International Tax Due Diligence in M&A: A Buyer's Guide (2026)

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

International Tax Due Diligence in M&A: A Buyer's Guide (2026)

I'm Deqian Jia, co-founder of Peony. Tax teams run cross-border diligence inside our data rooms every week, and the same pattern repeats: the buyer's checklist covers the domestic questions well, and then the deal crosses a border and the exposures stop living in tax returns and start living in the structure — in the flows between entities, in where people sit, in whether a holding company is real. Cross-border deals reached 39% of mid-market M&A in 2025, up from 33% the year before. Most tax DD guides still read as if every target files in one country.

This guide is the international layer: what to test, what changed in 2025-2026 (a lot), and — the part that actually decides outcomes — how to convert each finding into deal protection before you sign.

Quick answer: International tax due diligence is the buyer-side review of a target's cross-border tax position: transfer pricing defensibility, permanent establishment risk, withholding leakage on repatriation, Pillar Two exposure, indirect transfer taxes on the deal itself, and holding-company substance. It is not a compliance review — it is an exposure-pricing exercise. Every finding lands in one of four buckets: walk (rare: fraud, or exposure near the equity check), price chip (quantified and near-certain), escrow (uncertain but boundable, typically 36-60 months for tax), or specific indemnity (known and named, surviving to the statute of limitations plus 60-90 days). Budget $100K-$250K and 6-12 weeks for a six-country mid-market target, and stage the data room per jurisdiction before the clock starts.

What is international tax due diligence, and how is it different from domestic tax DD?

International tax due diligence is the workstream that tests how a target's tax position behaves across borders: whether intercompany pricing survives audit in each country, whether people and activities have quietly created taxable presence where no entity is registered, how much tax the cash loses on its way back to the parent, whether the global minimum tax regime touches the group, whether the transaction itself triggers tax in a country neither party lives in, and whether the holding structure has enough substance to keep its treaty benefits.

Domestic tax DD asks: did the company pay its taxes, and are the returns defensible? International tax DD asks a harder question: does the structure survive contact with six tax authorities at once — each with its own statute of limitations, its own audit posture, and its own claim on the same dollar of profit. The exposures compound rather than add, because a transfer pricing adjustment in one country creates double taxation in another unless a treaty process fixes it, and a permanent establishment finding drags payroll, VAT, and registration obligations behind it.

One scope note before the detail: this guide covers the cross-border layer only. For the full domestic-first framework — the eight pillars, the document checklist, and how tax DD fits alongside the other workstreams — use our tax due diligence checklist. The two are designed to run together: that post tells you what to collect; this one tells you what kills or reprices cross-border deals.

What changed in 2025-2026? The new cross-border baseline

More moved in the last 18 months than in the previous decade. If your tax DD template predates mid-2025, it is testing the wrong regime.

| Change | Effective | What it means in diligence |

|---|---|---|

| OECD side-by-side framework: US-parented groups excluded from other countries' IIR and UTPR | Fiscal years from Jan 1, 2026 (agreed as OECD guidance Jan 5, 2026) | US-parented targets keep QDMTT exposure in each local jurisdiction; FY2024-25 IIR/UTPR exposure is still live history; relief in any given country depends on local transposition, which lags |

| OBBBA: GILTI becomes Net CFC Tested Income (NCTI) | Tax years beginning after Dec 31, 2025 | Effective rate 10.5% → 12.6%, tangible-asset carve-out (QBAI) eliminated, 90% of foreign taxes creditable — roughly 14% foreign ETR now zeroes US residual tax; rerun the model, old GILTI math is wrong |

| OBBBA: Section 954(c)(6) CFC look-through made permanent; pro-rata rules now allocate by days held | Tax years beginning after Dec 31, 2025 | A recurring diligence expiry cliff is gone; mid-year closings now split the CFC inclusion between buyer and seller — negotiate the straddle-year allocation in the SPA |

| Transitional CbCR safe harbour extended one year | Now covers fiscal years beginning on or before Dec 31, 2027 (17% ETR test in FY2026-27) | In-scope groups can defer full GloBE calculations — but an acquisition can permanently break eligibility ("once out, always out"), so test it before close, not after |

| First GloBE Information Returns due | June 30, 2026 for calendar-year FY2024 adopters | A target near EUR 750M should already have GIR-grade data; its absence is itself a finding |

| Brazil: 10% withholding on dividends to non-residents (Law 15,270/2025) | Jan 1, 2026 | Dividends were previously exempt, and there is no US-Brazil treaty — every repatriation model with a Brazilian sub built before 2026 is stale |

| OECD Model Tax Convention 2025 update: remote-work PE framework | Published Nov 19, 2025 | First workable test for home-office PE: under 50% of working time is generally safe; above it, the arrangement needs a genuine commercial reason — employee preference does not count |

| India abolishes the equalisation levy; Pillar One stalls; DSTs persist in France, Italy, Spain, UK, Austria, Turkey | Levy removed Apr 1, 2025; Pillar One shelved after the US withdrawal | Digital-economy targets: DST registrations and US Section 301 retaliation risk are now a standing diligence item rather than a transitional one |

The rest of this guide walks the six exposure areas in the order they most often move price, then the deal mechanics that turn findings into protection.

Is the target's transfer pricing documentation actually defensible?

Start here, because transfer pricing is both the most common cross-border finding and the one whose exposure base — the target's intercompany flows — is knowable on day one. The three-tier OECD stack sets the frame: a Country-by-Country Report if the group clears EUR 750M in consolidated revenue (USD 850M for US-parented groups filing Form 8975), plus a master file and local files at much lower, country-specific thresholds — Germany requires a master file above EUR 100M in revenue and local documentation at just EUR 6M of cross-border goods flows, France at EUR 150M, India at roughly USD 60M of group revenue. A mid-market target that says "we're too small for transfer pricing documentation" is usually wrong about at least two of its countries.

What thin documentation costs, by regime:

- United States: a net Section 482 adjustment above the Section 6662(e) thresholds carries a 20% penalty, rising to 40% for gross misstatements — and the contemporaneous-documentation defense only works if the docs exist when the return is filed and are produced within 30 days of an IRS request.

- Germany: a 5-10% surcharge on the income adjustment (minimum EUR 5,000), late-production fines of at least EUR 100 per day — and since 2025, only 30 days to produce documentation on request, down from 60.

- India: 2% of the transaction value for missing documentation, plus a penalty of up to 200% of the tax on the adjustment (Section 270A: 50% for under-reporting, 200% for misreporting).

The red flags that predict adjustments are behavioral, not cosmetic. The most common failure pattern we see in diligence is the benchmarking-vs-agreement gap: intercompany agreements signed at one point, benchmarking studies run at another, and nobody ever reconciled the two — the gap between them is the adjustment base, gift-wrapped. Close behind: agreements drafted after the flows they govern, a "low-risk" contract manufacturer or distributor reporting volatile margins, year-end true-ups used as a margin plug (ask whether retroactive price adjustments are even permitted in both jurisdictions — many disallow them, stranding the true-up), persistent losses in one local entity while the group prospers, and management fees or IP royalties flowing to an entity with no people.

Sizing the exposure is arithmetic once you have the flow matrix: adjustment risk on each flow × the local rate and penalty regime × the open years under each country's statute of limitations, typically 4-7. Then decide the bucket. Defensible economics with thin paper is a specific-indemnity item plus a remediation budget. Economics that do not hold at arm's length is a price chip, because that liability recurs every year you own the company.

Does the target have a permanent establishment it never registered?

A permanent establishment is taxable presence without a legal entity — and it is the exposure most likely to be invisible in the data room, because by definition the target never filed where the PE sits. The classic triggers: a fixed place of business, a construction or installation project running past 12 months (6 months under many treaties with developing countries), and — the one that bites mid-market software and services companies — a dependent agent: a country manager or salesperson who habitually negotiates and effectively concludes contracts locally while the entity books revenue from abroad.

Remote work turned this from an edge case into a standing diligence item, and 2026 is the first year with a usable test. The OECD's November 2025 Model update sets a two-part framework: an employee working from home under 50% of their working time over any 12-month period generally does not create a fixed place of business; above 50%, the arrangement must serve a genuine commercial purpose — and the commentary says explicitly that employee preference, talent retention, and office-cost savings do not qualify. The framework is new enough that enforcement is uneven: a KPMG survey of 63 jurisdictions found only 25% have issued specific remote-work PE guidance. Uncertainty like that does not mean the risk is small — it means the finding is hard to close out, which is exactly what escrows are for.

The diligence method is a three-way map: headcount and contractors by country (from payroll and AP data, not the org chart) against the legal entity chart against the contract-approval matrix. Every country with revenue-generating people and no registered entity gets a flag; every flagged country gets the follow-up questions — who negotiates, who signs, how long has this run. Quantify a finding as the profits attributable to the PE × the local corporate rate (India taxes a foreign company's PE at 35% plus surcharge and cess, the base rate since April 2024), plus interest and penalties across open years, plus the payroll and VAT registrations that ride along. And check the contractor roster twice: a "contractor" who works exclusively for the target, on target systems, with a target title, is a misclassification and a PE fact pattern in one.

How much withholding tax will repatriation actually leak?

The deal model assumes cash in a foreign subsidiary is worth face value to the buyer. Withholding tax is where that assumption dies quietly. Every dividend, interest payment, and royalty crossing a border loses a statutory percentage unless a treaty reduces it: the US withholds 30% on outbound FDAP payments, India takes 20% (plus surcharge and cess) on dividends and roughly 21.8% effective on royalties and technical-service fees, and Brazil — the 2026 landmine — now withholds 10% on dividends to non-residents under Law 15,270/2025, ending a decades-long exemption, with no US-Brazil treaty available to soften it.

Treaty relief is not automatic; it is gated twice. The recipient must be the beneficial owner of the income, and the arrangement must survive the principal purpose test that the MLI wired into most treaties — benefits are denied if obtaining them was one of the principal purposes of the structure. The Danish beneficial ownership cases (CJEU, 2019) are the template authorities now apply: EU holding companies that were mere conduits — no people, no discretion over the cash, back-to-back flows — were denied withholding exemptions outright. If the target's structure routes income through a Luxembourg or Cyprus entity with no employees, assume the reduced rate is contestable and model both cases.

In diligence, build the repatriation path explicitly: each operating company → each intermediate holdco → the parent, applying the statutory rate, the claimed treaty rate, and the realistic rate (post-PPT) at every hop. Sum the leakage on the cash you are counting in the equity bridge. Where the number is material, the fixes are structural and mostly pre-close: qualify the holdco properly, re-route the path, extract pre-closing dividends at the seller's cost, or discount trapped cash — balances whose exit cost exceeds their carrying value — in the bridge itself rather than pretending they travel free.

Is the target in Pillar Two scope, and does anyone actually owe top-up tax?

For most mid-market deals the honest answer is "not yet, but check twice" — and both checks have M&A-specific traps.

Scope first. The GloBE rules apply to groups with EUR 750M+ consolidated revenue in at least 2 of the 4 preceding fiscal years. A standalone $150M EV target is nowhere near it. The trap is the merger rule: when groups combine, Article 6.1 of the Model Rules aggregates their separately reported revenues for the prior years — so a bolt-on into a platform that consolidates its acquisitions can pull the whole combined group into scope, effective from the acquisition date. A fund-level buyout through a standard non-consolidating private equity structure generally does not aggregate (the fund does not consolidate portfolio companies), which is why the same target can be in scope for one bidder and out of scope for another. Know which bidder you are.

If the group is in or near scope, the 2026 state of play: more than 50 jurisdictions had rules in force by 2025, with the charging order QDMTT first (the local jurisdiction taxes its own low-taxed profit), then IIR at the parent, then UTPR as backstop. For US-parented groups, the OECD side-by-side framework — agreed as administrative guidance on January 5, 2026 — excludes them from other countries' IIR and UTPR for fiscal years beginning on or after January 1, 2026, in exchange for the US keeping its own minimum-tax regime. Three diligence caveats keep that sentence from being a free pass: local QDMTTs still apply everywhere they exist, so a low-taxed sub still owes its domestic top-up; the exclusion needs local transposition, which lags — do not assume relief is live in any specific country without checking; and FY2024-2025 sit outside the relief entirely, so historic IIR/UTPR exposure for those years is still real money in an indemnity negotiation.

Two more deal-specific checks. The transitional CbCR safe harbour — extended through fiscal years beginning on or before December 31, 2027, with a 17% simplified ETR test in the final years — is what keeps most in-scope groups out of full GloBE math, and an acquisition can permanently break the target's eligibility under the once-out-always-out rule. And data: first GloBE Information Returns came due June 30, 2026 for calendar-year 2024 adopters, so an in-scope target with no GIR-grade data, no jurisdictional ETR map, and no safe-harbour analysis has a compliance program gap that you will inherit and fund. Write the seller's post-close data cooperation into the SPA; it is much harder to get after the wire clears.

Can the deal itself get taxed? Indirect transfer rules in India and China

Everything above concerns the target's taxes. Indirect transfer rules tax the transaction — the sale of shares in an offshore holding company can be taxable in the country where the underlying assets sit, even though neither buyer nor seller is resident there and the entity being sold is not either.

India codified this after the Vodafone litigation: under Explanation 5 to Section 9(1)(i), a transfer of foreign shares is taxable in India if the shares derive substantial value from Indian assets — the tests are Indian assets above INR 10 crore and representing 50%+ of the entity's global assets, with an exemption for transferors holding under 5% without management rights. The retrospective application that made Vodafone infamous was repealed in 2021; the rule itself applies prospectively and is enforced.

China's Bulletin 7 (SAT Announcement [2015] No. 7) is broader and, for buyers, sharper-edged: an offshore indirect transfer of Chinese taxable property can be re-characterized as a direct transfer and taxed at 10% on the gain if the arrangement lacks reasonable commercial purpose, tested on an eight-factor analysis with safe harbours for qualifying intra-group reorganizations and listed-share trades. The buyer's problem: the transferee is the statutory withholding agent. Fail to withhold on a taxable indirect transfer and the exposure — tax plus penalties — lands on you, not the departed seller. Enforcement has tightened through 2025, with authorities pairing Bulletin 7 reviews with transfer pricing audits.

The diligence method is structural: map every layer between the entity you are buying and the operating assets, and screen each layer against the indirect-transfer rules of every country where meaningful value sits — India and China are the canonical regimes, but the pattern exists elsewhere. Then check history: if the chain was reorganized in the past open years, an unreported historic Bulletin 7 or Explanation 5 event may already be sitting in the structure, and in a stock deal you inherit it. Where the current transaction is itself in scope, the mechanics belong in the SPA — who files, who withholds, who bears the tax — and the exposure belongs in the price, not in a hope that nobody notices.

Do the holding companies have substance — and is anyone actually resident where they claim?

Substance is the load-bearing wall under three other workstreams at once: treaty withholding relief (the Danish cases test), Pillar Two ETR math, and plain tax residency. In diligence it collapses into one question per holding entity: if a tax authority looked at this company, would they find a business or a mailbox?

The tests to run. Beneficial ownership and PPT on every entity in the dividend, interest, and royalty paths — an intermediate holdco with no employees, no office, and board minutes that rubber-stamp decisions made elsewhere will not hold its treaty rate. Residency and POEM: a company incorporated in one country but actually managed from another can be resident where the managers sit; post-MLI, dual-residence cases are resolved by competent-authority agreement rather than an automatic place-of-effective-management tie-breaker, which means a dual-resident entity can be stuck with no treaty relief at all until two governments agree — a genuinely bad place to discover mid-integration. Offshore substance regimes: Cayman and BVI entities carrying on relevant activities (holding-company business included, at a reduced standard) have filing and substance obligations with real penalties — pull the economic substance notifications and returns alongside the certificates of good standing. EU holdcos: Luxembourg and Irish structures built before ATAD need retesting against the 30%-of-EBITDA interest limitation and the anti-hybrid rules — an intra-group financing structure that worked in 2019 may be quietly non-deductible in 2026.

The red flags are consistent: directors who are all resident somewhere other than the holdco's jurisdiction, no local expenditure, management fees flowing to a zero-tax entity with one part-time employee, and minutes showing decisions "noted" rather than made. Each one converts a claimed tax rate somewhere in the structure into a contested one — and contested rates are exactly what the next section prices.

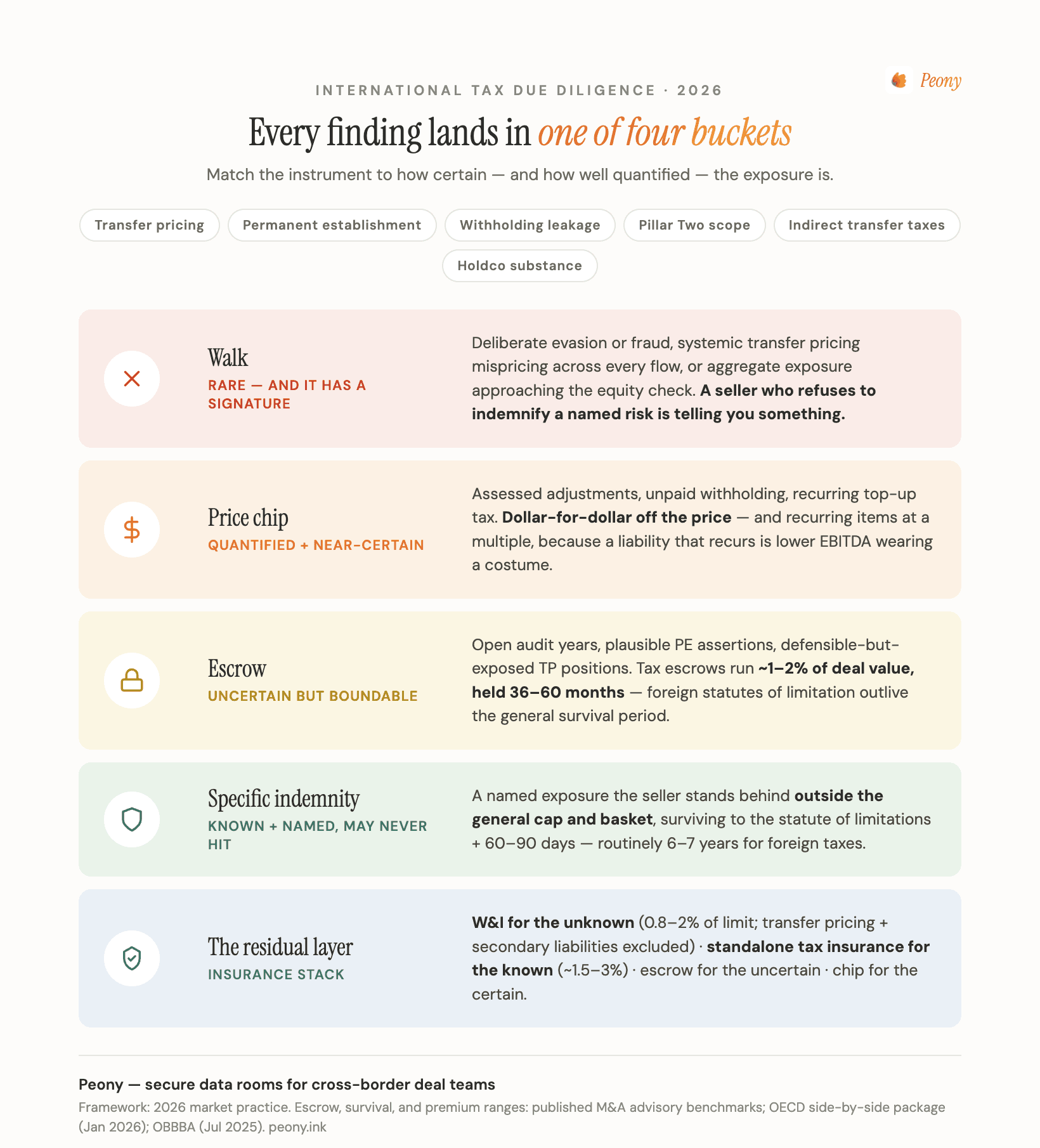

How do you turn findings into deal protection? Walk, chip, escrow, or indemnify

This is the section that separates international tax DD from an academic risk memo. Every finding must land in an instrument, and the instrument follows from two properties: how certain the exposure is, and how well quantified.

Price chip — quantified and near-certain. An assessed adjustment, an unpaid withholding liability, a top-up tax the group will owe every year it owns the structure. These come off the price dollar-for-dollar (recurring items at a multiple, because a liability that recurs is not a one-time finding — it is lower EBITDA wearing a costume). Buyers do not pay the LOI price; they pay the price that survives diligence.

Escrow or holdback — uncertain but boundable. Open audit years, a plausible-but-unassessed PE, a transfer pricing position that is defensible but exposed. General M&A escrows run 10-20% of price for 12-24 months; tax runs longer — a separate tax escrow of roughly 1-2% of deal value held 36-60 months is common market practice, because foreign statutes of limitation outlive the general survival period. Sizing above the midpoint estimate (we have seen escrows set at 130%+ of the assessed exposure) buys cushion for interest, penalties, and defense costs.

Specific indemnity — known and named. The workhorse for cross-border findings: a named exposure (the German PE question, the India royalty withholding, the pre-2026 Pillar Two years) that the seller stands behind outside the general indemnity cap and basket, surviving until the relevant statute of limitations plus 60-90 days — which for foreign taxes routinely means 6-7 years. A seller who refuses to indemnify a documented, named risk is telling you something about the risk.

Insurance — the residual layer. W&I insurance covers unknown breaches at premiums around 0.8-2% of the limit — but read the tax exclusions before you rely on it: transfer pricing, secondary tax liabilities, and anything known are standard carve-outs. The plug for known positions is standalone tax liability insurance — one identified exposure, one premium, transactional tax coverage typically pricing around 1.5-3% — a market growing fast enough (Euclid Transactional logged 1,917 submissions in 2025, up 25% year over year) that positions once considered uninsurable, including transfer pricing and withholding, now regularly get covered. The mid-market stack that works: W&I for the unknown, specific indemnity or tax insurance for the known, escrow for the uncertain, chip for the certain.

Structure — the instrument people forget. Stock versus asset (a stock deal inherits every historic exposure; an asset deal in the right jurisdictions leaves them behind, at the cost of transfer taxes and consents), a Section 338(g) election on a foreign target (a US-side step-up that changes the NCTI math post-OBBBA — model it, do not assume it), and pre-closing reorganizations to fix withholding paths or extract risky entities — executed between signing and closing with a step plan stapled to the SPA, so the seller bears the steps' tax cost and the buyer is not restructuring someone else's company on spec.

And walking? Rare, and it has a signature: deliberate evasion (indemnities assume honest sellers), aggregate exposure approaching the equity check, or structural problems no instrument reaches. Sellers preparing for exit can defuse most of this before a buyer ever sees it — that is a sell-side due diligence exercise, and cross-border tax is consistently the workstream where seller prep pays for itself.

What does international tax due diligence cost, and how long does it take?

Using advisory benchmarks rather than published rate cards (there are none): tax due diligence on $100-300M deals commonly runs $50K-$150K, and $150K-$400K on larger mid-market deals — with a six-country footprint pushing each band's top, because every jurisdiction adds local returns, withholding review, PE testing, and open-audit analysis, often through local offices billing partner time at $400-800 per hour. Cross-border timelines run 6-12 weeks against 3-6 domestic. These bands carry the cross-border premium; domestic-only tax DD scopes run at half or less. For where the tax workstream sits inside the whole diligence budget, our due diligence cost breakdown covers the full stack.

Two decisions control the spend. Tiering: full-scope review on the two or three jurisdictions holding most of the value and the riskiest flows; confirmatory-only elsewhere. A six-country target rarely needs six full workstreams — it needs two deep ones and four screens. Advisor mix: Big 4 breadth wins when you need simultaneous local presence in five countries; a boutique international tax firm wins on structuring depth and speed when the exposure concentrates in one or two; mid-market buyers increasingly run both — Big 4 for coverage, boutique for the SPA's tax clauses.

The hidden third lever is document logistics. Cross-border DD burns weeks when every local team requests returns country by country over email. The fix is unglamorous: stage everything before the clock starts.

The international tax DD request list — and how to stage it

The nine buckets that cover the cross-border layer (the full document checklist covers the domestic pillars):

- Entity chart with tax attributes — every entity including dormant ones, with tax residency, ownership percentages, and functional currency.

- Returns and assessments per jurisdiction — 3-6 years, matched to each country's statute of limitations, not a uniform three.

- Controversy file — every open audit, ruling, APA, and MAP proceeding, live or threatened.

- The transfer pricing stack — master file, local files, CbCR if filed, benchmarking studies, signed intercompany agreements, true-up calculations.

- Intercompany flow matrix — nature, amount, counterparties, and withholding actually collected on every cross-border flow.

- People map — headcount and contractors by country, contract-approval matrix, remote-work policies (the PE inputs).

- Pillar Two file — jurisdictional ETR map, safe-harbour analysis, GIR preparation status, for any group near EUR 750M.

- Holdco substance evidence — board minutes, director residency, local expenditure, economic substance filings.

- Cash and repatriation — dividend history, withholding certificates, trapped-cash schedule by country.

How you stage this matters more in cross-border DD than anywhere else, because the reviewing population is bigger and more fragmented: your fund team, Big 4 teams in multiple countries, local counsel per jurisdiction, and eventually the W&I underwriter — each of whom should see a different slice. This is the workflow Peony was built for, and it is why tax teams among our 5,900+ customers structure cross-border rooms as per-jurisdiction folders with per-advisor permissions: German counsel sees the German file, the underwriter sees the exposure schedule and nothing else, and every access is logged. Page-level analytics tell you which bidder's tax team actually read the local files (a bidder who never opened the TP folder has not priced the TP risk — expect it back as a late chip attempt), and AI Q&A over the room lets a reviewer ask "which entities paid withholding on royalties in 2024?" instead of paging through nine folders. Our data room folder structure guide has the full layout.

How Peony supports international tax due diligence

Peony is the data room, not the tax advisor — the exposure judgments above belong to your Big 4 or boutique team. What Peony contributes is the layer that makes a six-country review run like a two-country one: AI auto-indexing that organizes an uploaded document set into diligence-ready folders in minutes, granular per-folder and per-user permissions for jurisdiction-sliced access, dynamic watermarking and NDA gates for the documents that leave a paper trail (tax returns are among the most sensitive files in any room), a full audit trail your lawyers and the W&I underwriter will both ask for, and page-level analytics on 5,900+ customers' deals that show who engaged with what — before the negotiation makes it matter. Plans start free and scale at $30-$52 per admin per month, which for a $150K tax workstream is a rounding error that saves the expensive people weeks.

Bottom line

International tax due diligence is not a longer version of domestic tax DD — it is a different exercise with a different output. Domestic DD validates the returns. Cross-border DD prices the structure: what the intercompany flows would cost under audit, what the unregistered presence would cost if asserted, what the cash loses on the way home, whether the minimum tax reaches the group, whether the deal itself is taxable somewhere unexpected, and whether the holdcos are real. Run it through the four buckets — walk, chip, escrow, indemnify — with the 2026 baseline (side-by-side, NCTI at 12.6%, Brazil's 10% dividend withholding, the remote-work PE test) rather than the 2023 one, tier the jurisdictions instead of boiling six oceans, and stage the data room before the clock starts. The buyers who get hurt by cross-border tax are almost never the ones who found the exposure and priced it — they are the ones who found it and let it slip into the general reps, unpriced.

Frequently Asked Questions

We found a known cross-border tax exposure in diligence. Tax indemnity, escrow, or purchase price reduction — which should I push for?

Match the instrument to how certain and how quantified the exposure is. A quantified, near-certain liability (an assessed transfer pricing adjustment, an unpaid withholding bill) belongs in the purchase price as a dollar-for-dollar reduction — you should not escrow what you know you will pay. An uncertain but boundable exposure (open audit years, a plausible PE assertion) belongs in an escrow or holdback sized above the midpoint estimate, typically held 36-60 months for tax because foreign statutes of limitation run long. A known, named risk that may never crystallize (a defensible but undocumented intercompany flow) belongs in a specific indemnity that sits outside the general indemnity cap and basket, surviving until the relevant statute of limitations plus 60-90 days. Sellers push escrow over chip because they get the money back if nothing happens; buyers should concede that only where the exposure is genuinely contingent.

Which cross-border tax exposures are actual deal-breakers, and which can I cover with an indemnity?

Most cross-border tax findings are priceable, not fatal. Indemnifiable: historic withholding under-collection, thin transfer pricing documentation with defensible economics, an unregistered permanent establishment with modest attributable profit, open audit years. Deal-reshapers (fixable with structure, not just paper): indirect transfer exposure in India or China sitting mid-chain, holding companies that flunk beneficial ownership, trapped cash behind high withholding walls — these push you toward pre-closing reorganizations or carve-outs. True walk-away territory is rare and has a signature: deliberate evasion or fraud (indemnities do not cover sellers who lied about facts they knew), systemic transfer pricing mispricing across every flow where the aggregate exposure approaches the equity check, or an exposure the seller refuses to stand behind at any cap. If the seller will not indemnify a named, documented risk, treat that refusal as information.

Will reps and warranties insurance cover the transfer pricing exposure we already know about?

No — on two independent grounds. First, R&W insurance covers unknown breaches; anything disclosed in diligence or listed in the disclosure schedules is excluded as a known risk. Second, even for unknown matters, standard W&I policies carry standing tax exclusions, and transfer pricing is the most common one, alongside secondary tax liabilities and the availability of tax attributes like NOLs. The plug for a known, named exposure is either a specific seller indemnity or a standalone tax liability insurance policy, which underwrites one identified position for a single premium — transactional tax coverage typically prices around 1.5-3% of the covered amount, and the market has grown fast enough that specific transfer pricing and withholding positions are now regularly insurable. In practice mid-market buyers stack all three: W&I for the unknown, specific indemnity or tax insurance for the known, escrow for the uncertain.

GILTI vs Pillar Two: which one actually hits a US-parented target first in 2026?

For most US-parented mid-market groups, the US regime bites first — and since the One Big Beautiful Bill Act, it bites harder. GILTI was renamed Net CFC Tested Income (NCTI) for tax years beginning after December 31, 2025: the effective rate rose from 10.5% to 12.6%, the 10% deemed return on tangible assets (QBAI) was eliminated so the entire tested income base is exposed, and 90% of foreign taxes are now creditable. The practical crossover: a foreign effective rate of roughly 14% now zeroes out residual US tax. Pillar Two, by contrast, only applies at all if the group clears EUR 750M consolidated revenue in 2 of the prior 4 years — most $75-400M EV targets are out of scope on their own. And under the OECD side-by-side framework in effect for fiscal years from January 1, 2026, US-parented groups are excluded from other countries' IIR and UTPR charges — but local QDMTTs still apply in each jurisdiction that has one, so a low-taxed Irish or Swiss sub can still owe a domestic top-up.

The target group is under EUR 750M revenue. Is it really out of Pillar Two scope, and can our acquisition pull it in?

On its own, yes: the GloBE rules only capture groups with EUR 750M+ consolidated revenue in at least 2 of the 4 preceding fiscal years, so a standalone $150M EV target is comfortably outside. The acquisition can change that. If the buyer consolidates the target — a strategic acquirer, or a bolt-on into a platform company that prepares consolidated financials — the merger rule in Article 6.1 of the Model Rules aggregates the separately reported revenues of both groups for each of the prior four years, so a target that was never in scope can walk into a group that is, effective from the acquisition date. A fund-level acquisition through a typical non-consolidating private equity structure generally does not combine revenues, because the fund does not consolidate portfolio companies — but confirm that with your structure, because investment-entity accounting is exactly the kind of detail that varies. Also check the safe harbour: combining groups can break transitional CbCR safe harbour eligibility, forcing full GloBE calculations earlier than planned.

The target's transfer pricing documentation looks thin. How exposed are we really?

Size it in three steps rather than treating thin documentation as a binary red flag. First, exposure base: pull the intercompany flow matrix — every management fee, royalty, intercompany loan, and goods flow by amount and counterparty — because the adjustment risk is a percentage of those flows, not of revenue. Second, penalty regime by jurisdiction: in the US, a net Section 482 adjustment can carry a 20% or 40% penalty, avoidable only with contemporaneous documentation produced within 30 days of request; Germany adds a 5-10% surcharge on adjustments plus late-production fines and now allows only 30 days to produce documentation; India charges 2% of the transaction value for missing documentation plus up to 200% of the tax on the adjustment (Section 270A: 50% for under-reporting, 200% for misreporting). Third, open years: multiply across the statute of limitations in each country, commonly 4-7 years. Thin documentation with defensible economics is usually a specific-indemnity item plus a post-close remediation budget; thin documentation hiding non-arm's-length economics is a price chip.

Is $30M a year of intercompany flows a transfer pricing audit magnet?

It is enough to matter, and the composition matters more than the total. $30M of arm's-length product sales between a manufacturer and its distribution subs, benchmarked and documented, is routine. The same $30M concentrated in management fees, IP royalties, or intercompany loan interest flowing from high-tax operating countries to a low-tax entity is exactly the fact pattern tax authorities screen for — Germany, India, and Brazil all run data-driven audit selection on precisely those flows. The diligence questions that predict audit outcomes: do intercompany agreements exist and predate the flows, does a benchmarking study support each pricing policy, do year-end true-ups have a contractual basis that both jurisdictions accept, and has any local entity reported persistent losses while the group is profitable. If the target books material year-end true-up adjustments as a margin plug, price in remediation regardless of audit history.

The target has remote employees and contractors in Germany and Singapore. Is that creating permanent establishment risk?

Possibly — and 2026 is the first year with a real framework to test it. The OECD's November 2025 update to the Model Tax Convention added a two-part home-office test: an employee working from home under 50% of their working time over any 12-month period generally does not create a fixed place of business, while above 50% the arrangement must have a genuine commercial reason — and the commentary explicitly says employee preference, talent retention, and office-cost savings do not qualify. The sharper risk is usually the dependent-agent version: a country manager or salesperson who habitually negotiates and effectively concludes contracts can create a PE regardless of where they sit. In diligence, map headcount and contractors by country against the entity chart, flag every country with revenue-generating people but no registered entity, and check contract-approval authority. Quantify a finding as attributable profits times the local corporate rate plus interest, penalties, and the payroll and VAT registrations that usually ride along. Only about a quarter of jurisdictions have issued specific remote-work PE guidance, so uncertainty itself is part of the exposure — which is what escrows are for.

How much withholding tax will we leak repatriating cash from India and Brazil to the US parent?

Model it hop by hop, because the answer is a path, not a rate. India withholds 20% (plus surcharge and cess) on dividends to non-residents; the US-India treaty can reduce that to 15% for a corporate parent holding 10%+, subject to beneficial ownership and the principal purpose test. Brazil is the 2026 trap: Law 15,270/2025 introduced a 10% withholding tax on dividends to non-residents from January 1, 2026 — dividends were previously exempt — and there is no US-Brazil income tax treaty to reduce it, though interest on net equity (JCP) remains a deductible alternative channel, with its withholding rate raised to 17.5% in the same 2026 reform. On $30M of annual distributions split across those two, unplanned leakage can run seven figures a year. In diligence, build the dividend path from each operating company to the fund, apply statutory and treaty rates at each hop, test whether intermediate holdcos actually qualify for treaty relief (see the Danish beneficial ownership cases), and discount trapped cash in the equity bridge rather than assuming it travels at face value.

What does international tax due diligence cost for a $150M deal with subsidiaries in six countries?

Plan around $100K-$250K for the tax workstream on that profile, using advisory benchmarks rather than rate cards: tax due diligence on $100-300M deals commonly lands at $50K-$150K, and a six-country footprint with transfer pricing review pushes toward and past the top of that band because each jurisdiction adds its own local-tax, withholding, PE, and open-audit review, often with local-office involvement billing at partner rates of $400-800 per hour. Timeline stretches the same way: 3-6 weeks for a domestic mid-market target becomes 6-12 weeks cross-border. Two ways to keep both numbers down: tier the jurisdictions (full scope on the two or three countries holding most of the value and the riskiest flows, confirmatory-only elsewhere) and stage the data room per jurisdiction before the clock starts so local teams pull returns, assessments, and intercompany agreements without a three-week document chase.

What should I request in the data room for international tax due diligence?

Nine buckets cover the cross-border layer: (1) a legal entity chart with tax residency and ownership percentage for every entity, including dormant ones; (2) three to six years of income tax returns and assessments per jurisdiction, matching each country's statute of limitations; (3) every open audit, ruling request, APA, and MAP proceeding; (4) the transfer pricing stack — master file, local files, CbCR if filed, benchmarking studies, and signed intercompany agreements; (5) an intercompany flow matrix: nature, amount, counterparties, and withholding actually collected on each flow; (6) headcount and contractors by country against the entity chart, plus the contract-approval matrix, for PE testing; (7) a jurisdictional effective-tax-rate map and any Pillar Two or safe-harbour analysis if the group is near EUR 750M; (8) board minutes, director residency, and substance evidence for every holding company; and (9) dividend history plus a trapped-cash schedule by country. Stage them as per-jurisdiction folders with per-advisor permissions so local counsel in each country sees only their file.

We have 10 days of exclusivity left. Which international tax issues must be resolved before signing, and which can close later?

Resolve before signing anything that changes the structure or the price, because those cannot be papered afterward: whether an indirect transfer rule (India's Explanation 5, China's Bulletin 7) taxes the transaction itself and who withholds; whether the acquisition pulls the combined group into Pillar Two scope or breaks safe-harbour eligibility; whether trapped cash and withholding leakage change the equity bridge; and whether any exposure is large enough to demand a price chip or a pre-closing reorganization. Those are days of work each, not weeks, if the data room already holds the entity chart, flow matrix, and returns. Leave for the sign-to-close window or post-close, covered by indemnities: full transfer pricing benchmarking rebuilds, country-by-country PE deep dives beyond the flagged jurisdictions, and remediation planning. The discipline that makes a 10-day window survivable is converting every unresolved item into a named exposure with an instrument attached — chip, escrow, or specific indemnity — rather than letting it slip into the general reps unpriced.

Related Resources

- Tax Due Diligence Checklist — the full 8-pillar framework and document checklist this guide layers onto.

- Due Diligence Cost Breakdown — where the tax workstream sits in the full diligence budget.

- Sell-Side Due Diligence — defusing cross-border tax findings before buyers price them.

- M&A Data Room Guide — running the deal room the tax workstream lives in.

- Data Room Folder Structure Guide — the per-jurisdiction layout that keeps six countries reviewable.

- Best AI Data Rooms for M&A Due Diligence — AI Q&A and auto-indexing across a cross-border document set.

- What Is Due Diligence? — the full landscape of diligence workstreams for first-time deal teams.

You might also like

Apr 1, 2026

Tax Due Diligence Checklist (8 Pillars M&A Tax Advisors Miss) in 2026

Jul 8, 2026

State of M&A Data Rooms 2026: $296/mo vs $68K/yr (334 Deals)

Jun 16, 2026

Best Intralinks Alternatives & Competitors for M&A Due Diligence in 2026