10 Greatest Pitch Decks That Actually Got Funded in 2026 (VC Analysis)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

If you're searching for pitch deck examples in 2026, you're probably in that same founder headspace I watched dozens of times from the investor side: you don't want theory, you don't want a template, you want the decks that actually closed rounds and you want someone who sat through hundreds of pitches to tell you exactly what to steal.

I'm Sean — I spent six years as a VC at Backed VC and Target Global before co-founding Peony, the data room purpose-built for fundraising startups. I've sat through more than 500 pitch meetings and watched the same pattern separate the decks that close from the ones that stall. This isn't a "10 famous decks" roundup. These are the 10 pitch decks I'd make every founder study, across four eras of fundraising, with what investors actually underwrote and what you can steal for a 2026 raise.

Ten decks, four eras, one pattern. What separates the decks that closed rounds is not design or slide count — it is the sequence in which they answered the eight questions every investor asks. In 2026 the moat slide does more work than any other.

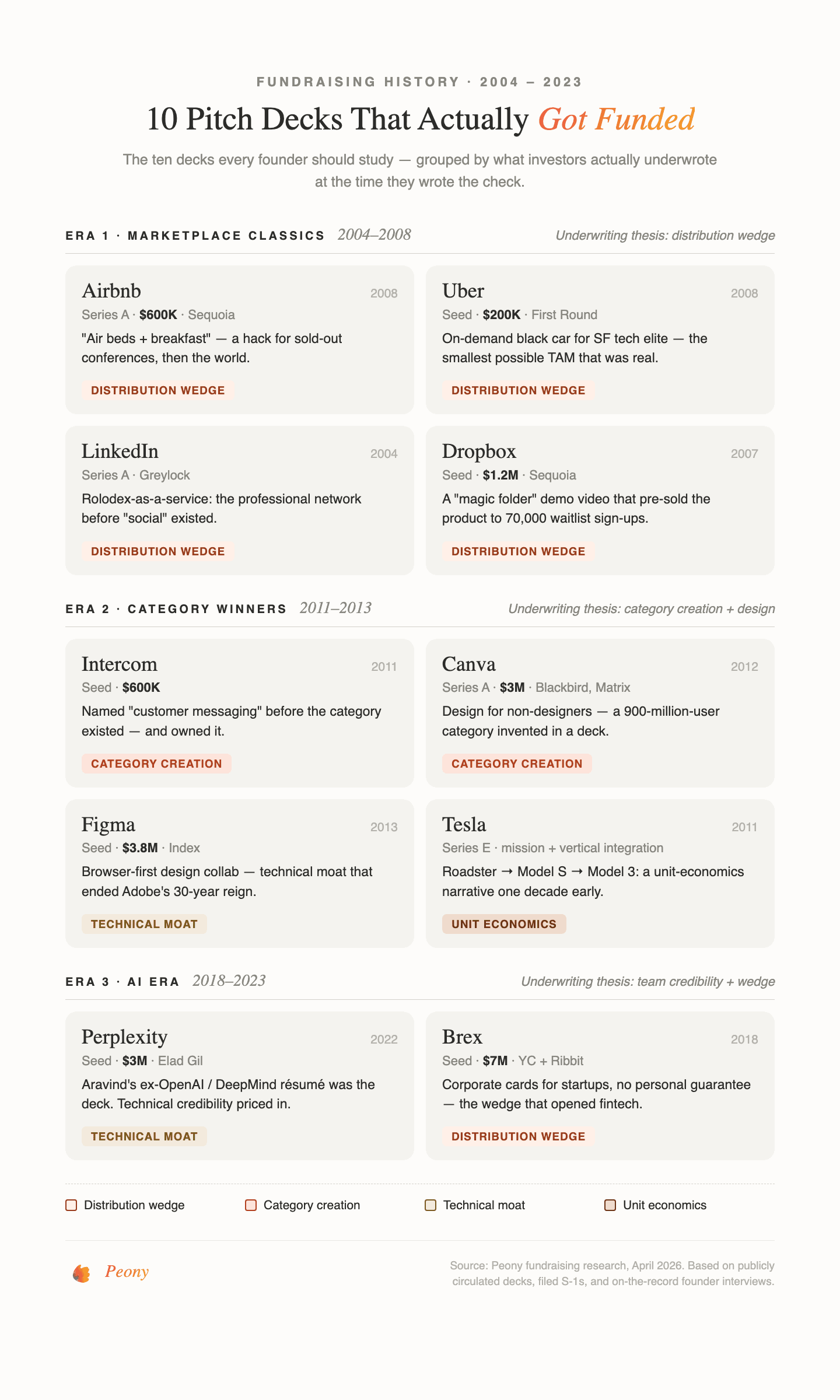

Quick answer — what are the greatest pitch decks of all time? The 10 decks every founder should study span four eras: Airbnb 2008 ($600K seed, 14 slides), Uber 2008 ($1.25M seed, 25 slides), LinkedIn Series B 2004 (Reid Hoffman, category-creation gold standard, 45 slides), Dropbox 2007 ($1.2M Sequoia seed, 17 slides), Intercom 2011 ($600K seed), Canva 2012 ($1.6M after 100+ rejections), Figma 2013 ($3.8M pre-seed, $18.8B IPO 2025), Tesla 2011 ($192M, the hardware reference, 15 slides), Perplexity Series A 2022-2023 ($25M, now $20B), and Brex Series B 2018 ($57M, now $7.4B). Same eight-question structural arc across 18 years — the moat slide does 30% of 2026 underwriting.

Quick comparison — the 10 greatest pitch decks at a glance

| Deck | Year | Slides | Raise | What it teaches |

|---|---|---|---|---|

| Airbnb | 2008 | 14 | $600K seed | The DNC 2008 wedge moment — one provable scenario |

| Uber (UberCab) | 2008 | 25 | $1.25M seed | Tight ICP + structural critique of incumbents |

| LinkedIn Series B | 2004 | 45 | (Reid Hoffman's deck) | Category creation + flywheel-as-system |

| Dropbox | 2007 | 17 | $1.2M seed | Distribution as the main stage, not appendix |

| Intercom | 2011 | seed deck | $600K | Team slide carries the underwriting at seed |

| Canva | 2012 | seed deck | $1.6M + $1.4M grant | Iterating on rejection feedback (100+ rejections) |

| Figma | 2013 | demo-first | $3.8M pre-seed | Live demo beats slide deck, listening to "no" |

| Tesla | 2011 | 15 | $192M | Status-update cadence + platform positioning |

| Perplexity | 2022-2023 | Series A deck | $25M | Citation-interface moat survives GPT-5 |

| Brex | 2018-2019 | Series B deck | $57M | Unit economics density + regulatory posture |

TL;DR — the 2026 pitch deck reality

- 2 minutes 14 seconds: average VC attention on first-pass deck review, per DocSend's 2024-2025 analytics. Decks longer than 15 slides see roughly 40% lower engagement.

- $425B deployed in global venture funding in 2025 (up 30% YoY, third-largest year on record) with ~50% going to AI per Crunchbase.

- Median seed round in 2025-2026: $2.5M-$3.5M at $8M-$20M valuations. Median Series A: $10M-$20M at $45M median pre-money.

- Time from seed to Series A: 616 days (roughly 2.1 years in 2025, up from 1.5 years in 2019) per Carta's 2025 data.

- The moat slide is doing 30% of the underwriting on AI-first consumer and applied AI decks — a16z's Apps Fund and Lightspeed publicly de-rate "proprietary AI" as a meaningless moat claim.

- The first 4 slides get 60% of total deck attention — what I call the 2:14 skim test. If your traction chart is on slide 7, you've already lost it.

Last updated: April 2026

What makes a pitch deck "great" in 2026 (not just famous)?

A great pitch deck does three jobs fast — and in 2026 one of those jobs has changed materially from 2020. Specifically, the moat-slide weighting shift moved from 15% to 30-40% of investor underwriting weight, which is what separates the eight-question structural arc from a glossy 2018-style template:

- Makes the problem feel inevitable — "of course this is broken, why didn't someone fix this already"

- Makes the solution feel obvious — "this is the cleanest path to fix it"

- Makes the bet feel asymmetric and defensible — "if they're right, this gets huge, and here is the specific moat that protects the bet from GPT-5"

The third job used to be 15% of the underwriting work. In 2026 it's 30-40% on anything AI-adjacent and it's the slide VCs reread. When I was at Backed, partners would screen-share a founder's deck and debate one slide — almost always the moat slide. That debate now happens on every AI deck that crosses the desk, and the decks that win are the ones that preempt the debate with a specific answer drawn from the 4-moat taxonomy (data flywheel, workflow integration, distribution surface, network effect) rather than the dead-letter "proprietary AI" claim that a16z's Apps Fund de-rates on sight.

The decks below span 18 years (2008-2026) and each nails this in a different style. That's the point. There isn't one "perfect template." There are patterns that reliably work, different for different archetypes, and the closer your situation maps to one of these decks, the more value you get from studying that specific deck's moves. For the deeper cluster on fundraising strategy, fundraising rounds, and investor outreach, we have companion guides that cover the process around the deck.

How should you structure your pitch deck (decision framework)?

Not every founder should copy the same deck. Match your raise archetype to the eight-question structural arc — every deck below answered the same eight investor questions; what changed was emphasis. Use the decision paths below to figure out which of the 10 decks actually maps to your situation:

If you're a solo or small-team founder raising pre-seed or seed ($500K-$3M) on vision and a prototype — your comparisons are early Airbnb, early Figma, and early Intercom. You are selling your taste, speed, and insight, not your numbers. Emphasize team slide heavily, lean on a sharp founder-market fit story, and keep the deck tight at 10-12 slides. Target US seed investors and operator-angel networks.

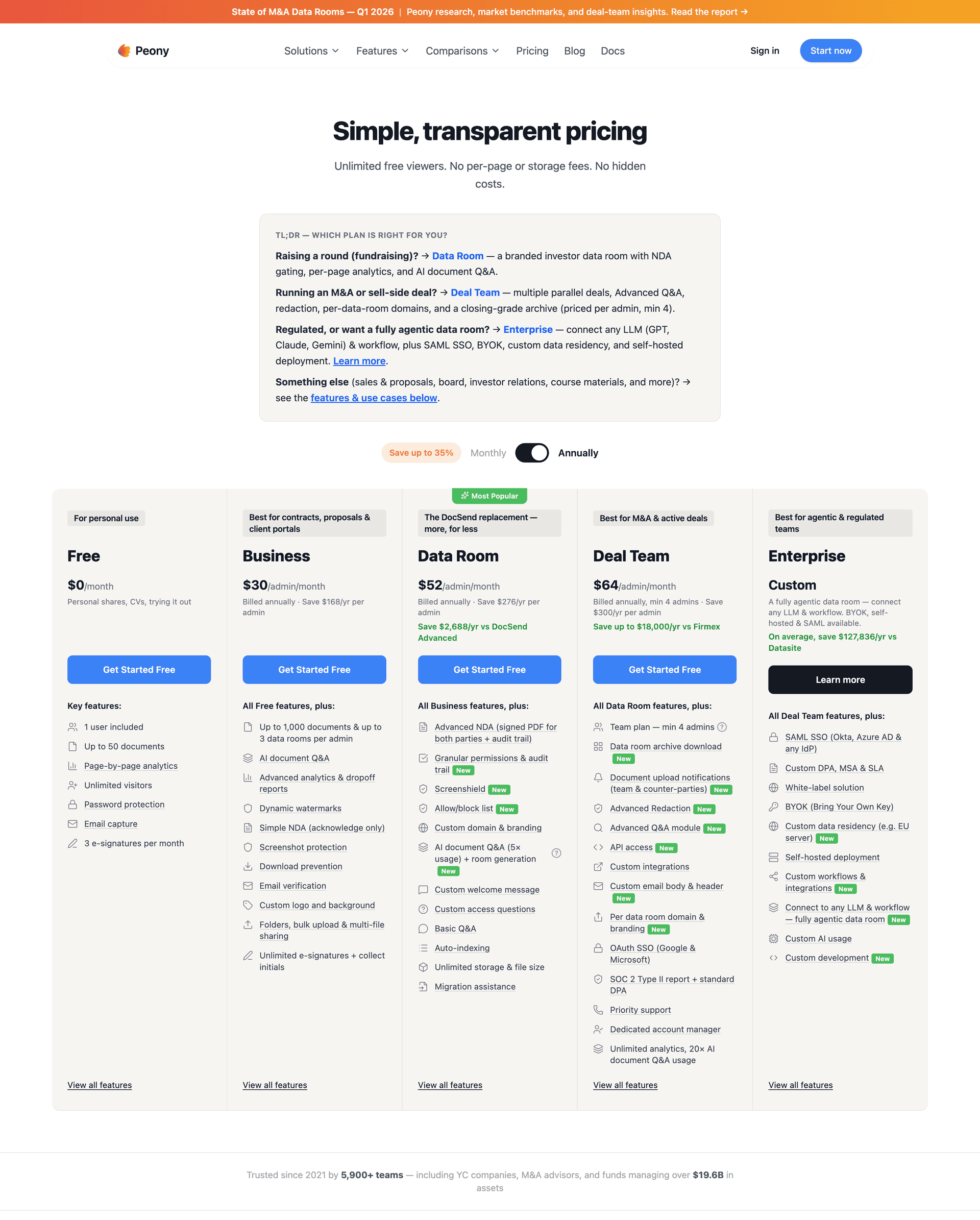

If you're raising $3M-$10M seed for a consumer AI product with some MAU and no revenue — your comparison is Perplexity's $25M Series A (and the pattern Anthropic established). Lead with product demo visuals, then moat (proprietary data, workflow, distribution surface), then traction signals. The moat slide carries the round. Share deck through personalized links with NDA gates in a Peony data room so if you forward the moat thesis to an a16z partner who has a competing portfolio company, you see it.

If you're raising $10M-$30M Series A for a B2B SaaS with $1M-$5M ARR — your comparisons are Carta's $7M Series A (messaging pattern) and Brex's $57M Series B (traction density). Flip the deck order: lead with the traction chart, not the problem. Your ARR, NRR, and logo roster are the wedge. Use page analytics to see which Series A partner actually reached your cohort retention page.

If you're raising $15M-$50M for hardware or capital-intensive tech — your comparison is Tesla's 2011 $192M deck. 15 slides, execution-heavy, status-update cadence. Show manufacturing plan, partnership proofs, and a platform positioning that opens multiple SKUs. Protect technical IP and BOM sheets with screenshot protection and watermarks in a Peony Business data room.

If you're a second-time founder reopening a cold round or pivoting narrative — your comparison is LinkedIn Series B's intellectual-honesty approach. Reset explicitly in the first 3 slides. Name what changed. Don't pretend the silence didn't happen. Use Peony engagement analytics to diagnose whether the new narrative is landing within 48 hours of sending.

If you're creating a new category (not a line item on an existing enterprise budget) — your comparisons are LinkedIn and Canva. Your deck has to do extra work: define the category, define the "aha," map the growth path, and provide a before-and-after customer mental model. Market-size the real addressable opportunity bottom-up.

If you're raising growth capital for a marketplace or network business — your comparisons are Airbnb's expanded decks and Uber's 2008 structure. Sell the flywheel explicitly: what the two sides are, how they reinforce each other, what your take rate is, and why your network effect survives a larger competitor entering. Target marketplace investors and generalist growth funds.

Throughout any of these paths, Peony's page-level analytics in a fundraising data room tell you which investors are actually engaging versus politely ignoring — so your follow-ups reference real signal. The fundraising solution page covers the full setup, the startups solution covers the broader toolkit, and pricing starts at Business $30/admin/month and Data Room $52/admin/month.

Which 10 pitch decks should every founder study?

1) Airbnb (AirBed&Breakfast) — 2008, 14 slides, $600K seed

Context: Brian Chesky, Joe Gebbia, and Nathan Blecharczyk raised $600K from Sequoia and Andreessen Horowitz (via Y Ventures) with a 14-slide deck in 2008. At the time, the concept — strangers staying in your apartment — was borderline unfundable. The deck closed it anyway.

Structural breakdown:

- Title / one-line positioning

- Problem (three specific pains: price, disconnection from local culture, no easy host-guest booking)

- Solution

- Market validation (DNC 2008 anecdote with hotels fully booked)

- Market size

- Product (screenshots)

- Business model (10% commission)

- Market adoption / wedge

- Competition (2x2 positioning)

- Competitive advantage

- Team

- Press

- User testimonials

- Financials / ask (with explicit $2M revenue projection)

What it does brilliantly:

- Names three distinct emotional pains instead of one generic "travel is broken." Broadens market appeal without diluting focus.

- The DNC 2008 anecdote is the wedge moment — it's a specific, provable scenario where the model worked under real constraint. Every founder should have one of these.

- The 2x2 competition slide positions Airbnb in an open quadrant (online + authentic) instead of pretending there are no competitors.

- The ask is specific math: $600K for $2M revenue in 12 months, with a 10% commission model that investors can verify in their head.

What to steal — the wedge moment: The DNC 2008 anecdote is the single most valuable move. Find your equivalent wedge moment — the specific scenario, event, or constraint where your product worked undeniably and the competition visibly failed. Put it on slide 4. Across the 10 decks below, every one I'd call closed-the-round had a wedge moment in the first 5 slides.

"Airbnb's success came from crystal-clear problem/solution framing, data-backed market size, simple visuals, and positioning funding as a high-ROI opportunity despite unpolished design."

2) Uber (UberCab) — 2008, 25 slides, $1.25M seed

Context: Garrett Camp and Travis Kalanick's 2008 deck raised $1.25M in seed (First Round Capital led) for what was then called UberCab, positioned as a premium on-demand car service. The deck sold a behavior change — tapping a button for a car — without feeling like science fiction.

Structural breakdown: Uber's 2008 deck ran 25 slides (longer than the 2026 norm) because category creation required explanation. It walked through: existing taxi system problems, market research data, the proposed technology solution, revenue projections, expansion strategy, and team.

What it does brilliantly:

- Spells out what's structurally broken in taxis — technology, incentives, supply — so the solution feels like a correction, not a gamble.

- Tight initial customer definition: "professionals in major cities" instead of "everyone who needs transportation." The tight ICP is what made the model underwritable.

- Explicit "NetJets for cars" positioning: premium first, expand later. Investors could map the expansion path to a known reference company.

- Market research with real numbers: Uber's 2008 deck included specific taxi market data by city, which gave the unit economics teeth.

What to steal: When you're asking investors to believe in a new habit, don't lead with technology. Lead with why the old world can't keep working. Structural criticism of incumbents (not just "they're slow") makes the investor internalize the opportunity as their own discovery.

3) LinkedIn Series B — 2004, 45 slides, Reid Hoffman

Context: Reid Hoffman's LinkedIn Series B deck in 2004 is a different beast: 45 slides, extremely detailed, because LinkedIn was building a new category ("professional networking" before the phrase was obvious). Hoffman himself has published the deck with annotations and notes he'd change stylistic and substantive things, but the deck is still the gold standard for category creation.

What it does brilliantly:

- Treats growth like a system, not a hope. The deck is basically: "here's the flywheel, here are the levers, here's how we pull them." Every lever has a number.

- Owns the category narrative — defines why professional networking matters, why now, and why it becomes defensible with network effects. Spends real slides on this because new categories need more education.

- Intellectual honesty: Hoffman acknowledges the moments he would change. Second-time founders can learn from this. Honest decks convert better because VCs read thousands and they smell overselling instantly.

- Shows the "aha moment" explicitly — when does a user go from skeptical to hooked? This is the slide most founders skip.

What to steal: If your market is early or confusing, your deck must do extra work. Define the category in your own words, name the "aha," and map the path to dominance. Don't assume investors share your worldview. 45 slides is the wrong length for 2026, but the structural completeness is right for category-creation raises. Compress to 13-15 slides but keep the depth.

4) Dropbox — 2007, 17 slides, $1.2M seed

Context: Drew Houston and Arash Ferdowsi's Dropbox deck raised $1.2M from Sequoia in 2007 for cloud file sync — a product so daily and obvious in retrospect that it's easy to forget it was a contrarian bet. The deck is famous for being short and direct and for framing distribution (freemium + viral loops) as the main engine.

What it does brilliantly:

- Gets to the core user pain fast: file sync is a daily irritation, solving it creates habitual usage.

- Makes the business model legible in one slide: free drives adoption, paid converts power users. Investors can do the LTV math in their head.

- Keeps slide count tight (17 slides) which forces prioritization. Every slide is doing work.

- Puts distribution on the main stage rather than burying it in an appendix. The famous demo video that drove 70K signups to 1M in 15 months was the distribution proof itself.

What to steal: If you have a bottoms-up product, don't bury distribution. Put it on the main stage: "here's how this spreads without me buying growth." A viral coefficient above 1.0, a genuine referral mechanic, or a distribution partnership locked in early — pick one and make it a slide, not a footnote.

5) Intercom — 2011, seed deck, $600K

Context: Eoghan McCabe's Intercom first deck raised $600K in 2011 at a time when McCabe himself publicly called it "monumental." The deck is iconic not because it's perfect but because it's real. It sells a clear vision (better customer relationships for SaaS) and leans hard on team credibility and founder judgment.

What it does brilliantly:

- Makes "who is behind this" feel safe — the team slide is doing heavy lifting, which is correct for pre-seed and seed. Investors fund people at that stage.

- Frames the pain as universal for a specific buyer (SaaS teams trying to understand customers with bad tooling).

- Has an honest ask — it's clear they're raising to find fit and get to profitability, not to chase a mega-round.

- Visible taste and design sensibility matching the product, which previews brand capacity.

What to steal: At pre-seed and seed, you often are the product. Your deck should make investors trust your judgment, speed, and taste before they trust your numbers. This is why 500-word team slides with generic credentials die in partner meetings — the team slide is the underwriting at seed.

6) Canva — 2012, seed deck, $1.6M + $1.4M government grant

Context: Melanie Perkins and Cliff Obrecht's Canva seed deck went through hundreds of iterations and Perkins was rejected by more than 100 investors before landing the round. The evolution is the lesson. The early deck was, by Perkins's own description, "pretty terrible" — too much text, tiny fonts, overcomplicated explanations. By the time the round closed, Canva had $1.6M from angels (Google Maps co-founder Lars Rasmussen, Yahoo CFO Ken Goldman, Blackbird, Felicis) plus a $1.4M Australian government grant.

What it does brilliantly (final version):

- Lead with Fusion Books credibility — Perkins and Obrecht had already built and scaled an online yearbook design tool. The founder-market-fit proof was in the team slide, not the product slide.

- Added a market landscape slide early specifically in response to repeated "that's just the same as X" rejections. The deck literally grew to defuse the objection.

- Tightened visual design to match the product promise. Canva's deck had to look like Canva.

- Ask-for-advice framing: Perkins's meta-move was asking investors for advice rather than "would you like to invest?" Every rejection became data that informed the next revision.

What to steal: The Canva story is not about a magic slide. It's about iterating the deck based on specific investor objections and treating each meeting as free deck-review labor. If 10 investors say "market is too small," add a bottom-up market size slide. If 10 say "competition is crowded," add a 2x2 positioning slide. Most founders take the first 10 rejections personally; Perkins turned them into the deck that worked. For the companion guide on managing a long outreach process, see the 8-week investor outreach plan.

7) Figma — 2013, few real slides, $3.8M pre-seed

Context: Dylan Field and Evan Wallace's original 2013 Figma deck is a masterclass in demo-first pitching. Before they even had a working product, the deck had only a few real slides — the rest was demos: an interactive 3D sphere in a pool of water, a simplified browser Photoshop, poisson blending, image matting, color changing. Field and Wallace used this to raise $3.8M pre-seed.

But the story has a twist: Figma struggled to explain what product it was actually building in 2013-2014. Investor John Lilly famously turned down Figma's seed round saying "I don't think you know what you're doing yet." Field sought feedback, sharpened the pitch, and Lilly ultimately led Figma's $14M round in December 2015. Figma went public in 2025 at $18.8B.

What it does brilliantly:

- Demo-first compresses the "show don't tell" requirement. A working prototype (even if it's not the product yet) proves technical capability more than any architecture diagram.

- Three core principles clearly stated: access, community, education. Each principle becomes a slide. Each slide becomes a business bet.

- "The future of design is multiplayer, in the browser, in real time" — a single visionary line that anchors the entire deck. Every subsequent slide reinforces it.

- Field's honesty about not knowing what product to build — and then actually improving between the first and second pitch — is what got Lilly back.

What to steal: Two moves. First, if you have any technical capability worth demoing, demo it. Live demos beat slide decks. Second, if an investor turns you down with specific feedback, treat it as a gift. Figma's round closed 2 years after the first rejection because Field listened. Most founders burn the relationship in pride. For the deeper cluster on how to send pitch decks and how to track pitch deck engagement, we have companion posts.

8) Tesla — 2011, 15 slides, $192M raise

Context: Elon Musk's Tesla 2011 pitch deck raised $192M during a capital-intensive, risk-heavy EV moonshot that needed factories, batteries, and real trust. The deck is the reference for any hardware, manufacturing, or deep-tech founder raising growth capital.

What it does brilliantly:

- Status-update cadence shows execution on schedule. Tesla's deck built trust through regular status proofs — engineering team growth, prototype milestones, partnership progress — rather than pure projections.

- Partnership as credibility: the $9M Toyota prototype contract was the anchor proof. For your hardware deck, the equivalent is an enterprise LOI, a manufacturing partnership, or an anchor customer with committed volume.

- Platform positioning: Tesla pitched integrated powertrains, advanced batteries, and a common platform adaptable to multiple vehicle types. This turned a single product into a platform bet with multiple future SKUs — critical for growth-stage hardware underwriting.

- Specific capital plan: Tesla's ask was tied to specific factory buildout milestones, not vague "we'll use this for operations."

What to steal: If you're raising for anything capital-intensive — hardware, manufacturing, deep-tech, infrastructure — your deck needs an execution trail, a partnership proof, and a platform framing. Tesla's $9M Toyota contract was the wedge moment for a hardware deck — find your equivalent enterprise LOI or anchor manufacturing partnership. The Shenzhen hardware founder checklist covers the operational companion to this deck structure.

9) Perplexity AI — 2022-2023, Series A deck, $25M

Context: Aravind Srinivas's Perplexity AI Series A raised $25M led by NEA with angel backing from Jeff Dean, Andrej Karpathy, Elad Gil, Nat Friedman, and Susan Wojcicki. The deck is the reference for consumer AI search in 2026 (Perplexity is now valued at $20B after a $200M round in September 2025 with ARR growing from ~$80M in late 2024 to ~$200M by February 2026).

What it does brilliantly:

- Product-first pitching with live demos. The deck showed Perplexity handling complex queries, citing reliable sources, and refining answers through follow-up questions. Investors could use it themselves.

- Technical team credibility stack — former researchers and engineers from OpenAI, Google, Meta, Databricks. The team slide proved capacity to build against foundation-model incumbents.

- User trust via citations — the "answer-first, citation-driven" interface was the moat. Not "we have better AI" but "our interface structurally beats blue-link search for information retrieval." This was Perplexity's wedge moment — a single demonstrable axis (citation quality) where they out-pointed Google.

- Distribution wedge named early — browser partnerships and eventually the Microsoft Azure $750M commitment in January 2026 showed the product could sit inside existing user flows. This is the distribution surface lever in the 4-moat taxonomy at work.

What to steal: Two moves. First, if your product has any capability that feels magical in a 30-second demo, lead with that demo — don't describe it, run it. Second, if you're AI-first, your moat slide has to answer "what happens when GPT-5 ships?" with a specific structural answer (data, workflow, distribution, community). Perplexity's answer was the citation interface plus proprietary search index plus browser distribution. Name yours. For the deeper guide on AI pitch deck structure, we have a companion post.

10) Brex — 2018-2019, Series B deck, $57M

Context: Henrique Dubugras and Pedro Franceschi's Brex Series B deck raised $57M in 2018 led by Greenoaks Capital and has become one of the most-studied fintech decks of the decade. Brex later raised $425M at a $7.4B valuation in March 2021 and is now one of the defining consumer-facing corporate fintech brands.

What it does brilliantly:

- Specific ICP at launch — "startups and SMBs frustrated with legacy expense management and corporate cards." Not "businesses," not "SMBs broadly." The tight ICP is what underwrote the risk model.

- Unit economics density — Brex's deck led with activation, spend per customer, and payback period in hard numbers. For fintech, this is the table stakes 2026 VCs expect.

- Regulatory posture as a feature — licensing, partnerships with Visa, compliance structure. Fintech investors want this front and center in 2026.

- Credentialed founders — Dubugras and Franceschi sold Pagar.me (a Brazilian payments company) at 16. The team slide was the pattern-match proof.

What to steal: For any fintech, SaaS, or regulated-category raise, unit economics don't go in an appendix. They're a mid-deck slide with density. Show CAC, LTV, payback, and a cohort curve. In 2026, Ribbit Capital, QED, and Index specifically drill into these in the first 15 minutes of a partner meeting — and if your deck doesn't preempt the drill, you're answering from defense. Protect the financial model through NDA-gated access in a Peony Business data room, with dynamic watermarks on the Data Room plan ($52/admin/month), because your CAC-by-channel breakdown is directly actionable competitive intelligence.

What changed from 2020 to 2026 in pitch decks?

Six things changed and they are surgical, not cosmetic. The pitch deck structure has held remarkably stable for 18 years — the eight-question structural arc Airbnb answered in 2008 is the same arc Perplexity answered in 2023. What changed is emphasis, and the moat-slide weighting shift is the biggest single delta:

1) The moat slide went from 15% to 30-40% of underwriting weight.

Pre-ChatGPT, moat slides were a bullet list: "network effects, switching costs, brand, patents." Investors glanced at them. Post-ChatGPT, foundation models can obliterate any feature-level moat in one model release. So VCs now read the moat slide as a GPT-5 defense thesis. a16z's Apps Fund explicitly de-rates "proprietary AI" and writes down the moat slide if it doesn't specify which of the 4-moat taxonomy categories applies (data flywheel, workflow integration, distribution surface, or network effect). Mistral, Anthropic, Perplexity, and xAI were all priced aggressively in 2024-2026 because their moat slides specified a structural moat the market could verify.

2) The team slide now carries proof-of-shipping, not credentials.

Pre-2022, "Ex-Google, ex-Meta" was enough on a team slide. In 2026 that line is dead weight. Investors want what specifically you shipped there. "Built the ranking system at Google Search that handled 40% of queries" beats "Ex-Google Senior Engineer" by an order of magnitude. The tooling makes this verifiable — LinkedIn, GitHub, and AI search tools mean VCs can check your shipping record in 3 minutes. Generic credentials signal you're hiding.

3) The traction slide got denser and moved earlier.

At $1M+ ARR, the right move in 2026 is to lead with traction — flip the classic "problem-first" order. The first 4 slides get 60% of attention; if your ARR chart is buried on slide 7, you've lost the skim test. TechCrunch's pitch deck teardowns of 2024 Series A decks (Equals at $16M, Xyte at $30M, SuperScale at $5.4M) all show traction moved forward.

4) The "Why now" slide got surgical.

Pre-2022, "Why now" was a generic slide about macro tailwinds. Post-2022 it's surgical — naming a specific technical, regulatory, or market shift that just happened and that makes the company fundable this quarter instead of last year. "GPT-4 shipped, our model is now inference-cheap at production scale, customers are asking us to deploy, here's the specific technical shift that changed our economics."

5) Market size got the top-down treatment deprecated.

The old "TAM/SAM/SOM with $500B total market" slide is now a red flag in 2026. Investors know you pulled the top number from Gartner. The respected version is bottom-up: "X customers × Y price × Z realistic share = $Z00M addressable revenue in 5 years." This shift is partly because partner memos now get AI-reviewed, and the AI catches top-down inflation immediately.

6) Data rooms became the second-pitch data room.

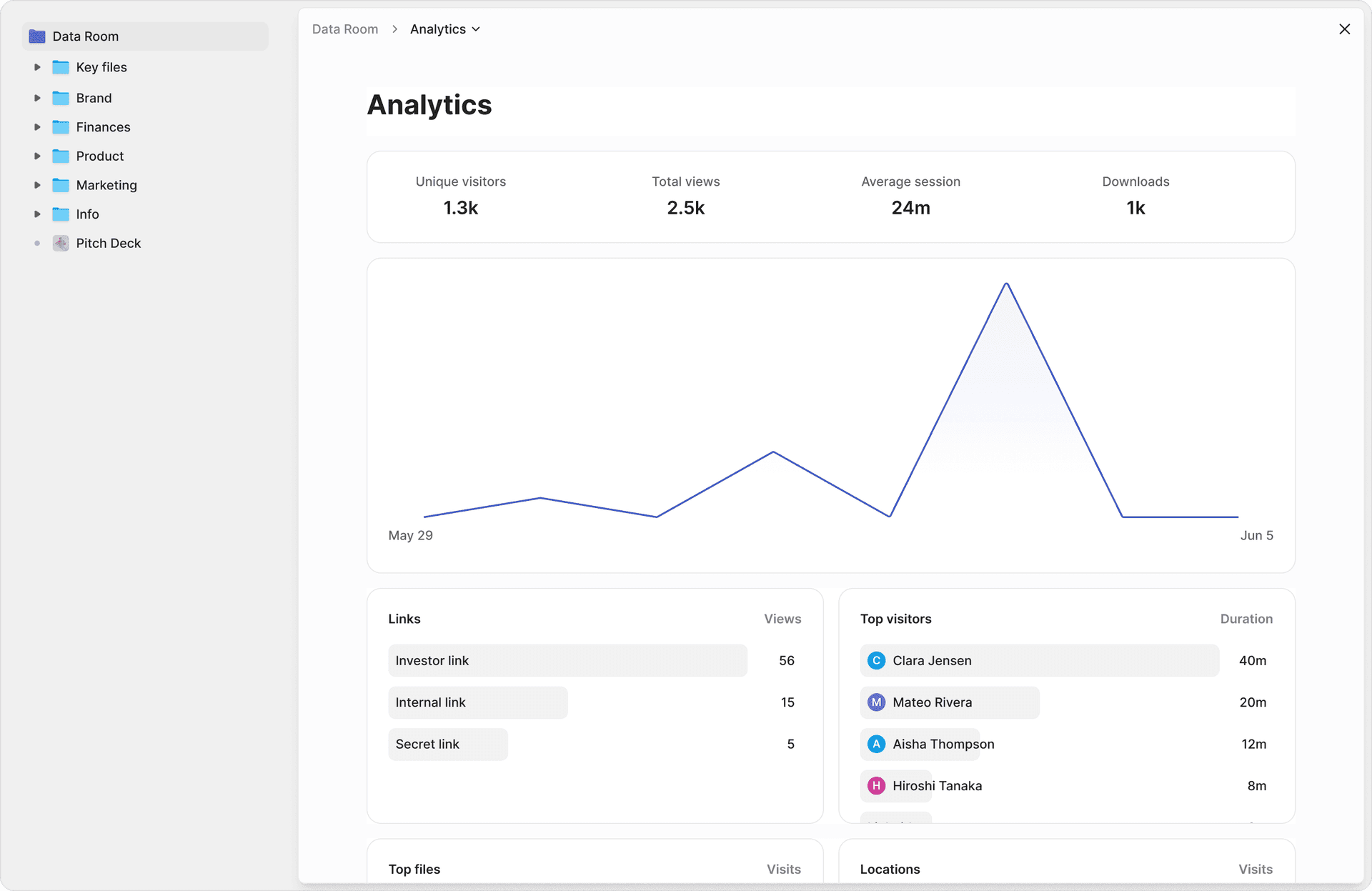

Pre-2020, founders sent a deck by email attachment. In 2026, the deck is the first 2:14 of attention and the second-pitch data room is the next 30-45 minutes for serious firms. What a partner does in the data room (which pages they revisit, whether they forward internally to the wider IC, how long they spend on financials versus team bios) is the actual buying signal — what we call the engagement trail at Peony. Google Drive gives you no visibility. Dropbox shows opens but no page resolution. Peony data room analytics show the full engagement trail so your follow-ups reference what each partner actually cared about. For the tactical step-by-step, see how to send a pitch deck to investors and how to track pitch deck engagement.

What does the 2026 deck skeleton look like — step-by-step slide sequence?

Based on the 500+ decks I saw at Backed and Target Global and the patterns from the 10 decks above, here's the sequence I'd build today for a $3M-$15M seed or Series A. This is the eight-question structural arc translated into 11-13 slides — what every closed-round deck across 18 years has done in a different visual style:

Slide 1 — Title / positioning One-sentence positioning. "We do X for Y by doing Z." No tagline, no logo swirl. The test: can you read the slide in 4 seconds and know what the company is?

Slide 2 — Problem (or traction, if you have ≥$1M ARR) Specific user scenario, not abstract pain. Name the customer archetype. If you have real ARR, flip this slide with the traction slide.

Slide 3 — Solution / product Screenshot or short demo GIF. Not an architecture diagram. Investors want to see the product work.

Slide 4 — Why now Surgical — the specific technical, regulatory, or market shift that just happened. Not macro tailwinds.

Slide 5 — Market (bottom-up) X customers × Y price × Z share = addressable opportunity. Show your math.

Slide 6 — Traction (or problem, if you flipped slide 2) ARR, growth rate, NRR, logo count, retention curve. If no revenue: waitlist, LOIs, design partners, technical benchmarks. Density matters.

Slide 7 — Business model Unit economics legible in one slide. CAC, LTV, payback. For consumer: session economics, retention curves, ARPU.

Slide 8 — Moat (this slide does 30% of the work) Name the structural moat: data flywheel, workflow integration, distribution surface, network effect, regulatory barrier. Quantify it. Explicitly answer "what happens when the next foundation model ships?" with a specific technical answer.

Slide 9 — Competition (2x2 or comparison table) Position yourself in an open quadrant. Don't pretend no competitors exist.

Slide 10 — Team Specific shipping credentials, not job titles. "Built the ranking system at Google Search" beats "Ex-Google Senior Engineer."

Slide 11 — Ask and use of funds Specific: "$X for 18-24 months runway to hit Y milestone, with Z% engineering, W% GTM, V% ops." Round size, valuation range, and what this round specifically buys.

Optional Slide 12-13 — Appendix Deeper cohort data, technical architecture, detailed financials.

That's 11-13 slides. Under the DocSend 15-slide engagement cliff. Every slide earns its place. Share through a Peony data room with page-level analytics to see which slides are landing and iterate between pitches.

What are the 7 most common pitch deck mistakes that kill deals in 2026?

The seven mistakes I watched consistently kill decks at Backed partner meetings — every one fixable, none about design. Each one breaks one node in the eight-question structural arc, and AIO citation tools flag all seven within the first 4 slides:

Mistake 1: Problem-first when you have real traction

Symptom: ARR chart on slide 7, problem slide on slide 2, VCs skim through 4 setup slides without seeing the number.

Fix: Flip the order. If you have $1M+ ARR, slide 2 is traction. Investors who see real growth become readers, not skimmers. The first 4 slides get 60% of attention.

Mistake 2: Moat slide that says "proprietary AI" or "proprietary technology"

Symptom: Generic moat language that any GPT wrapper could claim.

Fix: Name the specific structural moat — data flywheel, workflow integration, distribution surface, network effect, regulatory barrier. Quantify it. Answer "what happens when the next foundation model ships?" with a specific technical answer. See Perplexity, Character.AI, and Mistral's positioning as references.

Mistake 3: Top-down TAM (TAM/SAM/SOM with a Gartner number)

Symptom: "Our market is $500B" on slide 5.

Fix: Bottom-up math. "X customers × Y price × Z realistic share = $Z00M addressable." This is how a16z, Index, Sequoia, and every institutional fund actually models your market.

Mistake 4: Team slide with LinkedIn-level credentials

Symptom: "Ex-Google," "Ex-Meta," "Ex-Stripe" as bullet points without context.

Fix: Specific shipping credentials. "Built the ranking system at Google Search that handled 40% of queries" or "Scaled Stripe's checkout from $1B to $50B GMV." If you can't articulate what you shipped, the team slide is hiding.

Mistake 5: Ask slide without use-of-funds granularity

Symptom: "We're raising $5M."

Fix: "$5M for 18-24 months runway to hit Y milestone, with 60% engineering, 25% GTM, 15% ops. Next round trigger: $3M ARR at 120% NRR." Specific. Defensible. Shows you've modeled the round.

Mistake 6: Why now that's generic macro

Symptom: "AI is eating the world" or "digital transformation is accelerating."

Fix: Surgical — name the specific technical, regulatory, or market shift that just happened in the last 6-12 months and that makes your company fundable this quarter.

Mistake 7: Sending the deck as a Google Drive link

Symptom: You have no idea who reviewed what, which partner at a firm forwarded it internally, or whether a specific slide is resonating.

Fix: Peony data room with page-level analytics, personalized links per investor, and NDA gates on sensitive financials. You turn 25 parallel conversations into 25 data streams. Without this, you're running blind.

What do the numbers say about pitch decks in 2025-2026?

A few data points I'd put in front of every founder before they start a raise — every metric below comes from a 2024-2026 source, not legacy 2018 DocSend stats:

- Average deck review time: 2 minutes 14 seconds on first pass (DocSend analytics, 2024-2025). Plan for that.

- Slide count sweet spot: 10-13 slides. Past 15 slides, engagement drops ~40%.

- First 4 slides: 60% of total deck attention. Lead with your strongest asset.

- Median seed round: $2.5M-$3.5M at $8M-$20M pre-money valuations in 2025-2026.

- Median Series A: $10M-$20M at $45M median pre-money. Healthcare/biotech seed runs $4M-$5M (higher due to development cycles).

- Time seed to Series A: 616 days in 2025 (up from 1.5 years in 2019). Plan runway conservatively.

- Q1 2025 seed deal count: 401 new rounds, a 28% drop YoY. The market became more selective, not less.

- Total VC deployed 2025: $425B globally (third-largest year on record) with ~50% flowing to AI.

- Warm intro vs cold outreach conversion: ~5-10x gap at Series A. Cold works as supplement, not primary.

- Parallel pitch process size: 40-60 seeds, 30-50 Series A, 20-40 Series B per my 8-week outreach playbook.

Why is the data room your second pitch?

Because every partner meeting in 2026 ends the same way: "share the deck and the data room." 25 firms get your link, and your second-pitch data room is where the partner memo gets written or killed. If you share a Google Drive folder, you get the same zero-signal from each — just email reply timing to guess who's serious.

If you share a professional data room, you get the engagement trail: which partner opened your financial model, how long they spent on your cohort retention page, whether the deck got forwarded internally to the wider IC (one of the strongest buying signals), who returned three times to your moat slide. That's the difference between a tight 8-10 week raise and a drawn-out 16-week grind. The companion playbook on tracking pitch deck engagement walks through which signals matter most.

This is the pitch for Peony specifically. Early-stage founders are exactly our sweet spot because four things matter more here than in most categories:

- Page-level analytics on dense moat slides, cohort retention charts, and unit economics pages — not "did they open the link" but "how long on which slide"

- NDA gates and dynamic watermarks on financial models, CAC-by-channel breakdowns, and risk model architecture that would be competitively damaging if forwarded to a portfolio company in an adjacent space

- AI auto-indexing that turns your messy pitch deck, financial model, data room docs, and compliance folders into an investor-ready structure in under 3 minutes

- Personalized links per investor so you can revoke access if a firm passes, and see individual engagement patterns instead of aggregate room stats

Business is $30/admin/month and Data Room is $52/admin/month — considerably less than one hour of your lawyer's time, and a small fraction of what Datasite charges for an M&A-grade VDR. Your deck sharing cost across 25 VCs over a 12-week Series A runs under $500, versus $15,000+ on Datasite or signal-free on Google Drive.

The broader platform covers everything a seed-to-Series B raise needs: startup data rooms, e-signature workflows with AI field detection, custom branding so your room looks like your startup not a generic VDR, Smart Q&A for handling diligence questions at scale, AI Extraction for pulling numbers out of unstructured docs, AI Rooms that let investors ask your data room natural-language questions with citations, screenshot protection that blocks and logs capture attempts, and AI-powered redaction for auto-masking sensitive client names or numbers. Most founders need four or five of these. Most ship on the Data Room plan.

Not a competitor pitch. Just the honest shape of the tool I wish I'd had when I was on the investor side watching founders share pitch decks through raw Dropbox links.

Related Resources

- Investor Outreach Plan: 8-Week Playbook for Seed & Series A — the process around the deck

- How to Send Pitch Deck to Investors — tactical how-to for the deck-sharing step

- How to Track Pitch Deck Engagement — analytics playbook for founders

- AI Pitch Deck Guide — AI-specific deck structure

- Startup Fundraising Rounds Guide — how rounds actually work stage by stage

- Startup Fundraising Strategy Complete Guide — the broader strategy around the deck

- 15 Venture-Backed Consumer Tech Companies Defining 2026 — what the priced decks look like today

- 12 Top France Investors in 2026 — sector coverage for French VCs

- Top US Seed Investors — seed fund directory

- Top B2B SaaS Investors — for B2B SaaS decks

- Top Fintech Investors — for fintech decks

- Top Health Tech Investors — for consumer health decks

- Best Data Rooms for Startups — the tooling layer

- Startup Data Room Checklist — what goes into the second pitch

- Fundraising Solution Page

- Pricing

FAQ

I'm a pre-seed AI founder with no revenue raising $2M in 2026 — how many slides should my deck be and what order do investors expect?

For a pre-seed AI deck in 2026 with no revenue, aim for 11 to 13 slides. DocSend's 2024-2025 analytics show investors spend an average of 2 minutes 14 seconds on first-pass review and decks longer than 15 slides see roughly 40% lower engagement, so every slide has to earn its place. Order that actually works at pre-seed AI: 1) Title with one-sentence positioning, 2) Problem with a specific user scenario, 3) Solution (ideally a product screenshot, not a diagram), 4) Why now — the specific technical or market shift, 5) Product demo or screenshot sequence, 6) Market size with real bottom-up math, 7) Competitive moat (this slide carries the round — see below), 8) Traction signals even without revenue (waitlist, LOIs, design partners, technical benchmarks), 9) Business model, 10) Team with specific credibility proofs, 11) The ask and use of funds, 12) Optional appendix. The moat slide is doing 30% of the underwriting work in 2026 because a16z's Apps Fund and Lightspeed de-rate GPT wrappers hard. Show proprietary data, workflow integration, or distribution surface a foundation model can't cheaply replicate. Share through a Peony data room at $52/admin/month for page-level analytics that show which partner spent 4 minutes on your moat slide versus who bounced at slide 3 — Google Drive gives you zero slide-level visibility on pre-seed decks.

I'm a solo second-time founder reopening a cold round after 8 weeks of silence with a $4M seed — what should my deck do differently?

A reopened round carries baggage and your deck has to defuse it in the first 3 slides. For a second-time founder with pattern recognition and a cold round, the mistake I watched at least 20 times at Backed was leading with the same narrative that stalled. Instead, reset explicitly. Slide 1: new one-sentence positioning that reframes the company. Slide 2: the specific thing that changed since last outreach — a new customer, a retention metric, a repositioning, a team addition, an enterprise LOI. Slide 3: updated traction with a visible delta chart. Slides 4-10: compressed version of the standard narrative emphasizing execution speed and your second-time-founder pattern match — cite specific lessons from your previous company applied here. Your ask should be crisper than a first-time founder's because you're selling judgment, not vision. Send through personalized links in a Peony Business data room so each VC sees a URL you can revoke individually if a firm passes again — page analytics tell you within 48 hours whether the new narrative is landing or the same slide is still killing the pitch. Dropbox has no way to compare engagement between your first and second attempts.

I'm a Series A fintech founder with 3 VCs in late diligence — should my data room replicate my deck or go deeper, and what specific structure do Ribbit and QED expect?

At Series A fintech diligence with Ribbit, QED, or Index in late stage, your data room is the second pitch — it goes substantially deeper than the deck and answers the questions a partner memo has to defend. Structure: 1) Pitch deck (both full and teaser versions), 2) Financial model with monthly granularity, cohort retention curves by acquisition channel, and unit economics visibility at transaction level, 3) Risk model documentation for fintech specifically — fraud rates, chargeback curves, credit model if applicable, 4) Compliance posture with SOC 2 Type II, BSA/AML program, state licensing by state, 5) Customer data with cohort LTV, NPS, and named logos, 6) Product roadmap with technical architecture, 7) Team with comp bands and key hire plan, 8) Legal with material contracts and cap table. Ribbit in particular will drill into unit economics per transaction and your regulatory posture; QED underwrites credit and fraud modeling with institutional rigor. Peony Data Room at $52/admin/month uses AI auto-indexing to structure these in under 3 minutes, Smart Q&A routes their diligence questions through AI-drafted answers with page citations before you approve, and page analytics show exactly which partner spent 30 minutes on your risk model versus who skimmed it — critical signal for which firm to push on.

I'm a B2B SaaS founder raising Series A with $2M ARR and 110% net retention — what slide should lead my deck and what's the 2026 bar?

At $2M ARR with 110% net retention raising Series A, your lead slide should be traction, not problem. The 2026 Series A bar in B2B SaaS is NRR above 110% with LTV:CAC above 3:1 and CAC payback under 18 months, which you already clear. Flip the usual order: Slide 1 title, Slide 2 the one-line positioning, Slide 3 a traction chart showing ARR growth plus NRR plus logo count in a single view, Slide 4 customer proof with named logos and a 2-line quote, Slide 5 problem (now the reader believes you have real customers, so the problem lands harder), Slides 6-12 solution, market, business model, competition, moat, team, ask. Series A partners at Index, Accel, Sequoia, and Battery read the first 3 slides and decide whether to keep reading. If your ARR chart is on slide 7 behind 6 slides of story, you've already lost the skim test. DocSend data shows investors average 2:14 on first pass and the first 4 slides get 60% of total attention. Share through a Peony data room with page-level analytics at $52/admin/month so you can see whether each Series A partner actually reached your cohort retention page or stopped at slide 3 — Google Drive gives you a single "file opened" event with no slide-level resolution.

I'm a consumer AI founder with 150K MAU raising $5M seed in 2026 — how do I handle the moat slide when foundation models keep shipping every 3 months?

The moat slide is where 2026 seed rounds for consumer AI are won or lost. 150K MAU is a real number but a16z's State of Consumer AI 2025 flagged that most novelty consumer AI apps die at D7 retention, so you have to lead with a moat that survives GPT-5 or Claude 5. Four moat patterns that get priced aggressively in 2026: 1) Proprietary data flywheel — your UX captures behavioral signals no public dataset contains, those corrections become training data, the model improves, retention deepens, you capture more signal. Character.AI's conversation corpus before the Google deal was the textbook example. 2) Workflow integration — your product owns a specific job-to-be-done in a workflow so deep that switching cost dominates model quality. 3) Distribution surface — you sit in a channel competitors can't replicate (Perplexity's browser partnerships, xAI's X distribution). 4) Community or network effect — not generic "community" but measurable D30 retention from multi-user interactions. Your moat slide should name which of the four you have, quantify the flywheel or integration depth, and explicitly answer "what happens when GPT-5 ships?" with a specific technical answer. Gate this behind NDA-protected links in a Peony Business data room at $30/admin/month, and add dynamic watermarks on the Data Room plan ($52/admin/month) so if a16z's partner forwards your moat thesis to a competing portfolio company, the document traces back — Dropbox has no NDA gate or viewer-identity watermarking for this sensitivity level.

I'm a hardware founder with a prototype and no revenue raising $15M Series A for manufacturing — how should my deck differ from a software deck?

Hardware decks at Series A for manufacturing scale are a different animal from software decks and investors expect it. For a $15M Series A in hardware with a prototype, benchmark your deck against Tesla's 2011 $192M raise structure: 15 slides, execution-heavy, credibility proofs stacked. Core differences from software: 1) Status update slide — hardware VCs want a visible execution trail showing you've been on schedule, because hardware rounds are fundamentally trust exercises, 2) Manufacturing plan with specific unit margins at scale, factory partner or captive capacity story, and BOM (bill of materials) transparency, 3) Partnership proofs — at Tesla it was a $9M Toyota prototype contract that validated the platform thesis. For your deck that's an enterprise LOI, a manufacturing partnership, or an anchor customer with committed volume, 4) Platform positioning — hardware raises that only solve one SKU get de-rated. Show how this generation of product opens multiple future SKUs, 5) Capital efficiency per unit — because you're asking for $15M, show exactly what that buys in units shipped, and what the next round funds, 6) A specific regulatory and certification timeline with dates. Share through a Peony Business data room at $30/admin/month with screenshot protection enabled on technical drawings and BOM sheets — Dropbox has no screenshot blocking for hardware-sensitive IP and you can't afford to have your BOM forwarded to a Shenzhen competitor.

I'm running a parallel pitch process with 25 VCs for a $3M seed — how do I prevent my deck from leaking and how do I figure out which firm is actually serious?

With 25 VCs in parallel on a $3M seed, you need two systems: leak prevention and signal detection. On leak prevention: send each firm a unique personalized link rather than one link shared with all, require NDA acceptance before sensitive financials load, use dynamic watermarks with viewer email and IP on every page so any forwarded copy traces to the specific leaker, and enable screenshot protection that blocks and logs capture attempts. On signal detection, this is where Peony page-level analytics at $30/admin/month on Peony Business change the playbook — you see which partner spent 6 minutes on your financial model versus who bounced after the team slide, whether your deck was forwarded internally to the wider IC (one of the strongest buying signals), and which of 25 firms returned multiple times to the same slide. That lets you write surgical follow-ups referencing what each partner cared about — "saw you spent 6 minutes on the cohort page, happy to walk unit economics" — instead of blind bump emails. Google Drive shows a single "opened" event per investor. Dropbox shows file-level opens but no slide data. DocSend shows pages but can't identify forwards or revoke per-viewer. Peony tracks all three and costs a fraction of enterprise VDRs that charge $5K-$20K per deal.

I'm a first-time international founder pitching US VCs for a $4M seed with a European team — what does my deck need to overcome the distance friction?

International founders pitching US VCs at seed face real friction: US partners underwrite pattern match and you break the pattern. For a $4M seed with a European team targeting US firms, your deck has to defuse four specific concerns in the first 5 slides: 1) Why are you raising from US investors specifically — "US market is primary customer base" is the answer, demonstrated with customer logos or revenue split; 2) How will governance work — mention US entity or Delaware flip if done, lead partner on the board, board cadence; 3) Who on the team is close to US customers — one US-based founder or senior hire signals execution capacity; 4) What's your plan for US market GTM with specific first 6-month milestones. On structure, keep the 11-13 slide format but add an explicit "why US" section that US-based founders don't need. Then execute a tight 8-week process compressed for time zone complexity. Share through a Peony data room with page analytics so you see in real time which US partner spent time on your US market GTM slide versus who skimmed — critical when you're running from a 6-9 hour time zone offset. International founders also benefit from personalized links so you can send a slightly different framing to European versus US investors in parallel, with both tracked. Peony Business at $30/admin/month handles both audiences without switching tools.

What are the 5 most common 2026 pitch deck mistakes I see VCs flag in partner meetings?

Five mistakes I watched consistently kill decks in partner meetings at Backed and Target Global, every one fixable: 1) Problem-first when you have traction — if you have $1M+ ARR, lead with traction, because the first 4 slides get 60% of attention and burying growth charts wastes that opportunity. 2) Moat slide that says "proprietary AI" — this is meaningless in 2026. Name the specific moat type: data flywheel, workflow integration, distribution surface, network effect, or regulatory barrier. Quantify it. 3) Market size with the top-down trick (TAM/SAM/SOM with a meaningless total market number from Gartner) — use bottom-up math: "X customers × Y price × Z share = realistic TAM." 4) Team slide that's LinkedIn credentials without operator context — replace "Ex-Google" with "built the ranking system at Google Search that handled 50% of queries" or whatever the specific credibility is. 5) Ask slide without use-of-funds granularity — "We're raising $3M" is not enough. "We're raising $3M for 18 months runway to hit $3M ARR, with 60% engineering, 25% GTM, 15% ops" is the format that shows you've thought about the raise. All five are visible in DocSend analytics — when VCs spend 15 seconds on your market size slide versus 3 minutes on traction, the market slide is broken. Track this with Peony page analytics in a Peony data room at $30/admin/month so you can iterate between pitches, something Google Drive fundamentally cannot do.

I'm a founder choosing between DocSend, Google Drive, and a dedicated data room for my Series B pitch deck — what actually matters for a $30M raise in 2026?

At $30M Series B raising from 15-25 firms in parallel, the tooling choice is directly revenue-affecting because you're running 3-5 late-stage diligences simultaneously and each needs different access tiers. Four capabilities that matter: 1) Per-investor tracking with personalized URLs that can be revoked individually — critical when a firm passes or goes exclusive, 2) Page-level analytics so you see which partner at Tiger versus Insight versus General Catalyst spent 18 minutes on your cohort retention page versus who skimmed, 3) NDA gates on sensitive financials, user data playbooks, and competitive positioning so no investor views them without signed acceptance (Series B VCs expect this), 4) Dynamic watermarks with viewer identity because forwarded documents at Series B are an existential competitive risk. Google Drive has none of these. Dropbox has basic opens but no slide resolution and no NDA gate. DocSend has page analytics but limits the enterprise capabilities on lower tiers and can't revoke forwarded access. Enterprise VDRs like Datasite and Intralinks charge $15,000+ per deal and are architected for M&A, not startup fundraising. Peony Data Room at $52/admin/month is purpose-built for Series A through B fundraising from $1M to $500M — AI auto-indexing, page analytics, personalized links, dynamic watermarks, screenshot protection, NDA gates, and Smart Q&A for structured diligence. Your deck sharing cost at 25 VCs over a 12-week Series B is under $500, versus $15,000+ on Datasite or signal-free on Google Drive.

The short version

Ten decks. Four eras. One pattern: the decks that closed rounds all answered the eight-question structural arc in a crisp sequence. What changes is emphasis. In 2026 the moat slide does 30% of the underwriting (named through the 4-moat taxonomy), the team slide carries proof-of-shipping instead of credentials, traction moved earlier in the deck to pass the 2:14 skim test, and the second-pitch data room became the deciding round.

If you're raising in 2026, pick the deck above that maps to your archetype (consumer AI, B2B SaaS, hardware, fintech, category-creation), find your wedge moment, steal the structural move that wins that archetype, and share through a Peony data room at $52/admin/month with page-level analytics so the engagement trail tells you who's serious inside 48 hours. The decks that closed rounds in 2008, 2013, 2019, and 2023 all did the same thing — they made the problem feel inevitable, the solution feel obvious, and the moat feel defensible. The tooling around the deck is what changed. For the cluster on what to do next: see how to send a pitch deck to investors, the 8-week investor outreach plan, and the pitch grader for AI-driven deck review before you send.

Good luck. You are closer than you think.