materials in a Peony data room -- page-level analytics let you see which investors are actually reading your materials from anywhere in the world. The seed funding process does not require you to be in SF.

Series A: Geography starts to matter. Most Series A leads want at least one in-person meeting. If your target investors are SF-based (and 46 percent of VC is), plan to spend time there. But you do not need to live there. The "raise remote, build local" pattern works: pitch in SF for two weeks, then go home to Denver, Austin, or Bengaluru to build.

Series B and beyond: The capital concentration intensifies. Growth-stage deals increasingly require relationships with a small number of large funds, most headquartered in SF or NYC. Your data room complexity doubles with each round, and having organized, trackable materials becomes non-negotiable.

Cost-Adjusted Bang for Your Buck

If you are bootstrapping or running a lean seed-stage company, the per-dollar math matters enormously:

- Denver/Boulder: Strong accelerator ecosystem, 40-50 percent lower cost of living than SF, $5.0B in local VC. Best bang for buck among top-eight metros.

- Boston: If you are in biotech or deep-tech, the per capita VC density ($2,360 per capita on $16.7B total) and research institution access are unmatched. Lab space through LabCentral and Greentown Labs helps offset costs.

- Austin: Despite losing some startup talent, the cost basis is still attractive and Tesla/Oracle brought brand awareness. Best for hardware and enterprise startups.

- Bengaluru: If you can raise from US/Singapore investors and build locally, your engineering dollars go 3-5x further. The Indian accelerator ecosystem provides warm introductions to both Indian and global VCs.

The "Raise Remote, Build Local" Pattern

The dominant founder playbook in 2026 is:

- Build your product in a cost-effective city

- Set up your fundraising data room before you start outreach

- Pitch investors in SF/NYC/London through virtual meetings and trackable data room links

- Fly in for partner meetings (Series A and above)

- Use page-level analytics to identify your most engaged investors before spending money on flights

This pattern works because investors have adapted to remote diligence. The firm that invests $5M in your Series A will spend 20 hours in your data room before they ever meet you in person. What matters is whether your materials are organized, trackable, and secure -- not whether you are in the same zip code.

What This Means for VCs

Overinvested vs. Underinvested

The data reveals a clear mismatch between where capital flows and where the best risk-adjusted returns might be:

Potentially overinvested: SF for non-AI deals (valuations inflated by AI spillover), Miami (hype cycle capital without matching talent density), late-stage AI infrastructure (the compute cost arms race is getting winner-take-all).

Potentially underinvested: Boston biotech-AI intersection (the per-capita VC density suggests quality deal flow, not oversaturation), Denver-Boulder corridor (growing talent pool at lower valuations), Bengaluru and Indian metros (massive talent at sub-$10M seed valuations), Japanese deep-tech (government-backed 25x expansion target).

Emerging Ecosystems with Best Returns

For VCs looking for alpha, the most interesting ecosystems are the ones climbing the GSER rankings fastest:

- Philadelphia (+12 spots): University of Pennsylvania, Wharton, and a growing life sciences corridor. Still underpriced.

- Shenzhen (+11 spots): Hardware, robotics, manufacturing-adjacent AI. The only ecosystem on Earth where you can go from AI model to manufactured product in weeks, not months. The smartest hardware talent in the world is gravitating here -- and the robotics investor ecosystem is scaling to match.

- Bengaluru (+7 spots): The pipeline of engineering talent is a structural advantage. Valuations remain reasonable.

Cross-Border Deal Flow

The Deel data on cross-border hiring reflects a broader trend: startups are building across borders from day one. A founder in Singapore might have engineers in India, AI trainers in the Philippines, and investors in SF.

For VCs, this means portfolio companies are increasingly multi-jurisdiction from seed stage. The ability to support cross-border operations -- legal, compliance, HR, and yes, data room management for multi-party due diligence -- becomes a value-add that differentiates funds.

By the Numbers: Standalone Stats

Here are the most shareable data points from this research, sourced and ready for social media:

-

$120 billion -- OpenAI's March 2026 mega-round at an $850B valuation, the largest private funding round ever (CNBC)

-

$52 billion -- Bay Area VC in February 2026 alone, 84% of all US funding that month (AlleyWatch)

-

$339.4 billion -- US VC in 2025, up 57.6% YoY across 16,709 deals (PitchBook-NVCA)

-

65.6% -- AI's share of all US VC deal value in 2025, up from 47% in 2024 (PitchBook-NVCA)

-

65% -- Share of AI engineers at VC-backed startups in just SF and NYC (SignalFire 2025)

-

55,775 -- Tech workers laid off in Q1 2026 across 166 companies, flooding startup talent pools (MedhaCloud)

-

$177.8 billion -- Bay Area VC deal value in 2025, nearly doubling from $99.4B in 2024 (Colliers/PitchBook)

-

$2,360 -- Massachusetts VC per capita in 2025 ($16.7B / 7M residents), among the highest in the US (PitchBook via Boston Globe)

-

$15.6 billion -- Israeli startup funding in 2025, during an active military conflict (Calcalist Tech)

-

283% -- Growth in cross-border AI trainer hiring in 2025 (Deel 2025)

-

+69% -- Year-over-year growth in founder roles on LinkedIn in 2026 (LinkedIn)

-

25-30x -- Japan's government target for annual startup investment growth by FY2027 (Chambers & Partners)

Methodology Note

This analysis combines proprietary Peony data on fundraising activity across 40+ countries with seven public sources: PitchBook (US metro VC rankings, AI VC data), Crunchbase (per capita analysis, state-level VC share), SignalFire (talent migration, AI engineer concentration), Startup Genome (global ecosystem rankings), Deel (cross-border hiring), LinkedIn Economic Graph (hiring growth), and US Census Bureau (business formation). Israel data from Calcalist Tech, Japan data from IMARC and Chambers & Partners. UAE tax data from Khaleej Times and PwC. Shenzhen government subsidy data from official municipal announcements.

All data represents the most recent publicly available figures as of March 2026. Peony engagement data is aggregated and anonymized.

Set Up Your Fundraising Data Room

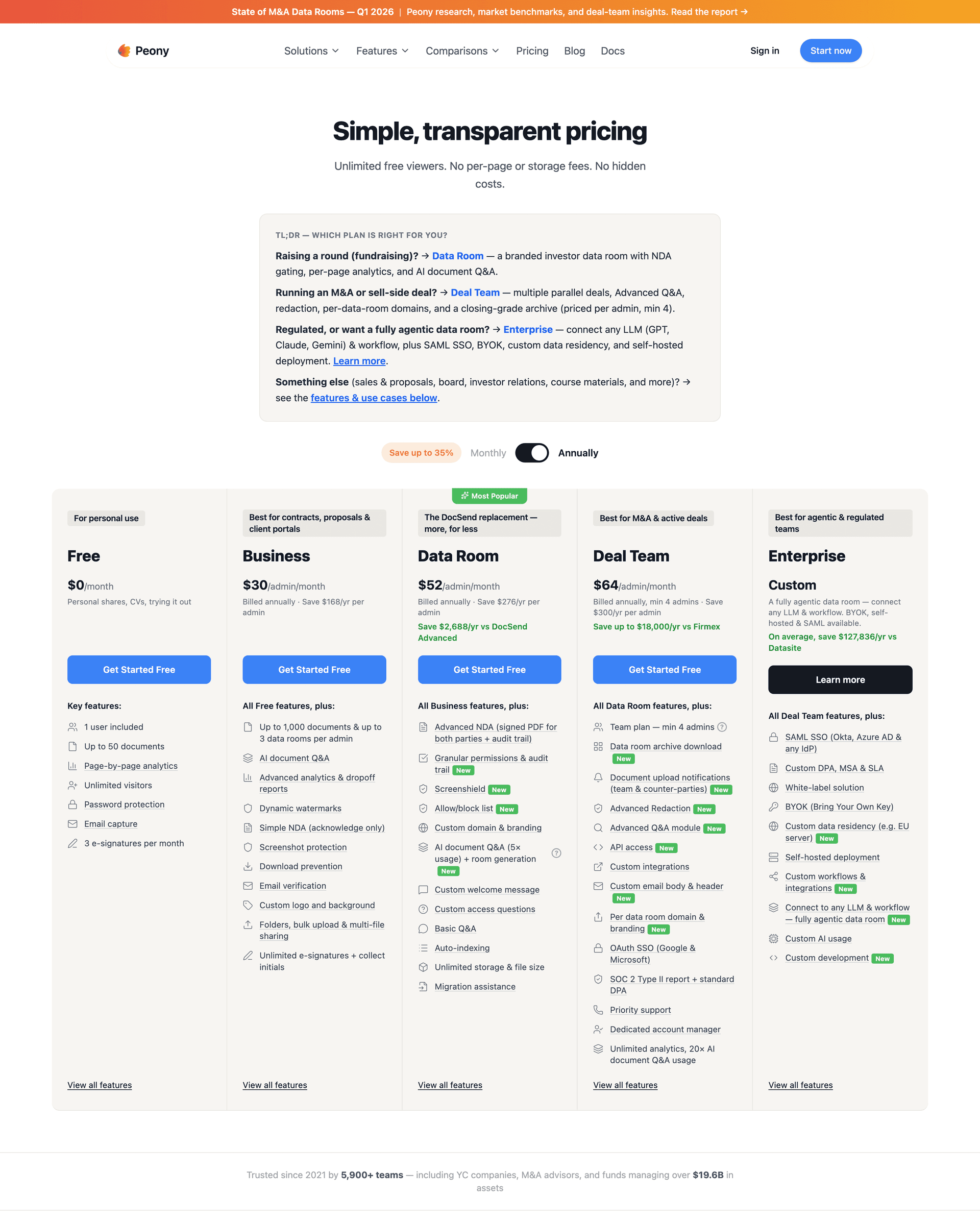

Wherever you are building -- SF, Shenzhen, or anywhere between -- the fundraising process starts with your materials. Peony helps founders in 40+ countries organize their data rooms in under 5 minutes with AI auto-indexing, track investor engagement with page-level analytics that show which pages each reviewer read and for how long, and protect sensitive documents with dynamic watermarks and screenshot protection.

The free tier includes 2 GB storage, page-level analytics, and security controls. No credit card required.

Frequently Asked Questions

Which US city receives the most venture capital funding?

The San Jose-San Francisco-Oakland metro area received $177.8 billion in VC deal value in 2025, nearly doubling from $99.4 billion in 2024. New York came in second at $33.5 billion and Boston third at $16.7 billion. If you are raising in any of these metros, set up your fundraising data room with Peony to organize materials in under 5 minutes and track which investors engage most through page-level analytics.

What percentage of global VC goes to AI startups?

AI captured 65.6 percent of all US venture capital deal value in 2025, totaling $222 billion out of $339.4 billion according to PitchBook-NVCA. Globally, the OECD estimates AI's share at 61 percent. In February 2026, AI captured 90 percent of a record $189 billion monthly total. Founders building AI companies can use Peony data rooms to share technical documentation and model benchmarks with investors through secure, trackable links with screenshot protection.

Where are AI engineers concentrating in the US?

San Francisco and New York City together employ 65 percent of AI engineers at VC-backed startups according to SignalFire's 2025 State of Talent report. This reconsolidation toward major hubs reversed the pandemic-era trend of dispersed remote work. Peony page-level analytics help distributed AI teams share investor materials across time zones and see exactly which documents drive the most engagement.

Which city has the highest venture capital per capita?

Massachusetts attracted $16.7 billion in venture capital in 2025, roughly $2,360 per capita, among the highest in the nation for a state of just 7 million residents. Boston's concentration of biotech, life sciences, and AI research institutions drives this outsized ratio. Founders raising in Boston can use a Peony data room to organize complex technical validation data and track reviewer engagement at the page level.

What are the fastest-rising global startup ecosystems in 2025?

According to the Startup Genome GSER 2025 rankings, the fastest climbers include Hangzhou at plus 13 spots, Philadelphia at plus 12, Shenzhen at plus 11, and Bengaluru at plus 7. Shenzhen is attracting the smartest hardware and robotics talent globally thanks to its unmatched supply chain of 74,000 robotics enterprises and a $630 million government AI subsidy. Peony supports data rooms for fundraising in 40+ countries with AI auto-indexing that organizes documents in under 3 minutes regardless of language.

Is Miami a good city for startups in 2026?

Miami shows a split signal. VC deal value was $3.6 billion in 2024, ranking seventh among US metros, and AI roles grew 12 percent year-over-year. However, Florida is losing overall VC share according to Carta data, and the ecosystem lacks the deep talent density of SF, NYC, or Boston. Miami works best for founders who want tax advantages and quality of life while raising from investors elsewhere. Set up a Peony data room to share materials with out-of-state VCs and track engagement remotely.

What is the AI trainer hiring trend?

Cross-border AI trainer roles grew 283 percent in 2025 according to Deel's Global Hiring Report, making it the fastest-growing job category in cross-border hiring. Fifty-eight percent of AI trainers are based in the US, with India at 7.2 percent and the Philippines at 4.6 percent. AI companies scaling their trainer workforces can use Peony data rooms to share onboarding materials, NDAs, and compliance documents across borders with built-in e-signatures and NDA gates.

Should I raise capital where I build my startup?

Not necessarily. The dominant pattern in 2026 is raise remote, build local. Founders increasingly pitch investors in SF, NYC, or London through virtual meetings and trackable data rooms while building their teams in lower-cost metros like Denver, Austin, or Bengaluru. Peony makes this seamless with personalized sharing links, page-level analytics, and dynamic watermarks that work regardless of geography.

Related Resources

- Seed Funding for Startups: What 200+ Data Rooms Taught Me

- Startup Fundraising Rounds Explained (Seed to Series C)

- Data Room for Investors: The Complete Setup Guide

- 15 Best US Seed Investors

- 12 Best Startup Accelerators in Boston

- 12 Best Startup Accelerators in Austin

- 10 Best Startup Accelerators in Colorado

- Top Startup Accelerators in India

- Robotics Investors in Shenzhen

- 15 Robotics VCs in the US

- Peony Solutions: Fundraising

- Peony Solutions: Venture Capital

- Peony Features: Data Rooms

- Peony Features: Page-Level Analytics

You might also like

Jun 26, 2026

Venture Debt Data Room: Why Lenders Underwrite the Floor, Not the Ceiling (2026)

Jun 25, 2026

Series A Data Room: The Step-Change Round Where Your Room Gets Graded (2026)

May 27, 2026

10 Fundraising Data Room Mistakes Sophisticated Bidders See in 2026