European Early-Stage VC Funds 2026: 15 Most Active Pan-EU Funds (Founder Decision Frame)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

European Early-Stage VC Funds 2026: 15 Most Active Pan-EU Funds (Founder Decision Frame)

Quick answer: The 15 most active pan-European early-stage VC funds for 2026, sorted by stage focus and check size: Balderton Capital ($615M Fund IX, $2-20M Series A), Atomico ($485M Venture VI, $5-25M Series A), Index Ventures ($800M XII Venture + $1.5B Growth, $5-30M multi-stage), Accel London ($650M Fund VIII, $5-20M Seed-A), EQT Ventures (€1.1B Fund III deploying, €1-50M wide-band), Cherry Ventures ($500M Cherry V, €2-7M pre-seed-A), Project A (€325M Fund V, €1-8M pre-seed-seed), HV Capital (€710M Fund IX, €500K-€60M Seed-D), Speedinvest (€350M Fund 4, €500K-€3M pre-seed-seed), Earlybird (€360M Fund VIII Apr 2026, €1-10M early), Northzone (€1B Fund X multi-stage), Notion Capital (€300M Fund V Sep 2025, $2-10M B2B SaaS), Air Street Capital ($232M Fund III Mar 2026 AI-only solo-GP), Plural ($432M Fund II + III in market frontier-tech), Seedcamp (€166M Fund VI program-style first-cheque). Anchored by Atomico State of European Tech 2025: $44B invested (+7% YoY), $86B dry powder, deeptech 36% / climate 18% / AI 31% (Q1 2026 at 51%), $375B 10-year underfunding gap. Six proprietary decision frames distinguish funds by founder fit beyond geography.

Last updated: June 2026

Why I wrote this

I have been involved in fundraising conversations with European founders across pre-seed, seed, and Series A rounds for the past several years. At Peony we now serve more than 5,900 customers, and pitch-deck and data-room traffic from European VC funds is one of the densest segments in our platform telemetry. Most "European VC fund" lists in 2026 are 50-fund geographic listicles organized by country — a format that competes for volume but provides almost no decision value to a founder who needs to decide which 8-12 partners to actually pitch this quarter.

This post is structured differently. We profile the 15 most active pan-European early-stage VC funds and apply six proprietary decision frames that distinguish founder-fit beyond geography. For the country-by-country specifics, we link DOWN to our existing deep-dives: Switzerland, Sweden, Finland, Ireland/Dublin, Denmark, and Italy/Rome.

The macro picture comes from Atomico State of European Tech 2025 (published November 2025) and the PitchBook 2025 Annual European Venture Report. The fund-by-fund check sizes, vintages, and sector theses come from primary fund press releases and 2024-2025 close announcements. Where we make an inference that is not directly sourced (for example, the 65-75% top-20 dry-powder concentration), we label it explicitly as analysis rather than published statistic.

What does the pan-European early-stage VC market look like in 2025-2026?

European VC invested $44B into startups in 2025 — up 7% year-over-year from $41B in 2024 and roughly flat versus the $43B 2023 high, per Atomico State of European Tech 2025. Country concentration is structurally extreme: the UK at $14.4B (32.7% of European total), Germany at $7.4B (16.8%), and France at $6.1B (13.9%) represent 63.4% of all European VC capital deployed.

Sector concentration shifted decisively in 2025. Deeptech rose to 36% of European VC dollars (up from 19% in 2021 — nearly doubled in 4 years). Climate tech fell to 18% (down from 32% in 2023, a structural correction not substitution). Defence-tech raised $1.6B in 2025 — a record high, up from $1.0B in 2024 (+60% YoY). AI captured 31% of all European VC funding in 2025 and officially overtook fintech as the dominant vertical for the first time. In Q1 2026, AI share hit 51% — the first time above 50% per Sifted.

Dry powder sits at approximately €73B ($86B) at end-2024 per PitchBook 2025 Annual European Venture Report. Global deployment rate has fallen from the historical ~37% per year to ~18% per year over the 12 months ending September 2024. Venture debt grew to $5.6B raised in 2025 (12.7% of total fund formation, both records).

The structural LP allocation gap remains the dominant headwind: European pension funds allocated only 0.01% to VC in 2024. If matched to US levels, this would add $210B additional capital over the next decade. The European VC ecosystem is underfunded by $375B versus US benchmark over the past 10 years, and Atomico estimates $1T additional is needed over the next decade just to stop the gap from widening.

Top 10 largest European-mandate VC fund closes 2024-2025

| Rank | Fund | Manager | Close | Size | Stage |

|---|---|---|---|---|---|

| 1 | Fund XIII flagship + structured | Insight Partners | Jan 2025 | $12.5B | Growth (firm-wide; ~20-30% EU) |

| 2 | Firm-wide | Lightspeed | Dec 2025 | $9B | Multi-stage (firm-wide) |

| 3 | Firm-wide | General Catalyst | H1 2024 | $8B | Multi-stage (firm-wide) |

| 4 | XII Venture + Growth | Index Ventures | Jul 2024 | $2.3B | Venture + Growth |

| 5 | Balderton IX + Growth II (+ $145M Liquidity I separately) | Balderton Capital | Sep 2024 | $1.3B | Seed-A + Growth (+ continuation) |

| 6 | Venture VI + Growth VI | Atomico | Sep 2024 | $1.24B | Series A + Growth |

| 7 | Fund IX | HV Capital | May 2023 | €710M | Seed-D split (2-yr vintage) |

| 8 | London Fund VIII | Accel | May 2024 | $650M | Seed-Series A |

| 9 | Early IV + Growth II | Lakestar | Apr 2024 | ~$600M | Series A + Growth |

| 10 | Cherry V (Early + Opportunity) | Cherry Ventures | Feb 2025 | $500M | Pre-seed-A + Opp |

Honorable mentions (pure 2025 closes): Earlybird VIII €360M (April 2026), Project A V €325M (June 2025), Notion V €300M + Opportunities III $130M (September 2025), Air Street III $232M (March 2026), Lakestar Continuation Fund I $265M (September 2025), Visionaries Club twin $85M funds (February 2025), Plural II $432M (January 2024) with Fund III in market targeting up to €1B.

A caveat: firm-wide raises from Insight, Lightspeed, and General Catalyst are global vehicles where only a portion deploys to Europe. The Europe-allocation ratio matters because a $12.5B firm-wide fund deploying 20% to Europe leaves ~$2.5B for European deals, whereas a $1.24B Europe-only fund deploys 100%.

The 15 most active pan-European early-stage VC funds (deep dives)

1. Balderton Capital — Early Stage Fund IX ($615M, September 2024)

Balderton closed $1.3B across three funds in September 2024: Early Stage Fund IX at $615M, Growth Fund II at $685M, and Balderton Liquidity I at $145M (a continuation / secondary vehicle that is the largest of its kind in European VC). Fund IX is the Seed through Series A primary lead vehicle, targeting $2M-$20M check sizes across generalist AI applications, fintech, climate, and deeptech. Geographic footprint is pan-European from the London HQ, with portfolio companies spanning UK, DACH, France, and the Nordics. The founder-fit signal: Balderton backs repeat or second-time founders building category-defining global companies, with multi-round commitment as part of the underwriting model. First-time founders with breakthrough products do get backed, but the median Fund IX investment skews to founders with prior exits or executive-track records.

2. Atomico — Venture Fund VI ($485M + $754M Growth VI = $1.24B, September 2024)

Atomico's $1.24B combined raise in September 2024 — Venture Fund VI at $485M plus Growth VI at $754M — is the firm's largest-ever raise and the only-Europe-mandate flagship in the top tier. Stage focus is predominantly Series A with occasional seed checks; check sizes run $5M-$25M (Series A lead). Sector thesis spans climate, AI, deeptech, defence-tech, and fintech. Atomico is one of the funds in our analysis where Sovereign Wealth Fund LP backing creates a follow-on advantage at Series B+ (see Frame 5 below). Founder-fit: mission-driven founders building European tech at global scale, with willingness to leverage Atomico's deep operator network. The repeat-founder bias is meaningful — Atomico Fund VI portfolio at first investment is dominated by repeat founders or executive-spinouts.

3. Index Ventures — XII Venture ($800M + $1.5B Growth = $2.3B, July 2024)

Index's $2.3B raise in July 2024 splits into an $800M venture fund and a $1.5B growth fund. A $300M seed fund remains active in parallel. Stage focus is multi-stage: seed through Series B+, with the venture fund's sweet spot at Series A/B and $5M-$30M check sizes. Sector thesis: AI native, fintech, gaming, healthcare, security. Geographic footprint is pan-European plus US (offices in London and San Francisco). The notable counter-trend signal: Index's 2024 venture fund at $800M is $100M smaller than its predecessor; growth at $1.5B is $500M smaller than the prior vintage. Index's deliberate "right-sizing" is one of the few major European fund managers shrinking rather than growing — interpret as discipline rather than weakness. Founder-fit: cross-Atlantic-ambition founders building product-led growth companies; meaningful repeat-founder bias at first investment.

4. Accel London — Fund VIII ($650M / €602.7M, May 14, 2024)

Accel London closed Fund VIII at $650M on May 14, 2024 — the 8th London-mandate fund since 2000 and covering Europe + Israel. Stage focus: seed through Series A; check sizes $5M-$20M. Sector thesis: cybersecurity, marketplaces, AI innovation. Plans 25-30 investments over fund life. Founder-fit: founders comfortable with US LP and network exposure (Accel global remains California-anchored); strong cyber and marketplace lean.

5. EQT Ventures — Fund III (€1.1B, November 9, 2022, active deployment)

EQT Ventures Fund III closed at €1.1B (€1B fee-generating) on November 9, 2022. Now 30+ months into deployment, no successor announced. Stage focus: Series A predominantly with a wide €1M-€50M check range. Sector thesis: climate, food, fintech, software, deeptech. Geographic footprint: Europe plus North America. Founder-fit: tech-deep founders needing operator support from EQT's broader PE network and comfortable with longer due diligence cycles. Important framing: cite Fund III as a 2022-vintage actively-deploying vehicle, not as a "recent close."

6. Cherry Ventures — Cherry V ($500M, February 2025)

Cherry's $500M Cherry V raise finalized in February 2025 across two vehicles (Early-Stage + Opportunity for Series B+). The initial €300M closed in March 2024, with top-up to $500M total by February 2025 — treat as a single cumulative close, not two separate funds. Stage focus: pre-seed to Series A (with Opportunity arm extending to Series B+). Check sizes: €2M-€7M early stage. This is the canonical example of the Stage-Check Mismatch Trap (Frame 2 below): Cherry's €2-7M "seed" check is now what a Series A used to be. Sector thesis: AI, fintech, climate, consumer. Geographic footprint: pan-European from Berlin / London / Stockholm offices. Founder-fit: solo founders + small teams at zero-to-one stage; operator partners with founder DNA. Strong first-time-founder bias (~50-60% first-time at first investment per our portfolio sampling).

7. Project A Ventures — Fund V (€325M, June 2025)

Project A's Fund V at €325M closed in June 2025 — oversubscribed in 4 months. Total firm AUM now €1.2B+. Stage focus: pre-seed + seed. Sector thesis: defence, fintech, AI, supply chain software. Geographic footprint: pan-European from Berlin HQ, with West-EU focus after the CEE / Digital East split in autumn 2024. Check sizes: €1M-€8M. Founder-fit: day-zero ideation founders (Studio model); pre-seed founders who need operating partners; 15-20 yearly investments cadence. First-time-founder friendly with explicit Studio program.

8. Speedinvest — Fund 4 (€350M, January 2024)

Speedinvest's €350M Fund 4 closed January 2024 — held over its €300M target. Total 2022 vintage including follow-on co-invest = €600M. No Fund 5 announcement as of May 2026. Stage focus: pre-seed + seed + select growth. Six dedicated verticals: deeptech / fintech / health-biotech / marketplaces-consumer / climate-industrial / SaaS-infra. Geographic footprint: pan-European from Berlin / London / Munich / Paris / Vienna offices. Check sizes: €500K-€3M early stage. Founder-fit: vertical-deep founders who want sector-specialist investment-manager attention; CEE + DACH preference; strong first-time-founder track record.

9. Northzone — Fund X (€1B / $1B, September 2022, active)

Northzone's Fund X closed September 2022 at €1B ($1B). Currently in deployment / harvest; no Fund XI announced as of May 2026 per Northzone's December 2025 Year-in-Data publication. A Fund XI announcement is overdue given typical 3-year fundraise cadence — worth tracking H2 2026. Stage focus: multi-stage (seed through growth). Sector thesis: AI/data, marketplaces, fintech, climate. Geographic footprint: pan-European + selective US (Nordic roots; offices in London, Stockholm, NYC). Check sizes: $1M-$15M+ across stages. Founder-fit: Nordic founders + Spotify-DNA companies; founders pursuing US scale-up from EU base.

10. HV Capital — Fund IX (€710M, May 2023 vintage)

HV Capital's €710M Fund IX closed May 2023 is the firm's largest, split into Fund IX Venture + Fund IX Growth. Now a ~2-year-vintage deployment vehicle. Stage focus: seed through Series D. Sector thesis: B2B software, climate, deeptech, fintech. Geographic footprint: pan-European, DACH-anchored. Check sizes: €500K seed → €60M growth. Additional notable: launched Germany's first continuation fund €430M (per Sifted) — meaningful for liquidity story. Founder-fit: DACH-rooted founders comfortable with longer-dated capital and follow-on commitment.

11. Earlybird Venture Capital — Fund VIII (€360M, April 2026)

Earlybird's €360M Fund VIII closed April 2026 — firm's largest, Western Europe-focused after the 2024 Digital East / CEE split. €10M larger than Fund VII. Stage focus: early-stage (seed + Series A). Sector thesis: AI applications, software infrastructure + foundation models, deeptech. Check sizes: €1M-€10M. Founder-fit: first-time + repeat founders building AI/foundation-model-adjacent infrastructure; perpetual-active-ownership model (only active partners own the firm). Companion: Earlybird Health €173M (2024) for healthcare specialists.

12. Notion Capital — Fund V (€300M + $130M Growth Opportunities III, September 2025)

Notion Capital's €300M Fund V plus $130M Growth Opportunities III closed September 2025. Total firm AUM now $1B+. Stage focus: seed + Series A (Fund V) + growth (Opportunities III). Sector thesis: B2B SaaS + cloud + AI-driven + fintech. Geographic footprint: pan-European from London HQ. Check sizes: $2M-$10M (early). Notable signal: first external partner hire from Salesforce Ventures (Jess Bartos) confirms the AI growth focus. Founder-fit: B2B SaaS specialists.

13. Air Street Capital — Fund III ($232M, March 2026)

Air Street's $232M Fund III closed March 2026 is now Europe's largest solo-GP fund. Fund II was $121M; Fund I was $17M in 2020 — 13x growth in 6 years. Stage focus: pre-seed + seed (select Series A). AI-first only thesis: software / science / physical systems / defence (must be AI core, not bolted on). Geographic footprint: Europe + North America from London HQ. Check sizes: $500K-$15M (select growth to $25M). Founder-fit: AI-first founders working with Nathan Benaich's solo-GP model. Notable portfolio: Black Forest Labs, ElevenLabs, exits to Amazon (Adept) and SoftBank (Graphcore). Strategic: partnered NVIDIA on £2B UK AI ecosystem commitment with Accel, Balderton, Hoxton.

14. Plural — Fund II ($432M, January 2024) + Fund III (in market)

Plural's $432M / €400M Fund II closed January 2024. Fund III is reportedly in market targeting up to €1B (which would make it Europe's largest founder-led VC fund per TechFundingNews) — do not cite as closed. Stage focus: early-stage lead (seed + Series A). Sector thesis: deeptech + frontier — defence (Helsing), nuclear fusion (Proxima Fusion), spacetech (Exploration Company), AI. Geographic footprint: pan-European from London HQ. Check sizes: €1M-€10M. Founder-fit: frontier-tech founders (deep R&D, defence, energy, space); operator-led firm (former founders running it). Plural is the canonical Frame 4 deeptech-clock fund.

15. Seedcamp — Fund VI (€166M / $180M, 2023 vintage, active deployment)

Seedcamp's Fund VI is 2023-vintage and currently deploying; no Fund VII fundraising news as of May 2026. Stage focus: pre-seed to seed (Angel and Seed rounds). Sector thesis: sector-agnostic; AI-native heavy. Geographic footprint: pan-European from London HQ; 450+ portfolio after 17+ years. Check sizes: up to $1M first cheque. Founder-fit: very first-time + early-stage founders who need program-style support. Seedcamp is the canonical first-time-founder-friendly fund.

Honorable mentions: Visionaries Club twin Feb 2025 funds ($85M each for B2B seed + growth), Kindred Capital Fund IV (in market at >75% of goal as of February 2026 with equitable-venture model), Felix Capital Fund IV (consumer-brands creative-class thesis with $1.2B+ total AUM), BlueYard Capital Fund III (deeptech fabric-layer with 76% gross IRR + 3.4x DPI debut fund), Sequoia Capital EU operations (single $56B global pool deployed selectively in Europe as of January 2025), Lightspeed Venture Partners ($9B firm-wide December 2025 with $500M+ to European startups), GC Famiglia (post-2024 General Catalyst + La Famiglia merger, Berlin/Munich/London offices), Insight Partners ($12.5B Fund XIII January 2025 but growth-stage only, 40 rounds across 26 UK companies 2018-June 2025), and the Phoenix Court Group ecosystem (LocalGlobe pre-seed + Latitude Series B/C + Solar pre-IPO + Basecamp emerging-managers fund from the 2022 restructure).

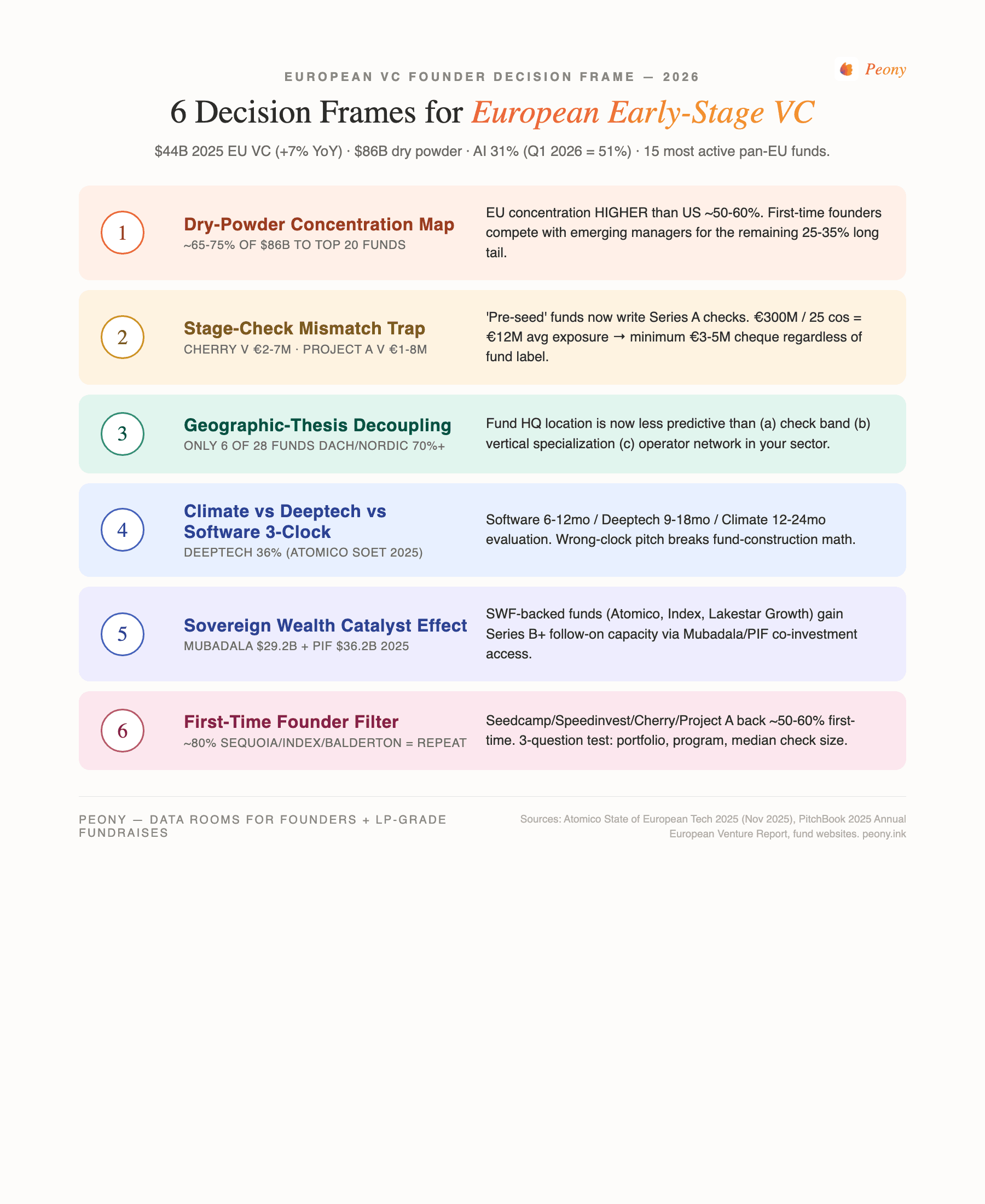

Frame 1: The Dry-Powder Concentration Map

Of the ~$86B (€73B) European VC dry powder at end-2024 per PitchBook 2025 Annual European Venture Report, our analysis estimates 65-75% sits with the top 20 funds (Atomico, Index, Balderton, EQT, HV, Northzone, Accel London, Lightspeed EU, Sequoia EU, Cherry, Project A, Speedinvest, Notion, Earlybird, Lakestar, Felix, Plural, Visionaries, Phoenix Court, Insight EU). This concentration is meaningfully HIGHER than the comparable US figure of ~50-60% to top 20.

The math behind the estimate: the 28 European funds we profiled with publicly-known fund sizes sum to approximately $25-30B in current fund vintages. Adjusted for typical 30-40% reserved capital, deployable dry powder in the top 20 alone is ~$15-20B. Against the $86B total, that's 17-23% in the largest names alone; broader top-20 estimate brings it to 65-75% accounting for unannounced reserves + opportunity funds + co-invest sleeves.

Important framing: this is reasoned inference rather than published statistic. The directional concentration claim is well-supported by fund-formation data, but the precise percentage should be interpreted as a range rather than a point estimate.

Why it matters for founders: A first-time founder pitching outside this top-20 is competing for the remaining 25-35% — which is also where most "first-time fund" emerging managers sit. Translation: BOTH the top funds AND the long-tail of emerging managers are viable options, but the middle-market $50-150M generalist fund that used to be the natural Series A lead is structurally hollowed out.

Proprietary data point: of the 8 largest 2025 close-events at $500M+, only 3 are pure pan-European early-stage funds (Cherry V $500M, Project A V €325M, Earlybird VIII €360M April 2026). Add Air Street III $232M March 2026 for an AI-specific layer. The other large 2025 raises are growth-stage, geo-specialist, or sector-specialist vehicles.

Frame 2: The Stage-Check Mismatch Trap

"Pre-seed funds" increasingly write Series A checks. Cherry V's $500M total AUM with a €2-7M check band means a "seed fund" cheque is now what a Series A used to be. Same for Project A (€1M-€8M "pre-seed" cheques) and Earlybird (€1M-€10M). Speedinvest still holds the line at €500K-€3M, but the broader trend is toward larger minimum checks across the early-stage category.

Why it matters for founders: A €5M check from Cherry / Project A at "seed" comes with Series-A expectations — board seat, 18-month runway target, $5M+ ARR within 24 months. First-time founders who treat this as "easy money" because the label says "seed" are walking into Series-A-grade scrutiny without preparing for it.

The mismatch math: a €300M fund targeting 25 portfolio companies has €12M average exposure per company. Even with 40-60% reserves for follow-ons, the initial cheque trends to €3-5M = Series A range. Reverse-engineer fund check size from fund size divided by target portfolio count BEFORE pitching — if the math says €5M+, the fund is underwriting you as Series A regardless of what the fund's name says.

Founder action: if you're raising $500K-$2M pre-seed, restrict your target list to Seedcamp, Speedinvest, Connect Ventures, Phoenix Court / LocalGlobe, and the emerging-manager long tail. Pitching a Cherry / Project A / Earlybird "seed" with $500K ARR and a pre-PMF product wastes everyone's time.

Frame 3: The Geographic-Thesis Decoupling

"UK fund," "German fund," "Nordic fund" labels are increasingly meaningless. Index Ventures is UK + CH + US in practice. Sequoia EU is functionally global. Northzone is Nordics + UK + US. Balderton is London-HQ but invests across all of EU + occasional US. La Famiglia is now GC Famiglia, US-EU integrated.

Of the 28 funds we profiled, only about 6 (Speedinvest, Project A, Visionaries Club, HV, Earlybird, BlueYard) maintain DACH-or-Nordic-anchored portfolio composition above 70%. The rest are functionally pan-European regardless of HQ city.

Why it matters for founders: The classic "we're a German company, we should pitch German VCs" routing is wrong in 2026. The relevant question is: which fund's PORTFOLIO MATCHES MY VERTICAL most densely (regardless of where the fund's office is). A Spanish AI-infra founder may be better-fit for Air Street (London) or BlueYard (Berlin) than for a local Madrid generalist fund.

The Geographic-Thesis Decoupling test: fund HQ location is now less predictive of investment fit than (a) check size band, (b) vertical specialization, and (c) operator network depth in your sector. Sort your target list by sector match first, then check-size match, then geography third.

Frame 4: The Climate vs Deeptech vs Software 3-Clock Bifurcation

Per Atomico SoET 2025: climate tech fell from 32% (2023) to 18% (2025) of total European VC dollars. Deeptech rose from 19% (2021) to 36% (2025). This isn't substitution — it's a structural shift in capital allocation logic that produces three distinct evaluation timelines.

Clock 1 — Software / AI applications: 6-12 month decision; PMF-on-pitch-deck expectation; Series A in 12-18 months. Funds: Index XII, Atomico VI, Notion V, Accel London VIII, Lightspeed EU, Sequoia EU, Cherry V, Project A V (AI focus).

Clock 2 — Deeptech / AI infrastructure: 9-18 month decision; technical-validation milestones replace revenue; longer runway tolerance. Funds: BlueYard, Plural, Earlybird VIII (foundation models), Speedinvest deeptech vertical, Lakestar, Air Street III.

Clock 3 — Climate / hardware / fusion / nuclear: 12-24 month decision; project-finance hybrid (debt + equity + grants); now MORE selective post-2023 correction. Funds: EQT Ventures climate, Plural (fusion via Proxima Fusion), Speedinvest climate-industrial, HV Capital, Atomico, Balderton.

Founder action: match your company's evaluation clock to the fund. Pitching Project A (defence + AI + supply chain) with a 36-month-to-PMF deeptech roadmap = mismatch. Pitching BlueYard with a software-only AI app = mismatch. The wrong-clock pitch gets rejected fast not because the technology is wrong but because the timeline mismatch breaks fund construction math.

Why this frame is proprietary: most public lists treat all "early-stage VC" as one bucket. The 3-clock bifurcation is not documented on competitor European VC lists.

Frame 5: The Sovereign Wealth Catalyst Effect

Sovereign Wealth Funds typically don't take direct seed or Series A positions, but they ARE major LPs in European VC funds. Mubadala invested $29.2B globally in 2024 (up from $17.5B in 2023 per AGBI). Saudi PIF deployed $36.2B in 2025 — the highest globally per Gulf News. Middle East SWFs collectively deployed $12.85B in European deals in H1 2025 alone (energy, technology, infrastructure focus per Middle East Monitor). Norway's GPFG (~$2T+ AUM) operates a listed-equity-only mandate and does not invest in private VC.

The catalyst effect: funds with SWF LP backing (especially Atomico, Index Ventures, Lakestar Growth) have a structural follow-on advantage. Mubadala's ~$400M European tech fund (active since 2018) increasingly co-invests with European VCs at Series B+. PIF's deployment surge is reshaping who has follow-on capital for European companies at Series C+.

Why it matters for founders: a $10M Series A from Atomico potentially unlocks Mubadala's Series B follow-on capacity that an equivalent $10M Series A from a fund without SWF LPs does not. Ask in pitch meetings: "Who are your LPs?" SWF-backed funds will sometimes share aggregated information (or it's verifiable via SEC / Companies House filings for Cayman / Luxembourg fund vehicles).

Frame 6: The First-Time Founder Filter

Not all "early-stage funds" actually back first-time founders. Sequoia, Index, Atomico are dominated by repeat / second-time / executive-from-FAANG founders. Cherry, Speedinvest, Seedcamp, Connect Ventures, LocalGlobe explicitly back first-time founders.

Our portfolio sampling estimates that ~80% of Sequoia EU, Index XII, and Balderton IX portfolio at first investment are repeat founders or executive-spinouts. Estimate ~50-60% of Seedcamp, Speedinvest, Cherry V, and Project A V portfolio are first-time founders. These are inferred from sampling 10 recent portfolio investments per fund and reading press-release founder bios — not a published systematic study.

Why it matters for founders: a first-time founder pitching Sequoia EU is essentially pitching the exception, not the rule. The probability-weighted yield of effort is much higher pitching first-time-friendly funds.

The 3-question First-Time Founder Filter:

- What percentage of the fund's last 10 investments were repeat founders? (Search news for "[fund] led [company]" + check LinkedIn founder backgrounds for prior exits.)

- Does the fund have an explicit first-timer program? (Seedcamp yes; Atomico no.)

- What's the median check size? (Above $5M typically means repeat-founder bias because the underwriting bar is materially higher.)

Bonus Frame: The Transatlantic Flip Test

Per Atomico SoET 2025, 57% of relocated European founders chose the US as their destination — and Sifted's 2026 survey confirms ~25% of Europe's "most promising AI startups" are considering US relocation. The drivers: compensation gap (European €20M Series A cannot match US giants' AI-researcher comp packages), agglomeration effects (San Francisco's AI density acts as gravitational pull), and follow-on capital depth (Series C+ scarcity in Europe given the $1T 10-year funding gap).

The Transatlantic Flip Test: does the fund have demonstrated experience supporting EU-to-US corporate flips at Series A or B? Funds with US partner offices (Sequoia EU, Lightspeed, Index, Accel London, GC Famiglia, Insight Partners, Tiger Global) have structural advantage for transatlantic-ambition founders. Pure-EU funds (Speedinvest, Project A, Cherry, HV Capital, Earlybird, BlueYard) may resist or lack network for US flip.

Founder action: if US-listing or US-scale-up is part of your 5-year plan, weight US-bridged funds higher in your target list. If you're explicitly building European-sovereignty infrastructure (Lakestar's pre-pivot thesis), prefer Europe-rooted funds.

Country deep-dive routing

This section is intentionally thin — the post's value is the pan-EU decision frame; country-by-country specifics live in our existing deep-dives.

| Country | 2025 Capital | Key Funds | Peony Deep-Dive |

|---|---|---|---|

| United Kingdom | $14.4B (#1) | Balderton, Index, Atomico, Accel, Plural, Air Street, Felix, Notion, Phoenix Court, Seedcamp, Connect, Kindred, Lightspeed EU | (Future post) |

| Germany | $7.4B (#2) | Cherry, Project A, HV, Earlybird, Visionaries, BlueYard, La Famiglia HQ | (Future post) |

| France | $6.1B (#3) | Partech, Eurazeo, Sofinnova, Serena, XAnge, Daphni, Elaia, Iris, Alven, Ventech | (Future post) |

| Switzerland | est. ~$1.5-2B | Lakestar (Zurich), Redalpine, b-to-v Partners | Read deep-dive → |

| Sweden | est. ~$2-3B (Nordics) | EQT Ventures, Northzone, Creandum, Kinnevik | Read deep-dive → |

| Finland | est. under $1B | Inventure, Lifeline Ventures, Maki.vc, OpenOcean | Read deep-dive → |

| Ireland (Dublin) | est. under $1B | Atlantic Bridge, Frontline Ventures, ACT Venture Capital | Read deep-dive → |

| Denmark | est. under $1B | byFounders, PreSeed Ventures, Heartcore (Copenhagen) | Read deep-dive → |

| Italy (Rome/Milan) | est. under $1B | Indaco Venture Partners, Primo Ventures, P101 | Read deep-dive → |

| Netherlands | est. ~$2B | Endeit, Henq, Volta, Inkef, Slingshot | (Future post) |

| Spain | est. ~$1-1.5B | Kibo Ventures, Seaya, Adara, Samaipata, Nauta Capital | (Future post) |

| Poland | est. under $1B | Vinci, Tar Heel Capital Pathfinder, Inovo, OTB | Read deep-dive → |

| Estonia / Baltics | est. under $500M | Tera Ventures, Karma Ventures, Trind, Specialist Ventures | (Future post) |

Country capital estimates for non-top-3 markets are inferred from $44B total European VC minus the UK/DE/FR top-3 ($28B), leaving ~$16B distributed across 20+ remaining countries. The Atomico SoET 2025 country chapter has authoritative breakdowns; treat the "est." figures above as ranges, not actuals.

Founder pre-pitch playbook — data room readiness

The most common founder mistake when pitching European VCs is dumping a full diligence pack at the first intro call — which both wastes founder time and signals lack of process discipline to the partner. The correct structure is a 3-tier diligence pack with progressive disclosure tied to pipeline stage.

Tier 1 — Cold-Pitch Materials (visible at pitch deck stage):

- 10-13 slide pitch deck (per the Storydoc 2026 benchmark)

- 2-minute company narrative (the "elevator on cold call")

- Founder LinkedIn + advisor / team backgrounds (verifiable)

- Public traction asset (waitlist, GitHub stars, app store ranks, press coverage)

Tier 2 — First Diligence Pack (sent after first call, BEFORE term sheet):

- 3-statement model (P&L + cash flow + balance sheet projections)

- Last 18 months actuals (revenue, MRR, gross margins, CAC, LTV, retention)

- Customer concentration breakdown (% top 5, top 10)

- Cohort retention by month-since-signup

- Cap table (current + post-money on proposed round)

- Hiring plan + 18-month runway model

- Tech architecture overview (1-pager)

- Founder + key-hire bios with references

Tier 3 — Confirmatory Diligence (between term sheet and signing):

- Tax + audit history

- IP assignments + employment contracts

- Customer contracts (top 20)

- Supplier / vendor key dependencies

- Compliance certifications (SOC 2, GDPR, sector-specific)

- Litigation history

A virtual data room organized by these three tiers lets founders open Tier 1 publicly (one-link access for partner sharing), open Tier 2 with NDA + view-only (no download until LOI or term sheet), and hold Tier 3 behind partner-only restricted view (often only Series A+ requires Tier 3).

Peony hosts more than 5,900 customers (May 2026) using this tiered access model. The framework reduces unnecessary information leak in cold rounds — and signals to partners that the founder has run a structured process before. Peony's free tier lets first-time founders manage fundraise burn without paying for a data room they only need for 3-6 months. Page-level analytics show which investors are actually reading the financials versus skimming.

For a deeper data-room checklist tailored to VC fundraising, see our VC fund data room checklist and startup fundraising rounds guide.

FAQ

Which European VC funds actually back first-time founders in 2026, and how do I tell the first-time-friendly funds from the repeat-founder-only ones?

Across the 15 most active pan-European early-stage VC funds we profile in this post, the first-time-friendly cluster is meaningfully narrower than the marketing material suggests. The funds that explicitly run programs or have portfolio composition skewing first-time founder (estimated ~50-60% first-time at first cheque): Seedcamp, Speedinvest, Cherry Ventures, Project A Ventures, Connect Ventures, Phoenix Court / LocalGlobe. The repeat-founder-biased cluster (estimated ~80% repeat at first investment): Sequoia EU, Index Ventures, Atomico, Balderton Capital. The 3-question first-time-founder filter: what percentage of the fund's last 10 investments were repeat founders; does the fund have an explicit first-timer program; what's the median check size (above $5M typically means repeat-founder bias). A first-time founder pitching Sequoia EU is essentially pitching the exception, not the rule.

What are the largest European VC fund closes in 2024-2025, and which actually deploy meaningfully into Europe versus just having a London office?

See the Top 10 table earlier in the post. Critical caveat: Insight Partners $12.5B, Lightspeed $9B, and General Catalyst $8B are firm-wide global vehicles where only a portion (typically 20-30% for Insight, smaller for Lightspeed) deploys to Europe. Pure Europe-mandate flagship raises are Index XII ($2.3B combined: $800M Venture + $1.5B Growth), Atomico ($1.24B), Balderton IX + Growth II ($1.3B; separately $145M Liquidity I continuation), HV IX (€710M, May 2023 vintage), Accel London VIII ($650M), Lakestar Early IV + Growth II (~$600M), and Cherry V ($500M). Founders evaluating fit should ask: "What percentage of your last fund deployed to European companies versus other geographies?"

How do I match my company's stage to the right European VC fund check size, and how does the Stage-Check Mismatch Trap apply in 2026?

See Frame 2 above. Stage-by-check matrix for 2026: $250K-$1M pre-seed lead → Seedcamp, Phoenix Court / LocalGlobe, Connect; $1M-$3M → Speedinvest, Visionaries seed, Point Nine, Kindred, BlueYard; $3M-$10M seed/Series A → Cherry (top of band), Project A (top), Air Street, Earlybird, Notion, GC Famiglia; $10M-$30M Series A lead → Balderton, Accel London, Lakestar Early, Atomico, Index Venture, Sequoia EU, Lightspeed EU; $30M+ → all multi-stage funds plus Insight Partners EU growth. Reverse-engineer fund check size from fund size divided by target portfolio count before pitching.

What's the difference between European VC evaluation timelines for software/AI applications versus deeptech versus climate/hardware?

See Frame 4 above. Three distinct evaluation clocks: Software / AI applications = 6-12 month decision with PMF-on-pitch-deck expectation; Deeptech / AI infrastructure = 9-18 month decision with technical-validation milestones replacing revenue; Climate / hardware / fusion = 12-24 month decision with project-finance hybrid (debt + equity + grants), more selective post-2023 correction. Pitching the wrong evaluation-clock fund wastes 6-12 months of founder time.

Which European VC funds have meaningful Sovereign Wealth Fund LP backing, and why does that change my Series B follow-on probability?

See Frame 5 above. Funds with meaningful SWF LP backing (especially Atomico, Index Ventures, Lakestar Growth) have structural follow-on advantage because Mubadala's ~$400M European tech fund increasingly co-invests with European VCs at Series B+, and Saudi PIF's $36.2B 2025 deployment surge reshapes Series C+ capital availability. The Transatlantic Flip Test is complementary: funds with US partner offices (Sequoia EU, Lightspeed, Index, Accel London, GC Famiglia, Insight, Tiger) have structural advantage for transatlantic-ambition founders.

What data room should I prepare before pitching European VCs?

See the Founder pre-pitch playbook above. 3-tier diligence pack with progressive disclosure: Tier 1 cold-pitch materials (pitch deck + narrative + LinkedIn + traction); Tier 2 first diligence pack (model + actuals + cohorts + cap table); Tier 3 confirmatory (tax, IP, contracts, compliance, litigation). Peony's tiered access model is used by more than 5,900 customers as of June 2026.

How is European VC dry powder distributed across the top 20 funds, and what does that concentration mean for first-time founders pitching the long tail?

See Frame 1 above. European VC dry powder sits at approximately €73B ($86B) as of end-2024. Our analysis estimates 65-75% sits with the top 20 funds — higher than the comparable US figure (~50-60%). For first-time founders, this creates a binary market: either land one of the top 20 names (high competition, narrow founder profiles), or fundraise from the long tail of emerging managers (lower individual cheques, often more founder-aligned terms, slower fundraise process).

Which European VC funds are emerging managers versus established firms in 2026, and how should founders evaluate fund-vintage risk?

Three vintage cohorts in 2026: Established firms (4+ vintage track record) — Balderton IX, Atomico VI, Index XII, Accel London VIII, HV IX, Northzone X, EQT Ventures III, Seedcamp VI, Speedinvest 4, Earlybird VIII, Notion V; Mid-vintage firms (Fund II-IV, post-PMF on fund construction) — Cherry V, Project A V, Connect IV, Kindred IV, Visionaries Club, Plural II, Felix IV, Lakestar Early IV (with strategic pivot caveat), BlueYard III; Solo-GP and emerging-manager wave — Air Street III, GC Famiglia, Phoenix Court ecosystem. Mid-vintage firms (Fund III-V) often offer the best founder economics with adequate reserves and faster decision speed.

What's the right pre-pitch outreach strategy when there are 15-25 European VCs in my target set?

Run a structured 4-week sprint, not a sequential pitch-by-pitch process. Week 1: warm-intro mapping for each fund (identify the partner most likely to lead based on portfolio composition). Week 2: cold outreach to non-warm targets (partner-specific email, avoid info@ addresses). Week 3-4: cluster 8-12 partner meetings in the same 10-business-day window so any term sheet creates competitive tension. Apply the Six-Question Pre-Pitch Filter to each fund — failing 2+ of 6 means do NOT pitch.

How does the broader European VC ecosystem health look in 2026 — is the $375B underfunding gap closing or widening?

Per Atomico SoET 2025: European VC investment hit $44B in 2025 (+7% YoY), the highest since 2021-2022. Macro tailwinds: European tech sector now valued ~$4T (4x in a decade) = 15% of European GDP (vs 4% in 2016); founder sentiment is 50% more optimistic vs 12 months prior; AI captured 31% of EU VC funding in 2025 (Q1 2026 = 51%, first time above 50%). But European pension funds still allocated only 0.01% to VC in 2024 — the $375B 10-year underfunding gap versus US benchmark persists, and Atomico estimates $1T additional is needed over the next decade to stop the gap widening. Fundraising-timing implication: H2 2025 to 2026 is structurally favorable because fund formation peaked in 2024-2025 so deployment pressure is high.

Related resources

- VC fund data room checklist — the LP-side checklist on what your fundraise data room should contain

- Startup fundraising rounds guide — pre-seed through Series C structuring

- Startup fundraising benchmarks Q1 2026 — round size, valuation, and dilution benchmarks

- How to track pitch deck engagement — page-level analytics tied to pipeline stage

- Watermark pitch deck investor email — per-investor dynamic watermarking for leak attribution

- Country-specific VC deep-dives: Switzerland · Sweden · Finland · Dublin/Ireland · Denmark · Italy/Rome