15 Venture-Backed Consumer Tech Companies Defining 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

If you're a consumer tech founder raising in 2026, this is the list I wish I'd had on the investor side. Not a hype roundup, not "15 DTC brands to watch" — the 15 venture-backed consumer tech companies actually commanding the capital right now, with 2025-2026 funding data I can point to, what investors underwrote, and what that tells you about the bar for your own round.

I'm Sean — six years as a VC at Backed and Target Global before co-founding Peony, the data room purpose-built for fundraising startups. I've sat in the partner meetings where consumer companies got priced (and where they got passed on). The pattern match in 2026 is stark: AI-first consumer is getting roughly half of all venture capital deployed globally, while traditional DTC is still recovering from the 97% funding collapse from 2021's peak. Consumer health is disciplined but alive. Consumer gaming is consolidating. The founders who close are the ones who can articulate, with data, where they sit in that landscape. Here's the current map.

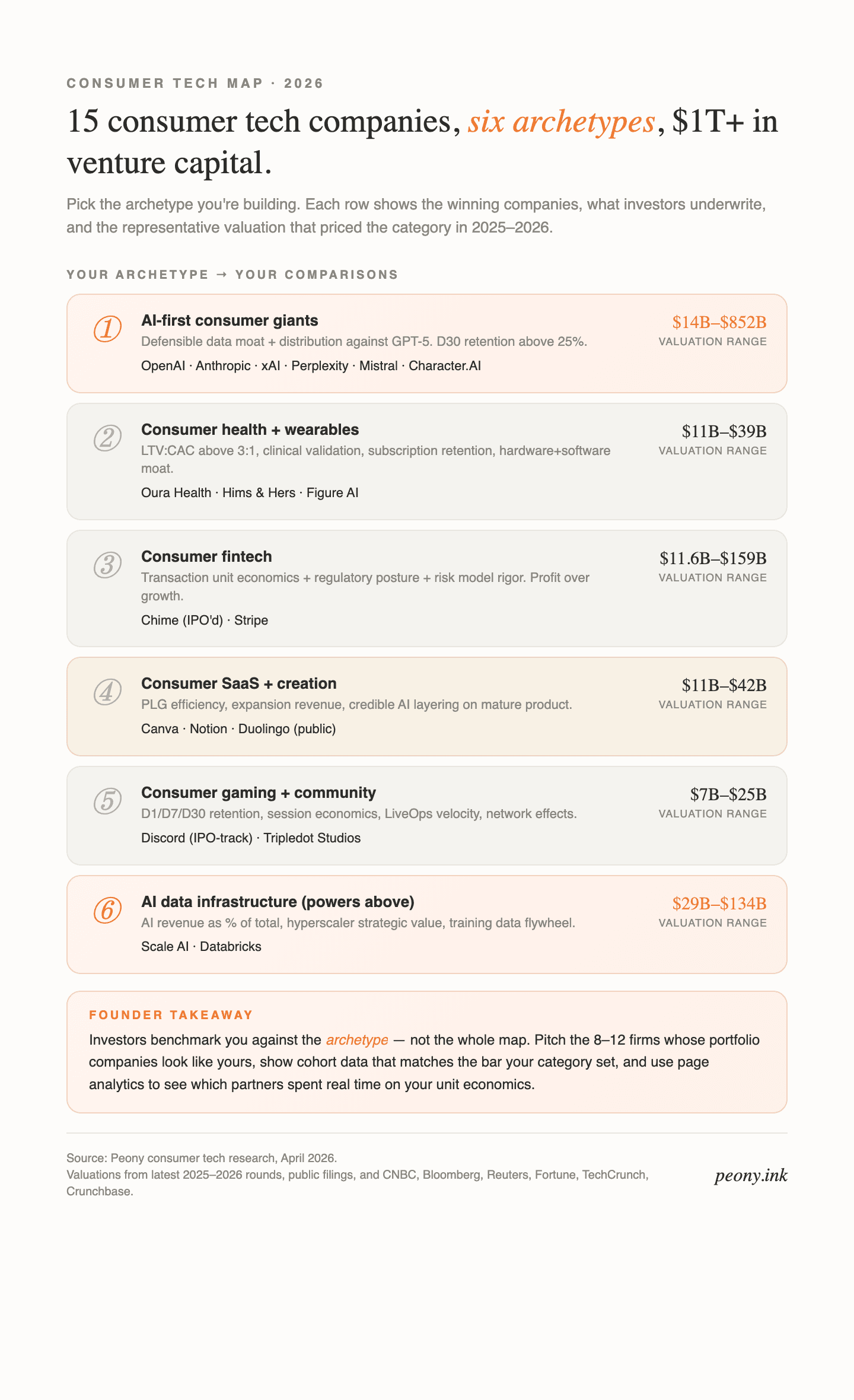

Six archetypes, one shortlist. Pick the archetype you're building — the companies that priced the category in 2025-2026, what investors underwrote, and the valuation range that tells you where the bar actually sits.

TL;DR: consumer tech capital in 2026

- $425B deployed in global venture funding in 2025, up 30% YoY and the third-largest year on record (Crunchbase)

- ~50% of venture went to AI in 2025 — $202B, up from 34% in 2024 (Crunchbase AI trends)

- OpenAI at $852B, Anthropic at $380B (with $800B+ offers surfacing in April 2026), xAI combined with SpaceX at $1.25T total — the AI consumer giants absorb mega-rounds

- 23 US IPOs above $1B in 2025 vs 9 in 2024, including consumer names Chime ($11.6B IPO) and Figma ($18.8B)

- Consumer health remains disciplined — Oura Health at $11B, Hims & Hers at $2.35B revenue, both built on unit economics not hype

Which consumer tech archetype are you building? (decision framework)

Not every consumer tech founder needs to pitch every investor or benchmark against every company on this list. Use the decision paths below to figure out where you actually sit — and which of the 15 companies to study as a pattern, not a comparison:

If you're a solo founder or 3-person team with a consumer AI product at 50K-500K MAU raising $2-5M seed — your comparisons are OpenAI, Anthropic, Perplexity, Character.AI, Mistral, and xAI. Investors benchmark you against D30 retention above 25%, a defensible data moat, and a clear story for what happens when the next foundation model ships. Target a16z Apps Fund, Lightspeed, Index, Thrive, and Spark Capital.

If you're a 5-10 person consumer health team with a clinically-validated product at $1-5M ARR raising Series A or B — your comparisons are Oura Health, Hims & Hers, and a handful of clinical-validation-forward startups. Investors benchmark unit economics (LTV:CAC above 3:1), subscription retention, and regulatory posture. Target Forerunner Ventures, General Catalyst, Thrive Capital, ARCH Venture Partners, and Bessemer's health practice.

If you're a consumer robotics founder with a hardware prototype and enterprise pilots raising $20M+ — your comparison is Figure AI's $39B valuation at Series C on humanoid robotics. Investors underwrite manufacturing capacity, unit margin at scale, and a credible enterprise-to-consumer path. Target OpenAI Startup Fund, Nvidia, Intel Capital, Qualcomm Ventures, Bezos Expeditions, and Microsoft's M12.

If you're a consumer fintech founder with a banking, payments, or lending product and 50K-500K users raising seed through Series B — your public comparisons are Chime (IPO'd at $11.6B) and Stripe (tender at $159B). Investors want regulatory posture, unit economics per transaction, and risk model rigor. Target Sequoia, Ribbit Capital, General Catalyst, Index Ventures, and QED Investors.

If you're a consumer SaaS founder with PLG traction ($500K-$10M ARR, freemium funnel) raising Series A or B — your comparisons are Canva ($42B), Notion ($11B tender), and Figma (IPO'd at $18.8B). Investors underwrite PLG efficiency, expansion revenue, and viral coefficients. Target Index Ventures, Thrive Capital, Accel, Sequoia, and a16z's growth practice.

If you're a consumer gaming, community, or entertainment founder with strong retention metrics (D1 above 45%, D7 above 20%) raising $3-15M — your comparisons are Tripledot Studios ($2B annual gross revenue after AppLovin deal), Discord ($879M revenue, IPO-track), and Duolingo ($414M net profit public). Investors want retention depth, session economics, and a LiveOps or community engine. Target a16z Games Fund, Bitkraft, Makers Fund, Griffin Gaming Partners, and Lightspeed.

You share your deck with the 8-12 firms that match your archetype through personalized links in a Peony data room, watch the page analytics to see who's actually reading your cohort data versus skimming the team slide, and use that signal to prioritize partner-meeting requests. For an investor-directory companion, Top 15 Consumer Investors in 2026 covers the firms still writing checks after the DTC correction; startup fundraising strategy covers the sequencing; and best data rooms for startups covers the tooling layer.

The 15 venture-backed consumer tech companies defining 2026

Ordered by current valuation and strategic weight. All have documented 2024-2026 funding activity or public-market milestones.

1) OpenAI — $852B valuation (March 2026)

- Category: AI-first consumer + enterprise (ChatGPT, Sora, API platform)

- Recent signal: Closed a $122B funding round at $852B post-money in March 2026 — the largest private round in history, led by Amazon ($50B), Nvidia ($30B), and SoftBank ($30B), with $3B from retail investors (CNBC)

- Why it matters: ChatGPT has crossed 1B weekly active users; the round was structured to fund compute buildout ahead of expected IPO. What investors underwrote: consumer scale, developer ecosystem, and a multi-modal product roadmap that makes the foundation-model moat credible.

2) Anthropic — $380B valuation (February 2026), $800B+ offers in April

- Category: AI consumer + enterprise (Claude)

- Recent signal: Closed $30B Series G at $380B in February 2026, led by Coatue and GIC; by April 2026, Bloomberg reported new investor offers valuing the company at $800B+ (CNBC)

- Why it matters: Differentiated on safety, interpretability, and a stronger enterprise revenue mix. Investors underwrote dual-sided growth (consumer Claude app plus API) and the strategic value of a hedge against OpenAI.

3) xAI (now part of SpaceX) — $1.25T combined valuation

- Category: AI consumer (Grok, integrated into X)

- Recent signal: Raised $20B Series E at $230B in January 2026 (Nvidia, Cisco, Fidelity led); in February 2026, SpaceX acquired xAI in an all-stock deal valuing the combined entity at $1.25T ($1T SpaceX, $250B xAI) (Fortune)

- Why it matters: Proves the distribution thesis — xAI used X's 500M+ users as a consumer moat. The SpaceX combination is unique, but the signal for consumer AI founders is clear: if you have an existing distribution surface, foundation-model investors will underwrite the wrapper as a real business.

4) Figure AI — $39B valuation (September 2025)

- Category: Consumer robotics (humanoid general-purpose robots)

- Recent signal: Raised $1B+ Series C at $39B post-money led by Brookfield, with Intel Capital, Nvidia, Qualcomm, Microsoft, OpenAI Startup Fund, and Bezos Expeditions. Total funding ~$1.9B (Intel Capital)

- Why it matters: Launched Figure 03 (October 2025) and Helix 02 (January 2026). BotQ factory targets 12,000 humanoids/year. Investors priced the consumer-robotics thesis ahead of revenue, which means the bar is manufacturing capacity and a credible enterprise-to-consumer path, not early-stage software unit economics.

5) Stripe — $159B valuation (February 2026)

- Category: Consumer commerce infrastructure (payments, subscriptions, tax)

- Recent signal: Tender offer in February 2026 valued the company at $159B, up 74% from $91.5B a year earlier. 2025 payment volume: $1.9T (+34% YoY) (CNBC)

- Why it matters: Powers the majority of consumer tech commerce. Patrick Collison said publicly that IPO is not in the top 5-20 priorities — which tells you how deep private capital runs right now. The business benchmark for consumer infra: profitability at scale with 30%+ revenue growth.

6) Databricks — $134B valuation (February 2026)

- Category: Data infrastructure for consumer AI applications

- Recent signal: Closed $5B round at $134B valuation in February 2026; annualized revenue $5.4B+ (+65% YoY), AI revenue over $1.4B (~26% of total). Raised $1.8B in debt in January 2026 ahead of expected IPO (CNBC)

- Why it matters: S-1 filing expected Q3 2026. Databricks is infrastructure, but it powers a huge share of personalization, recommendation, and analytics in consumer apps — from retail to streaming to gaming. The consumer-tech signal: AI revenue growing as a percentage of total is the metric investors reward.

7) Canva — $42B valuation (August 2025)

- Category: Consumer creative SaaS (design, video, AI creation)

- Recent signal: Employee share sale in August 2025 at $42B (up from $32B in October 2024). ARR $3.3B, 27M paid users, 240M MAUs in 190 countries. Fidelity led (Fortune)

- Why it matters: Blackbird (Canva's largest VC investor) signaled a possible second-half 2026 IPO. The business pattern: PLG freemium plus AI creation tools plus enterprise expansion. Investors underwrote the 240M MAU-to-27M-paid conversion funnel as the decade's best consumer PLG motion.

8) Scale AI — $29B valuation (June 2025)

- Category: Consumer AI data infrastructure

- Recent signal: Meta invested $14.3B for 49% non-voting stake at $29B valuation in June 2025 — the largest VC round of 2025. CEO Alexandr Wang left for Meta, Jason Droege replaced him. Launched Scale Labs research division in March 2026 (Crunchbase)

- Why it matters: Scale AI powers training data for consumer-facing AI across chat, image, and voice. The Meta deal was structurally close to an acquisition (DOJ-adjacent scrutiny). Pattern for founders: if you sit in the training-data or evaluation layer for consumer AI, you're strategic to every hyperscaler.

9) Perplexity AI — $20B valuation (September 2025)

- Category: AI-powered consumer search

- Recent signal: Raised $200M at $20B valuation in September 2025. ARR grew from $80M (late 2024) to ~$200M (February 2026). Signed a three-year $750M Microsoft Azure commitment in January 2026 for Deep Research and Model Council features (TechCrunch)

- Why it matters: Perplexity proved the answer-first, citation-driven interface can compete with Google on information-retrieval consumer use cases. Pattern: proprietary distribution (browser integrations, partnerships) plus defensible product UX is priced aggressively even against foundation-model incumbents.

10) Mistral AI — $14B valuation (September 2025), $830M follow-on in March 2026

- Category: AI consumer + enterprise (Le Chat, open-weight models)

- Recent signal: Raised €2B ($14B valuation) in September 2025, led by ASML ($1.5B for 11% stake). Raised an additional $830M in March 2026 for Paris and Sweden data centers. Le Chat mobile launched February 2025 — 1M downloads in two weeks. Revenue guidance: €1B by end of 2026 (20x growth) (Bloomberg)

- Why it matters: Europe's flagship AI lab. Strategic positioning as the sovereign-AI option for European consumers and enterprises. Open-weight distribution strategy combined with consumer Le Chat app and enterprise API.

11) Oura Health — $11B valuation (October 2025)

- Category: Consumer health wearable (smart ring)

- Recent signal: Raised $900M Series E at $11B valuation in October 2025, led by Fidelity with ICONIQ, Whale Rock, and Atreides. On track for $1B+ 2025 revenue (2x vs 2024's $500M). Interviewing IPO bankers for potential 2026 listing (CNBC)

- Why it matters: Gold standard for consumer health hardware-plus-software. Pattern: premium hardware price ($300+), subscription software tier, and clinical-grade data build a defensible hardware-plus-recurring-revenue moat. Investors underwrote the clinical validation and corporate-wellness channel expansion.

12) Hims & Hers Health (NYSE: HIMS) — $2.35B 2025 revenue

- Category: Consumer digital health (telehealth, prescriptions, GLP-1)

- Recent signal: 2025 revenue $2.35B (+59% YoY). 2026 guidance $2.7B-$2.9B (15-24% growth). Stock fell ~51% over six months into early 2026 on regulatory concerns, then rebounded ~35% in mid-April on GLP-1 momentum. International revenue +400% after ZAVA and Livewell acquisitions (Hims IR)

- Why it matters: The public-market case study for consumer digital health at scale. Pattern: direct-to-consumer + telehealth + subscription + international expansion. What broke (and rebounded): stock-price volatility on GLP-1 regulatory questions shows why regulatory posture is a first-order underwriting item in consumer health.

13) Chime (Nasdaq: CHYM) — IPO'd at $11.6B in June 2025

- Category: Consumer fintech (digital-first banking)

- Recent signal: IPO'd on Nasdaq at $27/share on June 12, 2025, closing +37% at $37.11 on debut. IPO valuation $11.6B; debut market cap ~$13.5B. Raised ~$700M in the offering (CNBC)

- Why it matters: First major consumer fintech IPO of the 2025 cycle — and priced below the 2021 peak of $25B, showing public markets demand profitability not growth-at-all-costs. Pattern: fee-free model + interchange revenue + credit-building wedge serving an underbanked segment scaled to 20M+ customers.

14) Duolingo (Nasdaq: DUOL) — $414M net profit 2025

- Category: Consumer edtech (language learning, expanding to math and chess)

- Recent signal: 2025 revenue grew 39%; bookings surpassed $1B; net profit tripled to $414M; paid subscribers hit 12.2M (+28% YoY). Stock down ~80% from 2025 highs after disappointing 2026 guidance. CEO pivoting to DAU growth (100M DAU by 2028 target) (Duolingo IR)

- Why it matters: Profitable consumer subscription SaaS at scale. The stock correction is a market signal: public-markets now penalize deceleration even in profitable consumer businesses. Pattern for founders: gamification, daily-habit loops, and AI tutor layering (Max → Super tier) compound retention.

15) Discord — confidentially filed IPO, January 2026

- Category: Consumer community (communication for gamers, creators, communities)

- Recent signal: Confidentially filed for IPO January 6-7, 2026 targeting Q1/March 2026 debut with Goldman Sachs and JPMorgan. 2025 revenue $879M. Valuation estimates: secondary markets imply $6.8-8B; bull case $25B at 20-25x ARR (Fintool)

- Why it matters: Discord rejected Microsoft's $12B offer in 2021 at $15B valuation. The IPO range ($7-25B) shows how far consumer community valuations compressed. Pattern: community + recurring Nitro subscription + creator monetization + expansion into games publishing and AI features.

Runners-up worth tracking: Character.AI (unique $2.7B Google licensing deal in August 2024 that left Character independent but abandoned LLM development, with DOJ antitrust scrutiny), Tripledot Studios (consumer gaming consolidator post-$800M AppLovin deal, 25M+ DAUs, $2B gross annual revenue), Notion ($11B tender in December 2025, ARR approaching $1B), and ElevenLabs (consumer AI voice — category leader but round sizes not fully disclosed).

What the 15 share: three funding playbooks that actually worked 2024-2026

Playbook 1: "Own unique distribution or unique data"

OpenAI, Anthropic, and Perplexity raised at eye-watering multiples because each has a distribution wedge the next GPT release can't replicate: ChatGPT's installed consumer base, Claude's enterprise integrations, Perplexity's search index and browser partnerships. xAI rode X's 500M+ users.

What this means if you're a consumer AI founder raising seed or Series A: investors in 2026 de-rate foundation-model wrappers. Your round gets priced on what you own — proprietary data, distribution surface, workflow integration, or community — not just the model you're calling. If you're a two-person team with a GPT wrapper and no moat, expect a strategic-partner round at modest terms. If you own something foundation models can't cheaply reproduce — a user corpus, a B2B2C distribution partnership, a workflow integration — you price aggressively.

Playbook 2: "Profitability rhymes with premium valuation"

Chime priced its IPO below the 2021 peak because public markets now penalize unprofitable growth. Duolingo's stock corrected 80% on decelerating bookings growth despite tripling net profit. Hims & Hers rebounded when GLP-1 revenue looked durable. Oura Health was priced at $11B partly because of clear paths to profitability via hardware margin plus subscription.

What this means if you're a consumer health, fintech, or SaaS founder prepping Series A or B: LTV:CAC above 3:1 and CAC payback under 18 months are table stakes. Gross margins matter — separate your hardware margin from software/subscription so a Forerunner or General Catalyst partner can model steady-state profitability in 10 minutes. Companies demonstrating "rule of 40" (revenue growth + operating margin) clear the bar. If you can't defend unit economics under a partner's questioning in the first 15 minutes, you're not ready yet.

Playbook 3: "AI layering wins in mature categories"

Canva's $42B valuation came after layering AI creation tools into its existing design platform. Duolingo's profit tripled partly because of AI-driven personalization in its paid tier. Oura's interpretation layer deepens as its data corpus grows. Even Hims & Hers built AI-powered care-plan personalization into its telehealth motion.

What this means if you're a consumer SaaS or DTC founder with a mature product and existing users: you don't need to be AI-first to get priced like an AI company. If you have existing consumer scale, credible AI layering that demonstrably deepens the moat — measurable retention lift, margin expansion, or net-new SKUs — is enough to re-rate the business. Bring before/after cohort curves that isolate the AI contribution, not a generic "we added AI" slide.

What investors underwrite in consumer tech — the 2026 checklist

-

Unit economics that breathe. LTV:CAC above 3:1, CAC payback under 18 months, gross margin above 60% for digital products (hardware is lower but should show margin expansion path). Consumer fintech wants transaction-level unit economics. Consumer health wants per-patient lifetime value.

-

Retention that doesn't crater. D1, D7, D30 retention are the first charts on the first slide for consumer apps. Consumer AI benchmark in 2025-2026: D30 above 25% is strong, above 40% is exceptional and priced aggressively. Subscription retention (annual cohort curves) is the proxy at scale.

-

A defensible moat against the next foundation model. If you're AI-first, investors ask "what happens when GPT-5 ships?" Your answer should be proprietary data, workflow integration, distribution surface, or community — not "our model is better."

-

Distribution that's legible. Retail LOIs, agency partnerships, publisher alliances, insurance contracts, or organic community. Paid-only acquisition at high CAC is a red flag. a16z's State of Consumer AI 2025 explicitly called out distribution as the variable most correlated with outlier outcomes.

-

A team that ships. Founder-market fit (deep understanding of the consumer problem), consumer operators on the team (brand, growth, product), and technical depth appropriate to the category. Ex-Stripe, ex-Shopify, ex-Meta, ex-top-consumer-AI engineers command a premium.

-

Regulatory and privacy posture. Consumer health needs HIPAA; consumer fintech needs licensing and risk model rigor; consumer AI increasingly needs privacy architecture as state laws (CPRA, Colorado, Connecticut, Virginia) mature.

The data room is a second pitch

Every partner meeting ends the same way: "share the deck and financials." Eight firms get your link. If you share a Google Drive folder, you get the same zero-signal from each — just email reply timing to guess who's serious.

If you share a professional data room, you get a dashboard: which partner opened your financial model, how long they spent on your unit economics slide, who forwarded the link internally, who returned three times to your cohort page. That's the difference between a tight 8-10 week raise and a three-month slog.

This is the pitch for Peony specifically. Consumer tech founders are exactly our sweet spot because four things matter more here than in most categories:

- Page-level analytics on dense retention charts, cohort tables, and unit economics — not "did they open the link" but "how long on which page"

- NDA gates and dynamic watermarks on sensitive user data, channel CAC breakdowns, and risk models that would be competitively damaging if forwarded to a portfolio company in an adjacent space

- AI auto-indexing that turns a messy Google Drive folder into a clean, investor-ready structure in under 3 minutes

- Personalized links per investor so you can revoke access if a firm passes, and see individual engagement patterns instead of aggregate room stats

Business is $30/admin/month and the Data Room tier is $52/admin/month — considerably less than one hour of your lawyer's time, and a small fraction of what Datasite charges for an M&A-grade VDR.

The broader platform covers everything a consumer tech raise needs: startup data rooms, e-signature workflows with AI field detection, custom branding so your room looks like your consumer brand not a generic VDR, Smart Q&A for handling diligence questions at scale, AI Extraction for pulling numbers out of unstructured docs, AI Rooms that let investors ask your data room natural-language questions with citations, screenshot protection that blocks and logs capture attempts, and AI-powered redaction for auto-masking sensitive client names or numbers. Most consumer tech founders need four or five of these. They ship across the Business and Data Room plans.

Not a competitor pitch. The honest shape of the tool I wish I'd had when I was on the investor side watching founders share pitch decks through raw Dropbox links.

Related Resources

- Top 15 Consumer Investors in 2026 — the investor-directory companion to this company map

- Top Health Tech Investors — if you're in the Oura/Hims lane

- Top B2B SaaS Investors — if your consumer tech sells as horizontal SaaS

- Top Fintech Investors — if you're in the Chime/Stripe lane

- Top Media Investors — if you're in the Discord/Duolingo lane

- Investor Outreach Plan: 8 Steps

- Startup Fundraising Strategy Complete Guide

- AI Pitch Deck Guide

- How to Track Pitch Deck Engagement

- Best Data Rooms for Startups

- Virtual Data Room Setup for Consumer Tech Fundraising

- Due Diligence Data Room Checklist

- What Is a Virtual Data Room

- Virtual Data Room Guide for Fundraising

- Pricing

FAQ

I'm a seed-stage consumer AI founder raising $4M — which VCs actually write checks into consumer AI in 2026 given what OpenAI and Anthropic have done to the category?

For a $4M consumer AI seed, the highest-conviction specialists are a16z's Apps Fund (writes $1-5M seed checks, backed Character.AI and funded much of the consumer AI wave), Lightspeed Venture Partners ($2-8M consumer AI seed program), and Index Ventures ($3-10M seed for consumer AI with strong engagement metrics). Spark Capital, Thrive Capital, and General Catalyst are active at seed-through-A with $5-15M. The bar has moved: with OpenAI at an $852B valuation and Anthropic raising at $380B (with offers surfacing at $800B+ per Bloomberg in April 2026), investors now underwrite whether you have a defensible data flywheel, proprietary distribution, or a workflow advantage that can't be replicated by a foundation-model wrapper. Show specific retention lift from AI versus non-AI baselines, proprietary signal your competitors can't access, and a clear story on why you're not road-kill when GPT-5 or Claude 5 ships. Share these through a Peony Business data room at $30/admin/month for page-level analytics that show which partner actually reviewed your retention cohorts versus who skimmed the team slide — Google Drive gives you zero investor-level visibility on dense quantitative material.

What are realistic 2026 check sizes and valuations across seed, Series A, and Series B in consumer tech after the 97% DTC correction and the AI reset?

Consumer tech check sizes bifurcated hard in 2025-2026. AI-first consumer rounds run hot: $2-8M seed at $15-40M valuations, $10-25M Series A at $75-250M valuations, and $40-100M Series B at $400M-$1.5B valuations — with outliers like Perplexity raising $200M at $20B. Traditional DTC and consumer health remain disciplined after the 2022-2023 correction: $1-5M seed at $8-20M valuations, $5-15M Series A at $30-80M, and $20-50M Series B at $150-400M. Mega-rounds ($100M+) are concentrated in AI (OpenAI's $122B round, Anthropic's $30B, xAI's $20B, Scale AI's $14.3B Meta check) and in category leaders with proven unit economics like Oura Health's $900M at $11B. Total global VC hit $425B in 2025 (up 30% YoY), with 50% going to AI per Crunchbase data. For pricing discipline at lower stages, investors want LTV:CAC above 3:1 and CAC payback under 18 months. Prepare your cohort tables and unit economics in a Peony Data Room at $52/admin/month — AI auto-indexing organizes everything in under 3 minutes and page analytics show whether investors actually read your unit economics or skipped to the team page.

I'm building a consumer AI product with 100K MAU raising $3M seed — what specifically do investors like a16z and Lightspeed want to see in 2026 beyond DAU/MAU?

For a $3M consumer AI seed, a16z's Apps Fund and Lightspeed's consumer AI practice look well beyond MAU. Both firms have publicly framed consumer AI underwriting around three pillars: engagement depth (sessions per day, session length trending up with AI assist versus baseline), retention against the brutal 2024-2025 consumer AI benchmark (D30 retention above 25% is strong; D30 above 40% is rare and gets priced aggressively), and moat structure (proprietary data, workflow integration, or network effects that survive GPT-5). They explicitly de-rate GPT wrappers and reward products that own unique signal — like Character.AI's conversation corpus before the Google deal, or Perplexity's search index. You also need to show retention curves are not cratering after the first 7 days, because a16z's 2025 State of Consumer AI report flagged that most novelty apps die at D7. Lead with D1, D7, D30 retention charts; AI-driven engagement lift; your proprietary data moat; and a specific plan for what happens when the next foundation model ships. Gate these through NDA-protected links in a Peony Business data room at $30/admin/month, and add dynamic watermarks on the Data Room plan at $52/admin/month so if a partner forwards your retention curves internally, you see it — Dropbox has no NDA gate or watermarking for this level of competitive sensitivity.

We're a consumer health tech startup with $3M ARR preparing for Series B in 2026 — what data room structure do investors expect after Oura reached $11B?

Consumer health Series B data rooms in 2026 need nine sections, learned from the underwriting patterns that priced Oura at $11B and Hims & Hers into its $2.35B revenue run-rate. One: cohort retention curves by acquisition channel with 12-18 month tails. Two: unit economics with LTV:CAC above 3:1, CAC payback under 18 months, and gross margin analysis separating hardware from software/subscription. Three: subscription retention and expansion revenue (critical — Oura's subscription model was a core part of the $11B underwriting). Four: clinical validation where applicable — published studies, FDA status, or academic partnerships. Five: HIPAA and data privacy posture with SOC 2 Type II if US-based. Six: channel mix with CAC by channel (organic, paid social, retail, insurance, corporate wellness). Seven: product roadmap showing how AI deepens the moat (Oura's interpretation layer and Hims' care-plan personalization). Eight: competitive positioning and defensibility. Nine: team bios with operator credentials from consumer brands. Peony Data Room at $52/admin/month uses AI auto-indexing to structure these in under 3 minutes, Smart Q&A routes investor diligence questions through AI-drafted answers with page citations, and page analytics show exactly which Series B partner spent 20 minutes on your cohort curves versus who clicked off at slide 3.

I'm running a parallel pitch process with 20 VCs for a consumer fintech seed — how do I prevent my unit economics and user acquisition playbook from leaking to competitors?

Consumer fintech especially is vulnerable to competitive intel leaks because your CAC by channel, retention by cohort, and risk model architecture are directly actionable by a competitor who gets forwarded the deck. With 20 VCs in parallel — some of whom have portfolio companies in adjacent fintech categories — you need five controls: per-investor personalized links so each firm has their own URL that can be revoked independently; NDA acceptance gated before any sensitive financials load; dynamic watermarks with viewer identity (email, timestamp, IP) on every page so a forwarded document traces back to the specific leaker; screenshot detection that logs and can block capture attempts; and expiry dates aligned with your fundraising window. This matters now more than in 2023 because Chime's IPO at $11.6B in June 2025 validated consumer fintech, and fast-followers are aggressive. Peony Business at $30/admin/month includes personalized links, screenshot protection, and NDA gates, with dynamic watermarking on the Data Room plan at $52/admin/month — Google Drive and Dropbox share through generic links with no per-viewer tracking, no watermarking, and no screenshot protection.

I'm raising pre-seed for a sustainable consumer products brand with $400K revenue — how long should I expect the raise to take in 2026 and what signals accelerate it?

Sustainable consumer brands raising pre-seed in 2026 typically take 8-14 weeks from first meetings to close, compressed significantly from the 2023 norm of 20+ weeks when consumer VCs had retreated from DTC after the 97% DTC funding collapse from the 2021 peak. The timeline is now faster because consumer mega-funds re-opened — L Catterton raised $11B in 2025, VMG Partners closed $1B for Consumer Fund VI, and CAVU closed $325M in February 2026 specifically for early-stage consumer. Forerunner Ventures remains the category anchor for DTC at $3-8M seed checks with Fund VII at $500M. What compresses timeline: demonstrable unit economics (LTV:CAC above 3:1), a real retention story (not just first-purchase volume), authentic sustainability credentials backed by supply-chain documentation, and a distribution wedge (retail LOIs, insurance partnerships, or direct community). What drags it out: corporate venture arms at CPG companies with sustainability assessment committees, impact funds with ESG scoring, or any thesis that requires education on why sustainability pays. Have your data room ready before outreach — Peony Data Room at $52/admin/month builds it in under 5 minutes with AI auto-indexing, and engagement analytics show which VCs are progressing fastest so you time partner meetings with the most engaged firms.

My startup spans consumer gaming and AI personalization — after Tripledot's $800M AppLovin deal, which gaming-plus-AI investors should I target and what metrics do they want?

Gaming-plus-AI is a hot crossover in 2026, accelerated by Tripledot Studios' $800M acquisition of AppLovin's games portfolio in June 2025 (combining into 2,500+ staff, 25M+ DAUs, $2B annual gross revenue). For a $5M seed, target a16z Games Fund ($5-15M for gaming with AI-driven retention mechanics, backed multiple studios), Lightspeed Venture Partners ($3-10M for mobile gaming with AI layers), and Bitkraft Ventures ($2-8M gaming specialist with gaming-AI thesis). BITKRAFT, Makers Fund, and Griffin Gaming Partners are the gaming-specific specialists; a16z and Lightspeed crossover into gaming-plus-AI. What they underwrite: session economics (ARPDAU, ARPPU, monetization per cohort), retention depth (D1 above 45%, D7 above 20%, D30 above 10% for casual; higher for mid-core), AI moat (personalized content generation, dynamic difficulty, or LiveOps automation), and a LiveOps story showing content velocity. If gaming is the primary, lead with D1/D7/D30 retention and ARPDAU; if AI personalization is the primary, lead with retention lift from personalization versus static baseline. Create separate branded data rooms for gaming versus AI-focused investors with Peony Business at $30/admin/month — each audience sees the narrative that matches their thesis.

I'm a consumer tech founder choosing a data room for my Series A fundraise — what actually matters when consumer data and competitive intel are on the line in 2026?

Consumer tech Series A data rooms in 2026 need four capabilities generic tools lack. First: per-investor page-level engagement analytics so you see whether Tiger Global's partner spent 18 minutes on your cohort retention page versus who bounced after the team slide — critical when you're running parallel pitches with 10-20 firms. Second: NDA gates on sensitive sections (user retention playbooks, channel CAC breakdown, risk models) so no investor views them without signed acceptance. Third: dynamic watermarks with viewer identity because your user acquisition playbook and retention strategy are directly actionable competitive assets — Consumer tech is uniquely vulnerable to leakage because retention tactics and channel mix translate 1:1 to a competitor. Fourth: AI-powered document organization to structure pitch deck, financial model, cohort data, and compliance docs into investor-ready folders in minutes — not the days it takes in Google Drive. Google Drive and Dropbox share through open links with zero tracking and zero watermarks. Enterprise VDRs like Datasite charge $15,000+ per deal and are architected for M&A, not startup fundraising. Peony Data Room at $52/admin/month is purpose-built for startup raises — AI auto-indexing, page analytics, personalized links, dynamic watermarks, screenshot protection, and NDA gates — the security consumer tech investors expect at a price that makes sense for a startup.

The short version

Fifteen companies, $1T+ in venture capital, three playbooks that actually priced through the AI reset and DTC correction. AI-first consumer absorbs the mega-rounds. Consumer health stays disciplined. Consumer fintech crossed into public markets. The founders who close in 2026 show unit economics that breathe, a moat against foundation models, and distribution that's legible — then pitch the 8-12 firms that match their archetype with real cohort data, not slide-deck vibes.

If you want the investor-directory companion, Top 15 Consumer Investors in 2026 covers the firms still writing checks after the 97% DTC correction. If you want the tooling layer, our data rooms page has the full feature breakdown, the fundraising solution page covers the founder-to-investor workflow, and the pricing page lays out Business at $30/admin/month and the Data Room tier at $52/admin/month. Set up your data room in under 5 minutes and run the outreach.

You might also like

May 27, 2026

10 Fundraising Data Room Mistakes Sophisticated Bidders See in 2026

Apr 29, 2026

Top 8 Boston Investors in 2026: The Founder's Complete Guide to Raising in Boston & Cambridge

Apr 29, 2026

Top 10 Active Investors in Italy (2026): Complete Founder Guide to Italian VC Firms