Corporate Acquisition Strategy in 2026: The Machine, Not the Memo

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Corporate Acquisition Strategy in 2026: The Machine, Not the Memo

Last updated: July 2026 · Last verified: July 2026

I'm Sean Yu, co-founder of Peony. I spend most of my time watching the acquirer's side of a deal, and the pattern I have come to trust is this: the companies that win at acquisitions do not have better memos. They have better machinery. I watch serial acquirers run deal after deal through Peony, and the difference between the ones who compound and the ones who stall shows up long before the term sheet — it shows up in whether acquisition #4 is cheaper and faster to run than acquisition #1.

Here is the archetype this post is built around, anonymized into a composite from several teams I have watched. A newly appointed Head of Corporate Development — the first in-house M&A hire at a private-equity-backed B2B software company doing a few hundred million in revenue. The sponsor wants three to five add-ons in 24 months. The CEO has asked for an acquisition strategy memo and a repeatable pipeline. And there are 40 targets sitting in a spreadsheet with no process behind them, no scores, no owner, no plan for what happens after "interesting." That person does not have a strategy problem. They have an infrastructure problem — and they are about to write a memo that will not fix it.

Quick answer: A corporate acquisition strategy that actually works in 2026 is not a memo — it is a machine. The best evidence in M&A says winners buy small, often, and repeatedly: McKinsey found that programmatic acquirers — those doing more than two small-to-midsized deals a year — delivered a median excess total shareholder return of about 2.3 percent per year over the 2013–2022 decade, outperforming every other approach, while organic-only strategies destroyed value. The real difference between programmatic and opportunistic acquirers is not ambition; it is infrastructure: a standing pipeline, a repeatable diligence kit, and deal infrastructure that makes each acquisition cheaper and faster than the last. Deals compound only if the machinery does. And at a 40-target pipeline, your biggest confidentiality risk is internal — a leaked strategy moves markets, spooks founders, and starts retention rumors — so granular access control is a strategy asset, not IT hygiene.

Where this post sits. This is the strategy-and-operating-system guide for a corp-dev leader building a repeatable acquisition capability. It deliberately does not re-explain the mechanics of a single deal — the eight-phase M&A process covers the sequence from LOI to close, merger vs acquisition covers the definitions, and if you are running your very first deal as a one-off, the how to acquire a company guide is the first-timer's single-deal view. What follows is about the layer above any one deal: the system that lets you run many.

What makes an acquisition "strategic" — and platform vs bolt-on

A strategic acquisition is one that buys you something you could not build fast enough, cheaply enough, or well enough on your own — and that fits a thesis you wrote down before you went looking. The word "strategic" gets used to mean "expensive" or "important," but the useful definition is narrower: strategic acquisitions close a specific growth gap in your plan, and you can say in one sentence which gap. If you cannot, you are not making a strategic acquisition; you are making an opportunistic one and calling it strategic after the fact.

The cleanest framework for what kind of strategic value a deal creates comes from Bain, which sorts deals into scale and scope. A scale deal strengthens what you already do — more of the same market, lower unit cost, higher share — and it is driven by cost synergies, which are the reliable kind. A scope deal takes you somewhere new — an adjacent segment, a faster-growing category, a capability or technology you do not have — and it is driven by revenue synergies, which are the hard kind. A capability deal (buy a specific technology or team) is a scope deal wearing work clothes. Bain has tracked scope deals climbing to a record share of large transactions — about 60 percent of deals over $1 billion in 2025 — and there is a reason first-time acquirers gravitate to them: scope deals are exciting. They are also where most of the disappointment lives, because the growth you are buying is growth you still have to earn after close.

Then there is the platform-versus-bolt-on distinction, which is about role rather than value type. A platform is the foundational company — larger, with a management team, systems, and a market position you intend to build on. A bolt-on (or add-on) is a smaller company you tuck into the platform to add customers, products, geography, or capability. In buy-and-build, you establish the platform first and then compound through bolt-ons. The scale of the bolt-on game is easy to miss: add-ons made up roughly three-quarters of US private-equity buyouts by count in 2025, but only about 11 percent by value (PitchBook). Read that ratio twice. Add-ons are where the deals are and megadeals are where the dollars are — which is exactly why add-on strategy is a corporate-development discipline built on repetition, not a once-a-decade megadeal event. If your sponsor already handed you the platform, your entire job is the bolt-on machine.

| Platform acquisition | Bolt-on / add-on | |

|---|---|---|

| Role | Foundational; you build on it | Tucked into an existing platform |

| Typical size | Larger; standalone management | Smaller; $5M–$30M EV band |

| Value driver | Market entry, management, systems | Customers, products, geography, capability |

| Cadence | Rare — once per platform | Repeated — the compounding engine |

The programmatic evidence: winners buy small, often, and repeatedly

The single most important finding in modern M&A research is that a steady diet of small deals beats the occasional big swing. McKinsey studied roughly 2,000 of the world's largest companies across 11,746 transactions over the decade from 2013 to 2022 and sorted them by M&A approach. Programmatic acquirers — companies doing more than two small-to-midsized deals per year — delivered a median excess total shareholder return of about 2.3 percent per year over their peers, and they outperformed every other strategy: large deals, selective deals, and organic-only (McKinsey, October 2021). The organic-only cohort actually destroyed value over the window. Let that reframe the instinct that acquisitions are risky: the riskier move, on this evidence, was standing still.

That 2.3 percent sounds modest until you compound it. Excess TSR is on top of what peers earned, every year, for a decade — the kind of gap that separates a category leader from an also-ran. And McKinsey's own read is that frequency drives it: the most-active programmatic acquirers earned the highest returns. The advantage is not the deals themselves. It is the repetition — each deal makes the next one better-sourced, better-diligenced, and better-integrated, because the organization has done it before and kept the muscle.

You can see the same logic in the public serial acquirers everyone in this seat eventually studies. Constellation Software has acquired well over 500 vertical-market software businesses — some trackers count higher once sub-group tuck-ins are included — organized under operating groups like Volaris, Harris, and Jonas, spanning 900-plus operating companies across more than 100 verticals, and in its busiest recent years its cadence has scaled toward roughly 100 acquisitions annually. That is not opportunism; that is a factory. Danaher built the Danaher Business System over four decades and roughly 400 acquisitions, then spun the capability out into Fortive, Envista, and Veralto — each now its own serial acquirer running the same operating system. Lifco, the Swedish compounder, has done well over a hundred deals since 2006 and consolidated 16 acquisitions in 2025 alone, on a decentralized "keep it simple" model. Halma in the UK runs an explicit target of 15 to 20 acquisitions a year with a dedicated M&A team. The cadence numbers differ; the lesson does not. These companies treat acquisition as a standing capability with dedicated people, a repeatable playbook, and infrastructure that makes the tenth deal of the year cheaper to run than the first.

I run Peony, a data room company used by more than 5,900+ teams, and this is the pattern I watch from the execution layer: the programmatic acquirers are not the ones with the most ambitious memos. They are the ones whose fourth deal of the year reuses the room template, the diligence checklist, and the integration plan from the third. The machine is the moat.

Build vs buy: a decision framework, not a coin flip

Before you buy anything, be honest about whether you should build it instead — because the most expensive acquisitions are the ones that bought a capability the company could have grown. Build-versus-buy is not a mood; it is a framework, and a strategic acquisition should clear it on purpose.

Run each growth gap through six questions:

- Time-to-market. How long would building take, and is that timeline competitively survivable? If the window closes before you ship, buy.

- Cost of build versus premium. What does the internal build truly cost — fully loaded, including the failures — against the acquisition premium? Buying is not automatically dearer once you price the build honestly.

- Talent and IP scarcity. Is the capability something you can hire and assemble, or is it locked in a team and a codebase that took years to earn? Scarce, defensible capability tilts toward buy.

- Integration risk. Can you actually absorb what you would buy? A capability you cannot integrate is worth less than one you can grow, even if the built version is slower.

- Cannibalization and overlap. Does the target's business collide with yours, or extend it? High overlap can be a scale win or an integration nightmare — know which.

- Regulatory and antitrust exposure. Would the deal draw scrutiny that a build would not? Usually minor in the $5M–$30M band, but worth a glance.

The honest output of this framework is that some gaps should be built, some partnered, and only some bought. A strategy that answers "buy" to everything is not a strategy — it is an appetite. The merger vs acquisition distinction matters here too: if the goal is a merger of equals rather than an absorption, the integration math changes entirely.

How to build an M&A pipeline from scratch: the 100→10→1 funnel

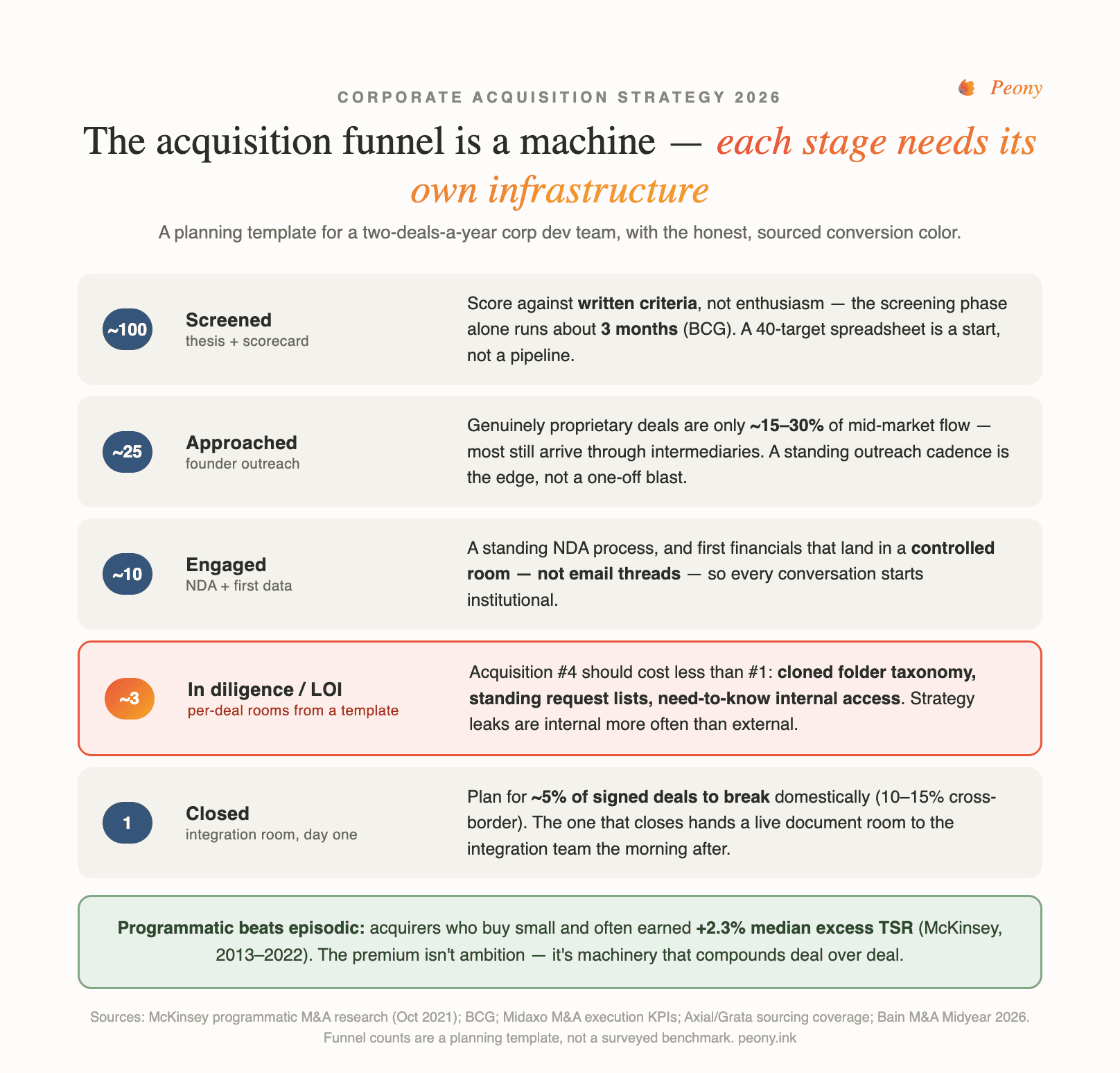

You build a pipeline the way you build any other operating system — as a funnel with named stages, conversion tracking, and a scorecard — not as a spreadsheet of logos you like. This is the single most-searched question a first corp-dev hire asks, and the honest answer starts with a reframe: the pipeline is the product. The deals are just what falls out of a well-run funnel.

The shape most practitioners describe is roughly 100 screened → 10 approached → 1 closed in a year — but treat that as the silhouette of a working year, not a surveyed law. There is no clean, universal "100-to-1" ratio; the discipline is to track each transition separately, because a single blended number hides where you are actually leaking. Screened-to-contacted, contacted-to-first-meeting, meeting-to-LOI, LOI-to-close: each is its own conversion rate, and the one that is broken is the one to fix. Plan for real attrition at the bottom, too — roughly a 5 percent deal-break rate on single-jurisdiction deals and 10 to 15 percent cross-border between LOI and close (Midaxo). And know that most acquirers simply cannot see the whole market: PE firms reportedly see only about 18 percent of relevant deals in their target space (Axial), which is why sourcing coverage is itself a competitive variable.

Now, the 40-target spreadsheet. The problem with it is not the count; it is that a flat list has no priority, so everything is either urgent or ignored. Score each target on four axes:

- Strategic fit — how directly does this target close a gap in your thesis? (Weight this heavily.)

- Integration difficulty — systems, culture, customer overlap. Lower is better.

- Ownership readiness — is the founder near a decision, or years away? (Weight this heavily too.)

- Price expectation — is their number, or their comps, inside your band?

Weight strategic fit and ownership readiness above the other two, because a perfect-fit company that will not sell for three years is not a Q1 target no matter how much you want it. The output is three tiers: a handful of A-targets you actively pursue, a B-list you nurture with periodic, genuine contact, and a C-list you monitor. Re-score quarterly, because ownership readiness moves — a founder's health event, a partner buyout, a soft year — and a C-target can become an A overnight. The scorecard's quiet second job is political: it makes deprioritization defensible when the CEO asks why you are not chasing their favorite logo. "It scored a 4 on ownership readiness — the founder just took growth capital and is not selling for years" is a better answer than a shrug.

Proprietary vs banker sourcing — and how to approach a founder

For sub-$30M add-ons, proprietary sourcing usually wins on price and fit, but you will still need bankers for part of the pipeline — so run proprietary as the default and let bankers extend your reach. The two channels are not rivals; they cover different ground.

A banker-led auction is clean and fast: a curated process, a data room already assembled, a timeline that runs itself. You pay for that convenience twice — in the advisory fee and, more expensively, in the competitive tension that lifts the price and walks you straight toward the winner's curse, where the auction winner is simply the most optimistic bidder in the room. Proprietary sourcing — you, building relationships with founders before they are for sale — is slower, lumpier, and mostly unglamorous relationship work. But genuinely proprietary deals are only about 15 to 30 percent of middle-market flow (V7), which is exactly why the ones you land carry disproportionate advantage: less competition, better price, a founder who already trusts you.

| Proprietary sourcing | Banker-led auction | |

|---|---|---|

| Speed | Slower, lumpier | Faster, process-driven |

| Price tension | Lower — often a one-on-one | Higher — competitive bidding |

| Fit / relationship | Strong — you built it | Variable — you meet at the table |

| Cost | Your time | Advisory fee + premium |

How to approach a founder about acquiring their company

Approach a founder the way you would approach a peer you respect, not a target you are hunting — because for a founder-owned business, the sale is personal, and the first conversation is an audition for whether you are safe to sell to. The move is a warm, direct, discreet outreach that leads with genuine interest in what they built and an explicit acknowledgment that it may not be the right time. Do not open with a number. Do not open with a term sheet. Open with a conversation about their business and their goals, and be honest that you are exploring, not pouncing.

Confidentiality is the whole game at this stage. A founder who suspects their staff might hear about a possible sale will end the conversation immediately, because a leak can trigger exactly the employee and customer flight that destroys the value you are trying to buy. This is why your outreach and early diligence have to be visibly discreet — a signed NDA before anything sensitive changes hands, a private channel for documents rather than an email thread that forwards itself, and a clear message that you understand the stakes. The founder is judging your process because it is the only evidence they have of how you would treat their company and their people after close. Tight process is not just efficiency here; it is courtship.

What to pay: multiples, structure, and overpay guardrails

Pay for what history says gets realized, not for what the model says is possible — because the fastest way to turn a good thesis into a bad deal is to overpay for synergies that never show up. Start with the market. Bain's 2026 midyear report puts the median deal multiple at 11.6x EV/EBITDA (Bain), though larger deals skew that above the $5M–$30M band where add-ons live. The size ladder matters more than the headline: in the same industry, a business with about $1.5M of EBITDA might trade around 3 to 4x, one at $10M around 5 to 7x, and one at $25M around 7 to 9x. Those are illustrative ranges, not promises, and software commands a premium over services.

That ladder is the engine of buy-and-build. Multiple arbitrage works because you buy small add-ons at low multiples and fold them into a platform valued at a higher one, so the blended entry multiple falls with each tuck-in and the whole is re-rated on exit — practitioners often describe an expansion from a 4-to-6x entry toward a 7-to-9x exit. That is real, and it is also why discipline on entry price is non-negotiable: overpay for the add-ons and the arbitrage evaporates.

On structure, the 2026 backdrop has shifted toward shared risk. Bain reports stock-plus-cash consideration reached a historic high of about 35 percent of deals while all-cash fell to a cyclical low of about 55 percent — buyers are spreading risk rather than paying full freight in cash. For founder-owned targets specifically, earnouts are a common bridge over a valuation gap: about 24 percent of private-target deals in 2025 included an earnout, up from 22 percent the year before, with a median earnout around 24 months and roughly 31 percent of the closing payment (SRS Acquiom). An earnout lets a confident founder bet on their own numbers and lets you avoid paying today for growth that may not arrive.

Now the guardrails, because this is where deals go wrong:

- Strategic buyers pay more than financial buyers — often around 10 points more in premium — because they can underwrite synergies a sponsor cannot. That is rational only if the synergies are real. Know which ones are before you bid.

- Price only the synergies history says get realized. Across BCG, McKinsey, and Bain research, cost synergies realize about 70 to 85 percent of announced value; revenue synergies only about 25 to 35 percent (McKinsey). So haircut announced cost synergies by roughly a quarter and revenue synergies by roughly two-thirds when you build the price. The memo should price only what history says gets realized.

- Walk away from the winner's curse. If you are the highest bidder in an auction, ask why everyone else stopped. Being willing to lose a deal is the only thing that keeps you from overpaying for all of them.

This is general information, not investment advice — your comps, your cost of capital, and your integration capacity change the math.

Why integrations fail — and the 100-day plan in one breath

Most acquisitions that disappoint do so at integration, because the value was underwritten as a spreadsheet and has to be delivered as an organizational change — and those are different jobs done by different muscles. The most-quoted warning in the field comes from Clayton Christensen and colleagues, who wrote in Harvard Business Review in March 2011 that "the M&A failure rate is somewhere between 70% and 90%." Cite it the way it deserves: a 2011 synthesis with a loose definition of "failure," useful as a caution, not as a fresh 2026 measurement. The more rigorous read is Bain's: executives who lived through failed deals point to integration as the primary problem about 83 percent of the time (Bain).

The mechanical culprit is synergy overestimation — specifically, revenue synergies. As above, cost synergies realize reliably and revenue synergies mostly miss, so a deal priced on revenue synergies is priced to disappoint. The other failure pattern is treating integration as something that starts after close; the teams that succeed start planning before signing (PwC found 71 percent launch change management before the deal is even signed).

The 100-day plan, in one breath: a single named integration owner who is not the deal lead; Day 1 readiness for payroll, systems access, and communications prepared before close; the two or three synergies that actually justify the price, each with an owner and a number; a 30/60/90 milestone cadence with weekly check-ins; and a deliberate retention plan for the founder and key staff, because people are where value leaks first. That is the summary. The full mechanics — workstreams, the integration management office, cultural integration, the common failure modes — live in our acquisition integration guide, which is the reciprocal depth to this strategy overview.

The acquisition strategy memo: an actual skeleton

The board asked for a memo, so give them one that reads like an operating plan for a repeatable capability — not a pitch for a single deal. A good acquisition strategy memo has six sections, and a target list is not one of them. Here is the skeleton I would hand a first-time corp-dev lead:

- Thesis. Why acquisition is the right tool for this specific growth gap, versus building or partnering. One page. If you cannot name the gap in a sentence, stop here.

- Criteria. The hard filters that turn "interesting" into "in scope": sector, size band ($5M–$30M EV), business model, geography, and explicit deal-breakers. Criteria are what let you say no fast.

- Funnel math. How many targets you will screen, approach, and realistically close, with the attrition assumptions visible. Roughly 100 screened → 10 approached → 1 closed, adjusted to your market, with the transition rates you will track.

- Capacity. How many deals the team and the business can actually integrate at once. This is the real speed limit, and naming it protects you from a mandate you cannot deliver.

- Synergy discipline. What you will and will not pay for, with cost synergies weighted and revenue synergies deliberately under-weighted. State the haircuts. This is the section that keeps you from overpaying.

- Risk. Deal-breakers, integration risk, customer-concentration risk — and the confidentiality plan for keeping the pipeline from leaking internally before anything is signed.

The tell of a strong memo is that it would still be useful if you swapped every target — because it describes a capability, not a transaction. That is the difference between a corp-dev function and a one-off deal.

First 90 days, and looking institutional to founders and bankers

Your first 90 days as Head of Corporate Development should build the machine, not chase the first deal — because a close you were not ready to integrate is worse than a quarter spent getting ready. The honest sequence: write the thesis and criteria, stand up the pipeline and scorecard, build the reusable diligence kit and a data-room template you can clone per deal, and then start working the A-list. The instinct to prove yourself with a fast first close is the instinct to resist; the sponsor hired you to build a capability, and a capability is what compounds.

Which brings up the credibility problem, because a first-time acquirer has no track record to point to. Founders and bankers judge you by the one proxy available: how tightly you run the process in front of them. This is not a soft point. A banker who watches you respond in hours, send a scoped and organized diligence request instead of a 300-item dump, and produce a real data room the moment a target engages will bring you the next deal — because you made their client's life easy and their fee likely. A founder who walks into a clean, well-organized room trusts that you will treat their company well after close. The tell of an amateur is a chaotic diligence phase: files over email, duplicated requests, no clear owner, a scramble to assemble a room after the founder has already said yes. Infrastructure is how a first-timer borrows the credibility they have not yet earned. The machine makes deal #1 look like deal #40 — and process tightness is the honest signal that you are someone worth selling to.

Confidentiality and deal infrastructure: the execution layer

At a 40-target pipeline, your biggest confidentiality risk is not a competitor hacking in — it is your own strategy leaking internally, and that is a leak that moves markets, spooks founders, and starts retention rumors before a single deal is signed. This is the part of acquisition strategy that gets treated as IT hygiene and should be treated as a strategy control. A serial acquirer's live target list is material non-public information about your intentions; if it circulates past the deal team, a competitor learns your roadmap, a target's employees hear they might be sold, and your own staff start guessing who is next. Granular access is not paranoia. It is governance of a strategic asset.

Here is what the execution layer looks like when it is built to compound:

- Internal leak control through granular access. The deal team sees the live pipeline; the wider company does not. When diligence starts, permissions are scoped per person, so a functional reviewer sees only their workstream and nobody sees the full target list who does not need to.

- Per-deal rooms from a template. Each deal gets its own room, cloned from a standing template so you are not rebuilding structure every time. Deal #4 opens in minutes because deal #3 defined the shape. This is precisely the "makes the next deal cheaper" mechanic that programmatic acquirers live on.

- A standing folder taxonomy. One diligence structure — corporate, financial, legal, commercial, tech, HR — reused across every deal, so your team and the seller's advisors always know where things go. A due diligence questionnaire drives the request list; the taxonomy holds the answers.

- An integration room after close. The deal does not end at signing. The same room becomes the integration workspace, carrying the diligence record straight into the 100-day plan so nothing is re-discovered.

- Attribution when it matters. A dynamic per-viewer watermark on every page means anything that leaks is traceable to the person who leaked it, and page-level analytics show exactly who opened what — so you can revoke a single person without tearing down the room.

An honest tool note, because the categories get confused. A pipeline CRM and a data room are different tools that meet at a handoff. DealCloud and Affinity are relationship and pipeline CRMs — they hold the top of the funnel: sourcing, contacts, the relationship history with a founder you have been nurturing for two years. Peony is not a CRM, and I would not pretend otherwise. Peony is the execution layer that sits after "target engaged": the secure room where diligence actually happens, where the founder shares their financials, where your reviewers work under scoped permissions, and where the record carries into integration. The clean stack is a CRM for the pipeline and a data room for the deal. For where the room sits in the deal itself, the M&A data room guide goes deep, and our State of M&A Data Rooms report — built on our own first-party dataset of 334 deals — is the closest thing to a benchmark for how these rooms actually get used.

More than 5,900+ teams run controlled sharing on Peony, and the serial acquirers among them all converge on the same setup: one template, cloned per deal, scoped per person, carried into integration. When an add-on happens to be overseas, the confidentiality and diligence stakes rise — our cross-border M&A guide covers the added regulatory and data-residency layer.

What a data room can't do — and when it's overkill

Two honest concessions, because a strategy post that only sells the tool is not a strategy post. First: a data room will not fix a bad thesis or force integration discipline. If the acquisition does not close a real gap, no amount of clean folder structure will save it; if you overpay for revenue synergies, a watermark will not earn them back; if nobody owns the 100-day plan, a per-deal room will not integrate the company for you. The machine amplifies judgment — it never replaces it. Infrastructure makes a good acquirer faster and a disciplined team more consistent, and it makes a bad deal fail more tidily. That is the honest ceiling.

Second: for a company doing one opportunistic deal every few years, heavyweight infrastructure is overkill. If you are not building a programmatic capability — if an acquisition is a rare event, not a repeated one — then a well-organized shared folder and a solid diligence checklist genuinely beat an elaborate system nobody keeps current. The whole argument of this post is conditional on repetition: the machinery pays for itself when it is reused. Buy the machine when you are going to run it. If you are running one deal, run the deal well and skip the factory.

2026 context: a record market, a friendlier filing environment

The backdrop for acquisition strategy in 2026 is a market that is loud at the top and thin at the bottom — a "K-shaped" year where megadeals boom while deal count contracts. Per LSEG's mid-year data, global announced M&A reached about $2.8 trillion in the first half of 2026, up 48 percent year over year — the strongest first half since records began in 1980 — while deal count fell about 9 percent to roughly 24,000, the weakest first-half count in six years (LSEG via Yahoo Finance). The dollars are concentrated in giants: 47 deals above $10 billion accounted for more than $1.3 trillion of it. Bain's independent read is directionally the same — about $2.4 trillion through May, up 41 percent — and, importantly for a corp-dev leader, Bain notes strategic (corporate) M&A value up about 36 percent year to date, which means corporates, not just sponsors, are driving this rebound.

Two structural forces are worth a corp-dev leader's attention. The first is the AI acqui-hire wave: rather than buy companies outright, the largest tech acquirers have been licensing technology and hiring founding teams — Meta's roughly $14.8 billion for a 49 percent stake in Scale AI, Google's roughly $2.4 billion license-and-hire around Windsurf — structures deliberately built to move fast and stay outside a full merger review. You are probably not doing a $14 billion acqui-hire, but the underlying move (buy the capability, not necessarily the corporate shell) is one to understand when a target's value is really its team.

The second is the regulatory environment, which got friendlier. The 2026 HSR size-of-transaction threshold rose to $133.9 million (FTC/Covington), so most $5M–$30M add-ons sit comfortably below the premerger-filing line to begin with. And the 2025 "updated" HSR form — the one that made filings heavier — was vacated by a federal court in February 2026, so agencies reverted to the lighter pre-update form while a new rulemaking sits pending, not in force (FTC). The net for a buy-and-build program is a more permissive, lighter-filing posture than a year ago. That is a tailwind for exactly the small, frequent deals this whole strategy is built on — the machine runs a little smoother in 2026 than it did in 2025.

Frequently asked questions

How do I build an M&A pipeline from scratch as a first corp dev hire?

Build it as a funnel with named stages and a scorecard, not a spreadsheet of logos. Start by writing the acquisition thesis down to hard criteria — sector, size band, business model, geography, deal-breakers — because a target you cannot screen against your criteria is not a lead, it is a distraction. Then run roughly 100 screened companies down to about 10 you approach and 1 you close: that is the shape of a working year, not a promise. Track each transition separately (screened to contacted, contacted to first meeting, meeting to LOI, LOI to close) so you can see which stage is actually leaking, and plan for real attrition — roughly a 5 percent deal-break rate on single-jurisdiction deals and 10 to 15 percent cross-border between LOI and close (Midaxo). Score every target on strategic fit, integration difficulty, ownership readiness, and price expectation, and re-score quarterly. A CRM like DealCloud or Affinity holds the top of that funnel; a data room like Peony holds the bottom, where diligence actually happens. The pipeline is the product — the deals are just what falls out of it.

How many add-on acquisitions can we realistically close in 24 months?

For a one-to-three-person corporate development team doing $5M to $30M add-ons, a realistic pace is two to four closes per year once the machine is running — so three to five over 24 months is a reasonable sponsor mandate, but only if the first six months build infrastructure rather than chase deals. The binding constraint is rarely deal supply; it is your own integration capacity and diligence bandwidth. A single mid-market deal typically runs three to nine months from target identification to close (BCG puts target screening alone at about three months), and proprietary, already-known targets compress to three to six months while auctions stretch longer. Front-load the pipeline and diligence kit, and deal #4 closes faster than deal #1 because the machinery — the room template, the diligence checklist, the integration plan — is already built. Promise the board a cadence you can integrate, not a count you can announce.

What should go in an acquisition strategy memo for the board?

Six sections, and none of them is a target list. First, the thesis: why acquisition is the right tool for this specific growth gap versus building or partnering. Second, the criteria: the hard filters — sector, size, model, geography, deal-breakers — that turn 'interesting' into 'in scope.' Third, the funnel math: how many targets you will screen, approach, and realistically close, with the attrition assumptions shown. Fourth, capacity: how many deals your team and the business can actually integrate at once, which is the real speed limit. Fifth, synergy discipline: what you will and will not pay for, with revenue synergies deliberately under-weighted because they are the ones that miss. Sixth, risk: the deal-breakers, the integration risks, the concentration risks, and the confidentiality plan for keeping the pipeline from leaking internally. A good memo reads like an operating plan for a repeatable capability, not a pitch for one deal.

Why do most add-on acquisitions fail at integration?

Because the value was underwritten as a spreadsheet and delivered as an organizational change, and the two are not the same job. The most-cited figure — that 70 to 90 percent of acquisitions fail — comes from Clayton Christensen and colleagues in Harvard Business Review (March 2011) and is a loose synthesis, not a fresh measurement, so treat it as a warning rather than a law. The more rigorous read: Bain finds executives who lived through failed deals point to integration as the primary problem about 83 percent of the time. The mechanical reason is synergy overestimation. Across BCG, McKinsey, and Bain post-merger research, cost synergies typically realize about 70 to 85 percent of announced value, but revenue synergies realize only about 25 to 35 percent — so a model that leans on revenue synergies is a model built to disappoint. The fixes are unglamorous: price only the synergies history says get realized, start integration planning before signing, and stand up an integration owner on day one. Depth on that lives in our acquisition integration guide.

How do I keep an acquisition from leaking internally before close?

Treat information access as a strategy control, not IT hygiene, because at a 40-target pipeline the biggest leak risk is internal. A leaked strategy moves markets, spooks the founder you are courting, and starts retention rumors inside the target before anything is signed. The discipline is granular, need-to-know access: the deal team sees the live target list; the wider company does not. When diligence starts, each deal gets its own room with permissions scoped per person, so a functional reviewer sees only their workstream. A dynamic per-viewer watermark on every page means anything that leaks is attributable to the person who leaked it, which changes behavior before it changes evidence. In Peony, access is per named viewer with page-level analytics, so you can see exactly who opened what and revoke a single person without tearing down the room. The point is not paranoia; it is that a serial acquirer's pipeline is a material non-public asset and should be governed like one.

Platform acquisition vs bolt-on — what's the difference and which do we do first?

A platform is the foundational acquisition — usually larger, with a management team, systems, and market position you intend to build on. A bolt-on (or add-on) is a smaller company you tuck into that platform to add customers, products, geography, or capability. In buy-and-build you almost always establish the platform first, then compound value through bolt-ons: add-ons made up roughly three-quarters of US private-equity buyouts by count in 2025 but only about 11 percent by value (PitchBook), which tells you they are numerous and small — a corp-dev story, not a megadeal story. If you already own the platform (you are the sponsor's portfolio company), your job is the bolt-on machine. Borrowing Bain's framing: a scale deal strengthens what you already do and is driven by cost synergies; a scope deal buys new growth or a new capability and is driven by revenue you have to earn. Most first-time programs over-index on scope deals and under-deliver, because scope synergies are the hard ones.

Should we hire a banker or source add-on deals directly from founders?

For sub-$30M add-ons, proprietary sourcing usually wins on price and fit, but you will still need bankers for part of the pipeline, so the honest answer is both — weighted toward proprietary. A banker-led auction is fast and gives you a clean process, but you pay for it twice: in advisory fees and in the competitive tension that lifts the price and exposes you to the winner's curse. Proprietary outreach — you, building relationships with founders before they are for sale — is slower and lumpier, but genuinely proprietary deals are only about 15 to 30 percent of middle-market flow, so the ones you land are disproportionately valuable. The practical build: run proprietary sourcing as your default for the $5M to $30M band where founders often prefer a direct, discreet conversation, and let bankers surface the deals you would never see on your own. Either way, the diligence and execution layer is the same — a controlled room, a repeatable checklist — so the sourcing channel does not change how you run the deal once a target is engaged.

How do I decide which of my 40 spreadsheet targets to pursue first?

Score them, do not rank them by gut. Build a simple scorecard with four axes: strategic fit (how directly the target closes your thesis's growth gap), integration difficulty (systems, culture, customer overlap — lower is better), ownership readiness (is the founder near a decision, or years away), and price expectation (is their number in your band). Weight strategic fit and ownership readiness most heavily, because a perfect-fit target that will not sell for three years is not a Q1 priority no matter how good it looks. The output is three tiers: a handful of A-targets you actively pursue now, a B-list you nurture with periodic contact, and a C-list you monitor. Re-score quarterly, because ownership readiness moves — a founder's health event, a partner buyout, or a soft year can turn a C into an A overnight. The scorecard's real job is to make the deprioritization defensible when the CEO asks why you are not chasing their favorite logo.

What multiple should I expect to pay for a $5–30M B2B software company in 2026?

It depends on size and growth, but the size ladder is the point: smaller companies trade at lower multiples, and that spread is the engine of buy-and-build. Illustratively, in the same industry a business with about $1.5M of EBITDA might trade around 3 to 4x, one at $10M around 5 to 7x, and one at $25M around 7 to 9x — ranges, not promises, and software commands more than services. The market backdrop in 2026 is firm: Bain's midyear report puts the median deal multiple at 11.6x EV/EBITDA across all deals (larger deals skew that higher than your band). Multiple arbitrage is why the math works — you buy small add-ons at lower multiples and fold them into a platform valued at a higher one, so the blended entry multiple falls and the whole is re-rated on exit. Two guardrails: strategic buyers structurally pay a higher premium than financial buyers (often around 10 points more) because they can underwrite synergies a sponsor cannot, so know which synergies are real before you bid; and price only the synergies history says get realized. This is general information, not investment advice.

What should a 100-day integration plan actually include?

A named integration owner, a short list of value drivers, and a cadence — not a 200-line checklist nobody reads. The essentials: a single accountable integration lead (not the deal lead, who is already onto the next target); Day 1 readiness (payroll, systems access, customer and employee communications ready before close, not after); the two or three synergies that actually justify the price, each with an owner and a number; a 30/60/90 milestone rhythm with weekly check-ins; and a deliberate people plan, because retention of the founder and key staff is usually where value leaks first. Crucially, start planning before signing — PwC found 71 percent of acquirers now launch change management before the deal is signed. Cost synergies get the aggressive timeline because they realize reliably (about 70 to 85 percent of announced value); revenue synergies get a conservative one because they mostly miss (about 25 to 35 percent). This is a summary — our acquisition integration guide covers the 100-day plan in full depth.

How do I look institutional to founders and bankers as a first-time acquirer?

Process tightness, not polish. Founders and bankers cannot see your track record if you do not have one, so they judge you by the only proxy available: how cleanly you run the process in front of them. That means responding within hours, not days; sending a diligence request list that is scoped and organized rather than a 300-item dump; having a real data room ready the moment a target engages instead of scrambling to build one; and closing the loops you open. A banker who watches you run a tight, low-friction process will bring you the next deal, because you made their client's life easy and their fee likely. The tell of an amateur is a chaotic diligence phase — files over email, duplicated requests, no clear owner. The tell of a professional is a room the founder can walk into and immediately trust. Infrastructure is how a first-timer borrows the credibility they have not yet earned; the machine makes deal #1 look like deal #40.

Related Resources

- Acquisition Integration Guide — the reciprocal depth to this post: the 100-day plan, the integration management office, and why deals fail after close

- Mergers and Acquisitions Process Guide — the eight-phase mechanics of a single deal, from LOI to close

- How to Acquire a Company — the first-timer's single-deal view for a one-off acquisition

- Cross-Border M&A Guide — the added regulatory and data-residency layer when an add-on is overseas

- Merger vs Acquisition — the definitions, and why the distinction changes the integration math

- M&A Data Room — how the execution layer works inside a deal

- State of M&A Data Rooms — benchmarks from our first-party dataset of 334 deals

- Due Diligence Questionnaire — the request list that drives the diligence room