Top 12 Chip Investors in 2026: Cerebras $5.55B IPO and +68% Day-1 Open the Cycle

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Top 12 Chip Investors in 2026: Cerebras $5.55B IPO and +68% Day-1 Open the Cycle

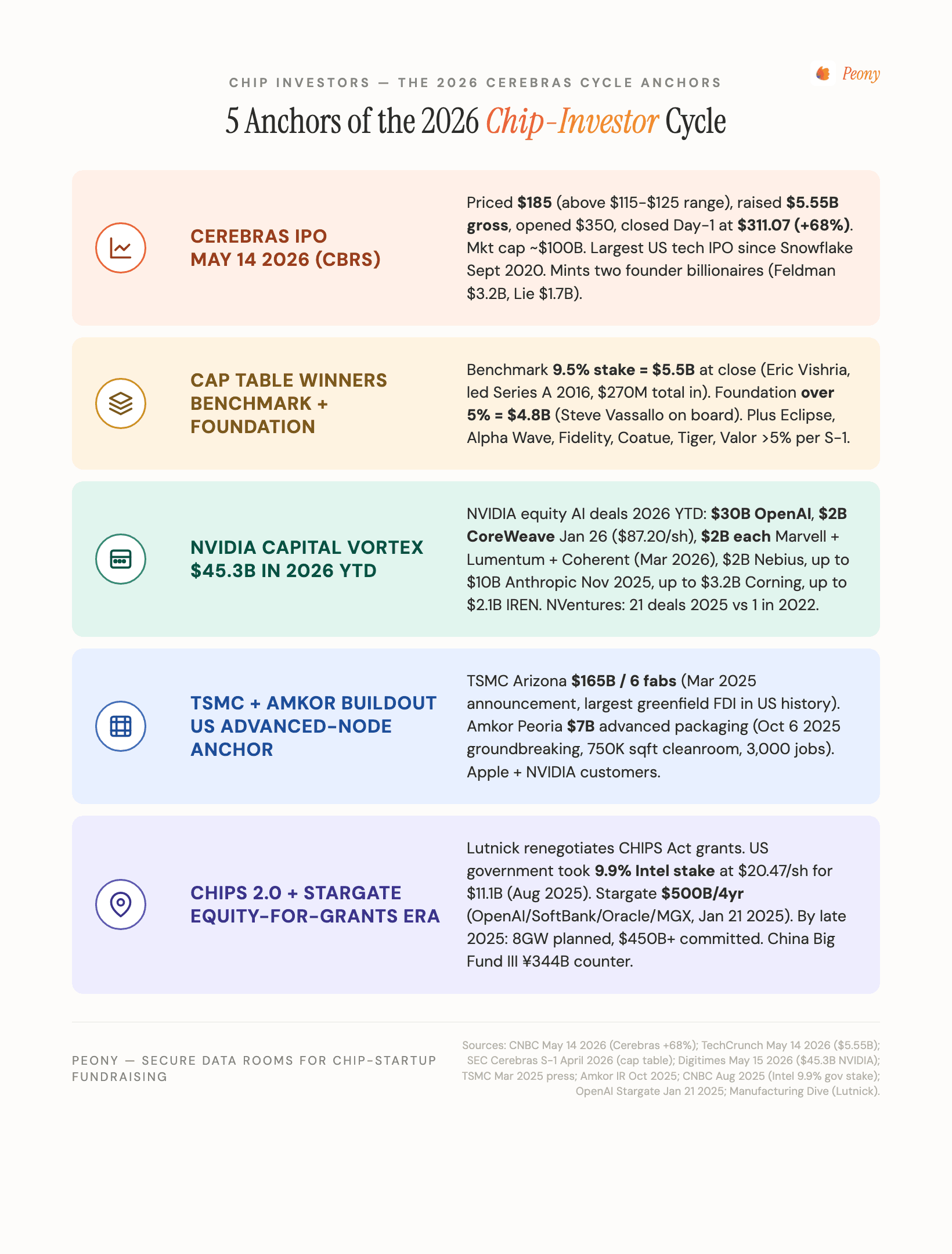

Quick answer: The 12 most active chip investors in 2026 split across four tiers. Top-tier early VCs that follow on: Benchmark (9.5 percent Cerebras stake worth $5.5B at May 14 close per CNBC), Foundation Capital (over 5 percent Cerebras stake worth $4.8B, Steve Vassallo on board), Eclipse Ventures (Cerebras Series A 2016, Lior Susan). Mega generalist VCs and crossover funds: Andreessen Horowitz (a16z, $15B new funds early 2026, co-led $475M Unconventional seed at $4.5B with Lightspeed), Coatue Management (led Cerebras Series B Dec 2016, Series D, and Series H Feb 2026 participant), Tiger Global (led $1B Cerebras Series H Feb 2026 at $89 per share, paper gain approximately $3.5B at IPO close). Corporate strategics: NVIDIA / NVentures ($45.3 billion equity AI deals 2026 YTD, including $30B OpenAI, $2B CoreWeave, $2B Marvell, $2B each Lumentum and Coherent), Intel Capital ($20B+ lifetime AUM, led SambaNova $35M+$15M February-April 2026 plus Ayar Labs $155M, currently spinning out as independent fund), Samsung Catalyst Fund (72 portfolio investments, led Normal Computing $50M March 2026, co-led Eliyan $60M Series B March 2024), Qualcomm Ventures (382 lifetime portfolio companies, 24 unicorns, joined India Deep Tech Alliance second wave November 2025). Specialist deep-tech: Walden Catalyst Ventures ($550M deep-tech fund, founded by Lip-Bu Tan before his appointment as Intel CEO effective March 18 2025), Celesta Capital ($1.1B AUM across 100+ investments since 2013, portfolio includes Credo over $25B market cap and Eliyan). The 2026 chip-investor cycle was catalyzed by Cerebras IPO May 13-14 2026 — priced $185 per share above the upsized $150-$160 marketed range (originally $115-$125, bumped May 11), raised $5.55B gross, opened $350, closed Day-1 at $311.07 (+68 percent), market cap approximately $95B (intraday peak briefly approached $100B), 20x oversubscribed, largest US technology IPO in nearly six years, minted two founder billionaires (CEO Andrew Feldman $3.2B, CTO Sean Lie $1.7B).

The 2026 chip-investor cycle has a clear starting gun: Cerebras Systems priced its IPO at $185 per share on the evening of May 13 2026 — above the upsized $150-$160 marketed range (the range was bumped May 11 from the original $115-$125) — for 30 million Class A shares, raising $5.55 billion gross (up to $6.33B if the underwriter greenshoe is exercised). Shares opened at $350 on Nasdaq under the ticker CBRS the morning of May 14 2026 and closed Day-1 at $311.07 (+68 percent from IPO price) giving a $95B market cap at close per CNBC's coverage and TechCrunch's analysis. The roadshow was 20x oversubscribed. This is the largest US technology IPO in nearly six years.

I have spent years on the investor side at Backed VC and Target Global before co-founding Peony — a data room platform now used by 5,900+ customers including chip-startup founders running parallel investor processes across the corporate strategic, financial VC, and sovereign tiers. This guide is the working map of who is actually writing checks, what they look for, and how the Cerebras IPO catalyst reshapes the syndicate construction calculus for chip founders in the next 12 months.

TL;DR: Cerebras priced $185 per share above the upsized $150-$160 range (originally $115-$125, bumped May 11), raised $5.55 billion gross, opened $350, closed Day-1 at $311.07 (+68 percent), $95B market cap at close (intraday peak briefly approached $100B), 20x oversubscribed — largest US technology IPO in nearly six years (CNBC, TechCrunch). The cap table winners are Benchmark (9.5 percent stake worth $5.5B at close) and Foundation Capital (over 5 percent worth $4.8B) with Eclipse, Alpha Wave, Fidelity, Coatue, Tiger, Valor, Altimeter, AMD also greater-than-5-percent holders per S-1. NVIDIA committed $45.3B to equity AI deals in 2026 YTD including $30B OpenAI, $2B CoreWeave, $2B Marvell, $2B each Lumentum and Coherent, $2B Nebius, up to $10B Anthropic — the NVIDIA Capital Vortex now eclipses every traditional corporate-strategic chip program (Digitimes May 15 2026). The 12 firms below collectively touch over $400 billion of 2026 chip-and-AI-hardware deployable capital against the $255.5B Q1 2026 AI venture funding total (exceeding full-year 2025's $254.4B in a single quarter per PitchBook). If you are a chip founder raising Series A through C, these are the firms to target — and having a secure data room ready before the first call is table stakes given the customer-concentration and IP-disclosure sensitivity of chip IP.

Why does this chip-investor list matter now? The Cerebras IPO catalyst

Three structural forces converged between Q4 2025 and Q2 2026 that reshape chip-investor decision-making in 2026:

1. Cerebras IPO validates the inference-cycle thesis. Cerebras' S-1 (filed April 2026, available on SEC.gov) disclosed 2025 revenue around $510 million with concentration of 24 percent from G42 (down from 85 percent in 2024) and 62 percent from MBZUAI — combined UAE customer concentration of 86 percent — plus a multi-year OpenAI compute contract worth over $10 billion. The market priced this at a $56.4B fully diluted valuation at $185 and accepted concentration risk in exchange for inference-cycle thesis exposure. PitchBook's senior research analyst Dimitri Zabelin framed the moment: the rotation from training-cycle dominance toward inference-cycle scaling is now the deciding axis of competitive positioning for AI hardware.

2. The NVIDIA Capital Vortex. NVIDIA committed $45.3 billion to equity AI deals in 2026 YTD per Digitimes May 15 2026 — eclipsing every traditional corporate-strategic chip program in history. The component deals: $30B in OpenAI (2026), $2B in CoreWeave at $87.20 per share (January 26 2026), $2B in Marvell for silicon-photonics partnership (March 2026), $2B in Lumentum, $2B in Coherent, $2B in Nebius Group, up to $10B in Anthropic (November 2025 alongside Microsoft's $5B), up to $3.2B in Corning, up to $2.1B in IREN. NVIDIA NVentures specifically (the corporate VC arm) did 21 deals in 2025 per TechCrunch (or 30 deals per PitchBook — sources conflict) versus just 1 in 2022. Portfolio highlights include PsiQuantum (Sept 2025 $1B Series E), SiFive (April 2026 $400M Series G), Figure AI, Wayve, Lambda, CoreWeave, Ayar Labs, Commonwealth Fusion, and Scale AI.

3. The CHIPS Act 2.0 reorientation under Trump-Lutnick. Commerce Secretary Howard Lutnick has been renegotiating CHIPS Act grant agreements, pushing federal funding to roughly 4 percent or less of total project value per Manufacturing Dive's reporting. The structural precedent: the US government acquired a 9.9 percent stake in Intel at $20.47 per share for $8.9 billion in equity in August 2025 (with $2.2 billion in prior CHIPS Act grants counted toward the $11.1 billion total Trump-Intel commitment per Intel's press release) — converting CHIPS Act grants to equity. Natcast was shut down in August 2025, a $325M NIST budget cut was proposed, and Stargate Project ($500B over 4 years from OpenAI plus SoftBank plus Oracle plus MGX, announced January 21 2025) emerged as the private-sector mega-infrastructure alternative. By late 2025, Stargate had 8GW planned capacity and over $450B committed across 9 sites.

Frame: The Inference-Cycle Pivot. Until late 2024, the dominant chip-VC thesis was training-cycle compute — large clusters, frontier-model training, capital intensity in the multi-billion-dollar range. The 2025 catalyzing reversal: inference-cycle scaling (token generation speed and cost per query) now determines competitive positioning, because inference workloads run continuously at production scale while training is episodic. Cerebras' wafer-scale architecture is the canonical inference-cycle bet. The implication for investor selection: firms with explicit inference-cycle theses (Coatue, Tiger Global, Atreides Management, Valor Equity Partners, plus the NVIDIA Capital Vortex) are pricing differently than legacy training-cycle backers.

Quick Reference Table

| Investor | Type | HQ | Stage | Estimated Check | Key Chip Portfolio Hits |

|---|---|---|---|---|---|

| Benchmark | Top-tier early VC | San Francisco | Series A-C | $10M-$50M | Cerebras 9.5% stake $5.5B at IPO close |

| Foundation Capital | Top-tier early VC | Palo Alto | Seed-Series B | $5M-$30M | Cerebras over 5% stake $4.8B at IPO close |

| Eclipse Ventures | Specialist hardware | San Francisco | Seed-Series B | $5M-$30M | Cerebras Series A 2016, VulcanForms, AheadComputing |

| Andreessen Horowitz (a16z) | Mega generalist | Menlo Park | Multi-stage | $5M-$200M+ | Co-led $475M Unconventional seed at $4.5B (with Lightspeed) |

| Coatue Management | Growth/crossover | New York | Series B-pre-IPO | $50M-$500M+ | Cerebras Series B/D/H, NVIDIA-cycle infrastructure |

| Tiger Global | Growth/crossover | New York | Series C-pre-IPO | $100M-$1B+ | Led Cerebras $1B Series H Feb 2026 at $89/share |

| NVIDIA / NVentures | Corporate strategic | Santa Clara | Series A-pre-IPO | $1M-$30B | $45.3B 2026 YTD: OpenAI/CoreWeave/Marvell/Lumentum/Coherent |

| Intel Capital | Corporate strategic | Santa Clara | Seed-Series E | $1M-$50M | SambaNova $35M+$15M, Ayar Labs $155M, Astera Labs exit |

| Samsung Catalyst Fund | Corporate strategic | Mountain View | Series A-Series D | $5M-$50M | Led Normal Computing $50M, co-led Eliyan $60M Series B |

| Qualcomm Ventures | Corporate strategic | San Diego | Seed-Series C | $1M-$25M | 382 portfolio, 24 unicorns, joined India Deep Tech Alliance Nov 2025 |

| Walden Catalyst Ventures | Specialist deep tech | San Francisco / Tel Aviv | Seed-Series A | $1M-$10M | $550M fund 2021; Lip-Bu Tan founding GP (now Intel CEO) |

| Celesta Capital | Specialist deep tech | Palo Alto | Series A-Series C | $5M-$25M | Credo over $25B mkt cap, Eliyan, IDTA founding member 2025 |

Before reaching out to any of these firms, organize your chip-startup data room with Peony. Our AI auto-indexing structures silicon roadmap, IP docket, customer NDAs, fab agreements, and export-control compliance documentation in under 3 minutes, and page-level analytics show you exactly which partner spent time on which page — so you know who to follow up with first.

Frame: The Cerebras Cap Table — who actually won the $15B+ Day-1 paper gain

The Cerebras S-1 disclosed the greater-than-5-percent stakeholders, and the May 14 2026 close at $311.07 produced the largest VC chip win in modern history. The cap-table winners ranked by paper gain at Day-1 close:

- Benchmark — 9.5 percent stake worth $5.5B at close per CNBC's coverage. Eric Vishria led the $25M Series A in 2016. Benchmark invested approximately $270M total across rounds ($18M early plus $250M later), generating an estimated 20x-plus paper return. Per Vishria's own admission to TechCrunch, Benchmark "almost didn't take the meeting" — a humbling reminder that even top-tier early VCs nearly miss generational chip wins.

- Foundation Capital — over 5 percent stake worth $4.8B at IPO per Whatfinger / Steve Vassallo profile. Vassallo sits on the Cerebras board and was the Series A co-lead alongside Benchmark.

- Eclipse Ventures — over 5 percent stake (exact equity not publicly disclosed). Lior Susan led Eclipse's Cerebras Series A participation in 2016 and Eclipse is listed as a named over-5-percent shareholder per S-1.

- Alpha Wave — over 5 percent stake. Rick Gerson led the $250M Series F November 2021 at over $4B valuation alongside Abu Dhabi Growth Fund.

- Fidelity — over 5 percent stake through later-round participation.

- Coatue Management — led Series B December 2016 and participated in Series D November 2018, then participated in $1B Series H February 2026 at $23B valuation.

- Tiger Global — led the $1B Series H February 2026 at $89 per share. At the IPO close of $311.07, Tiger's $1B converts to approximately $3.5B paper value — a 3.5x mark-up in roughly 3 months.

- Valor Equity Partners — over 5 percent stake; tied most-active disclosed AI chip investor with 3 deals over trailing 12 months including Groq and both Positron rounds.

- Altimeter, AMD, 1789 Capital, Abu Dhabi Growth Fund, G42 — all in the cap table at various sizes.

Founder paper-billionaire creation: CEO Andrew Feldman ($3.2B stake at close) and CTO Sean Lie ($1.7B stake at close) became billionaires May 14 2026 per CNBC. Both were among 5 co-founders ex-SeaMicro (which sold to AMD).

The lessons for early-stage chip investors: (1) conviction at Series A in deep-tech founders who have shipped silicon at scale produces 20x-plus returns when the inference cycle hits; (2) strategic customer concentration (G42 plus MBZUAI combined 86 percent of 2025 revenue per S-1) carries diligence risk but does not preclude IPO; (3) the 5-co-founder ex-SeaMicro team shows that prior-sold-to-AMD founder DNA is a pattern worth indexing.

The 12 verified chip investors

1. Benchmark

- Type: Top-tier early-stage VC

- HQ: San Francisco

- Lead chip partners: Eric Vishria (Cerebras board, led Series A 2016)

- Stage focus: Series A through C with conviction follow-on

- Estimated check: $10M-$50M Series A, $25M-$150M follow-on

- Most recent chip headline: Cerebras 9.5 percent stake worth $5.5B at May 14 2026 close — largest single VC chip win in modern history per CNBC analysis. Total invested approximately $270M across rounds.

- Why hire them: The conviction-and-follow-on archetype for chip investing. Benchmark's small partnership structure (no team scaling, no fund-of-funds layer) translates to direct senior-partner relationships through every round.

2. Foundation Capital

- Type: Top-tier early-stage VC

- HQ: Palo Alto

- Lead chip partners: Steve Vassallo (General Partner, Cerebras board)

- Stage focus: Seed through Series B

- Estimated check: $5M-$30M

- Most recent chip headline: Cerebras over 5 percent stake worth $4.8B at IPO close per Whatfinger / CNBC. Vassallo on Cerebras board.

- Why hire them: Foundation has a sustained chip and frontier-hardware thesis. The Cerebras outcome strengthens Vassallo's posture in any 2026 chip-startup conversation.

3. Eclipse Ventures

- Type: Specialist hardware and industrial-tech VC

- HQ: San Francisco

- Lead chip partners: Lior Susan (Founding Partner, Cerebras backer)

- Active portfolio: 96 active companies per CB Insights December 2025, 218 lifetime investments

- Stage focus: Seed through Series B

- Estimated check: $5M-$30M

- Most recent chip headline: Cerebras Series A 2016 (over-5-percent S-1 stakeholder at IPO); active in AheadComputing, VulcanForms

- Why hire them: The clearest hardware-specialist brand in the US chip-VC universe. Susan's posture is "build hard things from scratch" which is the founder-fit screen Cerebras passed.

4. Andreessen Horowitz (a16z)

- Type: Mega generalist VC

- HQ: Menlo Park

- Lead chip partners: Multiple GPs across the Infrastructure and American Dynamism funds

- Recent fund: $15 billion new funds raised early 2026 (largest ever haul) per Crunchbase News — includes $1.7B Infrastructure fund and $1.176B American Dynamism

- Portfolio: 1,076 portfolio companies; 186 investments in 2025

- Stage focus: Multi-stage from seed to pre-IPO

- Estimated check: $5M-$200M+

- Most recent chip headline: Co-led $475M seed round in Unconventional at $4.5B valuation (Naveen Rao, ex-Databricks) building probabilistic AI chips per Inc. Magazine, alongside Lightspeed Venture Partners as co-lead; co-led Anduril $5B round at $61B valuation with Thrive Capital (closed May 13 2026); one of top-3 firms leading billion-dollar AI rounds in 2025 alongside Lightspeed and Founders Fund per CB analysis.

- Why hire them: Capital depth and brand pull for capital-intensive chip rounds. The American Dynamism and Infrastructure funds give a16z explicit chip-and-defense theses.

5. Coatue Management

- Type: Growth and crossover fund

- HQ: New York

- Stage focus: Series B through pre-IPO and public

- Estimated check: $50M-$500M+

- Most recent chip headline: Led Cerebras Series B December 2016, participated in Series D November 2018, then participated in $1B Series H February 2026 at $23B valuation. Multi-year holder through public market.

- Why hire them: Coatue's NVIDIA-cycle infrastructure thesis treats AI hardware as a sustained allocation, not a tactical bet. Mike Volpi and the crossover team move fast on growth chip rounds.

6. Tiger Global Management

- Type: Growth and crossover fund

- HQ: New York

- Stage focus: Series C through pre-IPO and public

- Estimated check: $100M-$1B+

- Most recent chip headline: Led the $1B Cerebras Series H February 2026 at $89 per share (with Benchmark, Fidelity, Altimeter, AMD, Coatue, Valor Equity, 1789 Capital, Alpha Wave participating). At the IPO close of $311.07, Tiger's $1B converts to approximately $3.5B paper value — a 3.5x mark-up in three months. Co-led Eliyan $60M Series B chiplet-interconnect round (March 2024) with Samsung Catalyst.

- Why hire them: Tiger's appetite for chip growth rounds is now backed by the live Cerebras case study. Expect Tiger to lead at least 2-3 additional chip pre-IPO mega-rounds in the next 12 months.

7. NVIDIA / NVentures

- Type: Corporate strategic (parent public-co plus NVentures corporate VC arm)

- HQ: Santa Clara

- 2026 YTD AI-equity commitments: $45.3 billion per Digitimes May 15 2026 — including $30B OpenAI (2026), $2B CoreWeave at $87.20 per share January 26 2026, $2B Marvell for silicon-photonics March 2026, $2B each Lumentum and Coherent March 2026, $2B Nebius Group, up to $10B Anthropic November 2025, up to $3.2B Corning, up to $2.1B IREN

- NVentures deal volume: 21 deals in 2025 per TechCrunch (or 30 per PitchBook — sources conflict) versus 1 in 2022

- Portfolio: PsiQuantum (Sept 2025 $1B Series E), SiFive (April 2026 $400M Series G), Figure AI, Wayve, Lambda, CoreWeave, Ayar Labs, Commonwealth Fusion, Scale AI

- Most recent chip headline: $45.3B 2026 YTD — the NVIDIA Capital Vortex eclipses every traditional corporate-strategic chip program in history.

- Why hire them: NVIDIA's strategic-customer plus capital combination is unmatched. The structural caveat: NVIDIA strategics introduce competitive-positioning constraints if your chip company sells into NVIDIA's customer base.

8. Intel Capital

- Type: Corporate strategic (in process of spinning out as independent fund)

- HQ: Santa Clara

- Lifetime AUM: $20B+ deployed; approximately $400M new and follow-on in 2024

- Stage focus: Seed through Series E

- Estimated check: $1M-$50M

- Most recent chip headlines: Invested $35M in SambaNova February 2026 taking stake to 8.2 percent, then additional $15M in April 2026 taking ownership to 9 percent; led Ayar Labs $155M financing at over $1B valuation (silicon photonics); co-led RunPod $20M seed with Dell Technologies Capital; participated in Scale AI $1B Series F at approximately $14B valuation.

- Portfolio exit: Astera Labs (ALAB) IPO 2024 — all-time high $262.90 September 18 2025, trading at $199.79 on May 8 2026; FY2025 revenue $852.5M (+115 percent YoY); Q1 2026 revenue $308.4M (+93 percent YoY).

- Why hire them: Intel Capital's spinning-out-as-independent posture frees the team from Intel parent strategic conflicts and gives them a clean cap-table profile for chip founders. The Astera Labs IPO 2024 success is the live precedent that Intel Capital's portfolio matures to public exits.

9. Samsung Catalyst Fund

- Type: Corporate strategic

- HQ: Mountain View (US headquarters of Samsung's strategic investment arm)

- Portfolio: 72 investments to date

- Stage focus: Series A through Series D

- Estimated check: $5M-$50M

- Most recent chip headlines: Led Normal Computing $50M March 2026 for thermodynamic AI chips; Teramount $50M July 2025 for optical interconnect; participated in Groq Series E $750M September 17 2025; co-led Eliyan $60M Series B (chiplet interconnect taped out on Samsung 4nm node) with Tiger Global in March 2024.

- Parent context: Samsung announced $73B semiconductor investment plan for 2026 amid HBM demand surge.

- Why hire them: Samsung Catalyst is the strongest corporate-strategic for advanced packaging, chiplet interconnect, and HBM-adjacent companies. Direct fab-access value-add for portfolio companies needing Samsung 4nm or 3nm tape-out partnerships.

10. Qualcomm Ventures

- Type: Corporate strategic

- HQ: San Diego

- Portfolio: 382 lifetime portfolio companies (28-year history), 24 unicorns, 16 investments in 2025 plus 4 in 2026 YTD per Tracxn

- Stage focus: Seed through Series C

- Estimated check: $1M-$25M

- Most recent strategic move: Joined the India Deep Tech Alliance second wave November 2025 alongside NVIDIA (Celesta Capital spearheaded the September 2025 founding cohort) — committing to a 5-10 year semiconductor and quantum capital allocation

- Why hire them: Qualcomm Ventures is the strongest corporate-strategic for mobile compute, RF, modem, and India-market chip companies. The India Deep Tech Alliance (where Qualcomm joined the second-wave November 2025 cohort with NVIDIA) provides a parallel growth-capital channel to the US-dominant venture ecosystem.

11. Walden Catalyst Ventures

- Type: Specialist deep-tech VC (US, Europe, Israel)

- HQ: San Francisco and Tel Aviv

- Fund size: $550M raised November 2021 for early-stage deep tech

- Stage focus: Seed through Series A

- Estimated check: $1M-$10M

- Note on Lip-Bu Tan: Walden Catalyst's founding Managing Partner Lip-Bu Tan was appointed Intel CEO effective March 18 2025 — Walden Catalyst continues as a fund but Tan's day-to-day involvement is now at Intel where he has executed 35,500 total job cuts (15K prior management plus 20,500 under his tenure) targeting headcount of approximately 75,000 by end-2026.

- Related context: Tan's Walden International (separate from Catalyst) has a 600+ company history and over $5B deployed lifetime — including seeded SMIC and 100+ China deals (subject of 2025 controversy).

- Why hire them: Walden Catalyst is the deep-tech specialist with the longest founding-team chip operating experience. Even post-Tan-to-Intel transition, the team retains the chip-company-building playbook.

12. Celesta Capital

- Type: Specialist deep-tech and chip VC

- HQ: Palo Alto

- AUM: $1.1 billion across 100+ investments since 2013

- Stage focus: Series A through Series C

- Estimated check: $5M-$25M

- Portfolio highlights: Credo (over $25B market cap, public), Eliyan (chiplet interconnect, taped out Samsung 4nm, raised $60M Series B March 2024 co-led with Samsung Catalyst plus Tiger Global), Atonarp, Recogni ($102M Series C closed February 2024 led by Celesta plus GreatPoint Ventures). Celesta also spearheaded the India Deep Tech Alliance launch in September 2025 at SEMICON India with founding investors Accel, Blume, Premji Invest, Gaja Capital, Ideaspring, Tenacity, and Venture Catalysts.

- Why hire them: Celesta is the clearest pure-specialist chip-VC brand in the US — the team has deep semis backgrounds and explicitly does not generalize into AI applications. For chiplet interconnect, EDA tools, and intelligent systems companies, Celesta is a natural lead.

Frame: The NVIDIA Capital Vortex reshapes corporate-strategic chip investing

NVIDIA's $45.3 billion in equity AI investments committed in 2026 YTD per Digitimes is structurally different from any prior corporate-strategic chip program. The component flows form a self-reinforcing vortex: NVIDIA invests in AI compute customers (OpenAI $30B, Anthropic up to $10B with Microsoft's $5B); those customers commit to NVIDIA chip purchases (Anthropic's $30B Azure compute purchases including up to 1GW NVIDIA Grace Blackwell/Vera Rubin); NVIDIA invests in the data-center infrastructure layer (CoreWeave $2B at $87.20 per share January 26 2026, expanding 5GW AI-factory buildout; IREN up to $2.1B); NVIDIA invests in the silicon-photonics and optical-interconnect layer that solves the post-electrical-interconnect bottleneck (Marvell $2B March 2026, Lumentum $2B, Coherent $2B); NVIDIA invests in the materials layer (Corning up to $3.2B). The result: a chip-investor flywheel that operates at scale rivaling sovereign-fund deployment.

For chip founders, the practical implication: NVIDIA NVentures should be modeled as a customer-and-investor combined rather than a pure financial backer. The strategic-customer reference value can be the difference between a credible Series B and a stalled round, but the customer-concentration disclosure (Cerebras' G42-plus-MBZUAI 86 percent of 2025 revenue is the canonical comparison) must be modeled explicitly in the data room.

Frame: The Inference-Cycle Pivot — why training-cycle backers may underperform 2026-27

PitchBook's senior research analyst Dimitri Zabelin framed the moment: the rotation from training-cycle dominance toward inference-cycle scaling is now the deciding axis. Training-cycle bets (large-scale clusters, frontier-model training) are episodic capital intensity — they spike for 6-12 months around model releases and then idle. Inference-cycle bets (token generation speed, cost per query) are continuous capital intensity — they run at production scale 24/7.

The implications for chip-investor selection:

- Inference-cycle specialists (Cerebras with wafer-scale architecture, Groq with LPU, SambaNova with Reconfigurable Dataflow Unit, Tenstorrent with Wormhole architecture) attract concentration capital

- Training-cycle backers without inference-cycle pivot risk are now in a structural headwind through 2027

- Inference economics (token-per-watt-per-dollar versus NVIDIA H100/B100/B200/GB300 benchmarks) becomes the universal Series B-C diligence question

Active firms positioned for the inference-cycle: Tiger Global, Atreides Management, Valor Equity Partners, Coatue, plus the NVIDIA Capital Vortex itself. Chip founders should explicitly frame inference economics in pitch materials and ensure data room sections cover token generation speed, cost per query, watt-per-token, and competitive benchmarks against the most recent NVIDIA Hopper-and-Blackwell baselines.

Honorable mentions (the bench beyond the top 12)

These firms did not make the named top-12 cut but consistently show up in chip syndicates and warrant founder targeting:

- In-Q-Tel (CIA-backed; 800+ startups backed lifetime; 500+ tech transitions; chip-relevant 2026 EDA tools focus per their year-ahead memo)

- Founders Fund ($6B growth fund closed May 2025; $1B in Anduril; $1.25B in Anthropic; participates in chip-adjacent defense plays)

- Lightspeed Venture Partners (top-3 firm for billion-dollar AI rounds in 2025; led Ricursive $300M Series A January 2026 at $4B valuation)

- Atreides Management (most-active disclosed AI chip investor with 3 deals in 12 months including Cerebras and both Positron rounds; led SiFive $400M Series G April 9 2026 at $3.65B valuation)

- Valor Equity Partners (tied most-active AI chip investor at 3 deals; greater-than-5-percent Cerebras stakeholder per S-1)

- Khosla Ventures ($3.5B raised across 3 funds early 2025; AI fund vehicle approximately $405M March 2025; 104 investments in 2025)

- Sequoia Capital ($7B late-stage fund closed April 2026; led Ricursive Intelligence seed at $750M valuation, chip AI co-founded by ex-DeepMind AlphaChip team)

- 1789 Capital (active in Cerebras Series H and multiple AI chip rounds)

- Fidelity, BlackRock, Temasek, Baillie Gifford, T. Rowe Price (crossover and public-market participants in Cerebras Series F+ and PsiQuantum Series E)

- G42, Saudi PIF, Qatar Investment Authority, Mirae Asset, Korea Development Bank (sovereign anchors)

- China Big Fund III (¥344B / $47.5B launched December 31 2024; the largest state-backed semi vehicle in history — structurally walled-off from US chip startups per CFIUS exposure)

What does the 2026 chip-fundraising calendar look like over the next 12 months?

The Cerebras IPO is the starting gun, not the finish line. Based on the cap-table mechanics, late-stage round timing, and S-1 patterns:

- Q3 2026: At least one of SambaNova, Lightmatter, MatX, or PsiQuantum is likely to file confidentially. Groq is unlikely to IPO independently after the NVIDIA $20B licensing-and-acquihire deal announced December 24 2025 (Fortune analysis January 5 2026 per Fortune) — Groq's $750M Series E September 2025 valuation of $6.9B was effectively re-priced at ~2.9x to $20B via the NVIDIA structure.

- Q4 2026: 2-3 chip startups in the Series D-E range complete bridge rounds at compressed valuations as public-market comparables clarify pricing

- Q1 2027: Honeywell Aerospace HONA spin (Q3 2026 target) starts impacting chip-adjacent defense supplier deal flow; HONA's 2025 net sales of $17.4B and pro forma EBIT of $4.3B create a structural strategic-investor pool for chip-supplier M&A

- 2027 full year: The 18-24 month CSDDD contractual flow-down implementation window arrives 18 months before the statutory 2029 application — see our third-party due diligence guide for the compliance overhead this adds to cross-border chip transactions

The macro tailwinds remain in place: TSMC Arizona $165B 6-fab buildout (Fab 1 N4 production Q4 2024, Fab 2 N3 volume targeted 2028, Fab 3 N2/A16 in 2025-26 construction window) plus Amkor's $7B Peoria advanced packaging campus (October 6 2025 groundbreaking, 750,000 square feet cleanroom, 3,000 jobs, first facility complete mid-2027, production early 2028) plus Stargate Project's $500B 4-year commitment all create sustained demand for chip-startup capital deployment through at least 2028.

What do chip investors actually look for in your data room?

Chip-startup data rooms require deeper technical diligence packs than software startups because investors are pricing capital intensity, fab access, and customer-concentration risk simultaneously. The standard chip-startup data room sections:

- Silicon roadmap with tape-out timelines — node selection (TSMC N3, N2/A16, Samsung 4nm, Intel 18A), fab partner LOIs, mask costs, NRE budget

- Customer concentration disclosure — every contract value over $5M with renewal terms, the Cerebras G42-plus-MBZUAI 86 percent concentration is the canonical comparison investors will model against

- IP filings and patent docket — FTO opinions, claim charts, defensive-publication strategy, any pending litigation

- Inference cost projections — token-per-watt-per-dollar economics versus NVIDIA H100/B100/B200/GB300 benchmarks

- Export-control compliance — Entity List screening, EAR99 versus ECCN classifications, CFIUS exposure on foreign capital, ITAR if defense-relevant

- Talent pipeline — ex-Intel, ex-Nvidia, ex-AMD, ex-TSMC, ex-Synopsys/Cadence hires; Intel's restructuring under Lip-Bu Tan has released significant chip engineering talent

- Capex plan tied to round sizing — 18-24 month burn against next round trigger, fab capacity reservation costs

For sub-vertical-specific diligence packs, see our analogous capital-intensive structures in the biotech data room guide, oil and gas data room guide, and cybersecurity due diligence guide. For founders preparing for the IPO comfort-letter cycle that Cerebras just navigated, our due diligence for IPO guide walks through the 135-day window mechanics under AICPA AS 6101.

Which data room is best for chip-startup fundraising? The honest landscape

Chip-startup fundraises at Series A through C with multi-party syndicates (typically 15 to 30 investors including 5-8 corporate strategics, 3-5 financial VCs, and 2-3 sovereign or family-office anchors) need three things from a data room: per-investor NDA gating because IP and customer disclosures are sensitive, page-level analytics so the founder can verify which partners actually engaged versus skimming, and dynamic watermarking because chip IP leaked to a competitor is existential.

The honest competitive picture:

- Datasite is the enterprise gold standard with per-page pricing $0.40 to $0.85 (a typical chip Series D with 8,000-12,000 pages of historical financials, contracts, IP filings, and customer NDAs can hit $3,200-$10,200 in upload overage alone before subscription costs). Strongest for cross-border or $200M-plus rounds with international participation and bulge-bracket bookrunner involvement.

- Intralinks (SS&C-owned) carries deep IRM controls useful for ITAR-classified defense chip startups. Priced $7,500 starting and $4,000-$25,000-plus annual contracts.

- Firmex is flat-rate at $625-plus monthly with unlimited users — predictable cost for a 12-month Series B fundraise that may have 50+ external party interactions.

- Ansarada offers mid-market AI-driven Q&A management at $244-$5,134 per month tiered, useful for managing 50-plus syndicate questions from corporate strategics, financial VCs, and sovereign anchors simultaneously.

- iDeals serves mid-market with strong UI for non-technical investor reads.

- Peony at $52 per admin per month on the Data Room plan with unlimited rooms, page-level analytics, NDA gates, and dynamic watermarks is best-fit for chip startups raising Series A-C where per-deal data room cost matters and where the founder needs fast setup (under 5 minutes) without enterprise procurement cycles. We make Peony, so this is honest disclosure: for $200M-plus cross-border chip rounds with multiple bulge-bracket banks and ITAR-classified defense documentation, Datasite or Intralinks remain the better fit for the main room. For Series A through C chip fundraises which cover the majority of the 2026 chip-investor deal flow, the flat-rate options (Peony, Firmex, Ansarada) typically deliver equivalent functionality at substantially lower transaction cost.

The decision test: can your founder demo dynamic watermark and page-level analytics views inside a buyer-party sub-room without the buyer seeing the admin view? Peony and Firmex handle this within the standard plan; most enterprise VDRs require a separate admin seat.

For chip founders running parallel investor processes — particularly when targeting NVIDIA NVentures plus Intel Capital plus Samsung Catalyst in the same syndicate where strategic conflicts must be managed — see our guides on different passwords per investor, how to send pitch deck to investors, and the investor data room playbook.

Final reflection

The Cerebras IPO is the starting gun for a 2026 chip-startup fundraising cycle that will define the next 18-24 months. The capital is there — $255.5B Q1 2026 AI venture funding (eclipsing full-year 2025 in one quarter), the NVIDIA Capital Vortex committing $45.3B 2026 YTD, approximately $725B Big Tech AI capex planned for 2026 across Google + Microsoft + Meta + Amazon (up from approximately $410B in 2025 per Yahoo Finance) — and the 12 firms above are the live syndicate spine.

For chip founders, the practical pattern: target one specialist financial VC (Eclipse, Foundation, Walden Catalyst, or Celesta) plus two corporate strategics (any two of NVIDIA NVentures, Intel Capital, Samsung Catalyst, Qualcomm Ventures) plus one sovereign or family-office anchor (G42, Saudi PIF, Mirae Asset, Korea Development Bank). Reserve growth-stage participation for Tiger Global, Coatue, Andreessen Horowitz, or Benchmark depending on stage-fit and brand needs. Set up your secure data room before the first partner meeting because the 2026 inference-cycle thesis requires deeper diligence than the 2023 generative-AI moment did.

The Cerebras two-billionaire moment is real, the cycle is real, and the syndicates are forming now. The question for founders is who calls who first.

Last updated: May 2026

You might also like

Apr 27, 2026

Top 12 Quantum Investors in 2026: $4.9B VC Year After 192% YoY Surge

Jun 26, 2026

Venture Debt Data Room: Why Lenders Underwrite the Floor, Not the Ceiling (2026)

Jun 25, 2026

Series A Data Room: The Step-Change Round Where Your Room Gets Graded (2026)