How to Acquire a Company in 2026: A First-Time Buyer's Playbook for $1M–$25M Deals

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

How to Acquire a Company in 2026: A First-Time Buyer's Playbook for $1M–$25M Deals

Last updated: July 2026 · Last verified: July 2026

I'm Sean Yu, co-founder of Peony. I run Peony, a data room company, which means I do not sit in the buyer's seat myself — I watch thousands of deal teams run acquisitions through our rooms, and the ones that close look different from the ones that stall in ways that have almost nothing to do with the headline price.

Here is the archetype this post is built around, anonymized and composited from many real buyers. An operator leaves a corporate job to buy a business. Eight months into the search, they have evaluated dozens of companies and lost two LOIs — one outbid, one that fell apart when the seller got cold feet. The third time, they sign an LOI on a home-services business: $4.2M price, roughly $1.1M in SDE, a multiple of 3.8x, a 75-day exclusivity window. And then the real work starts, because the seller runs the company out of a personal email account, sends financials as attachments whenever asked, and has never heard the phrase "quality of earnings." The buyer has never run diligence, the QoE quote feels expensive, and the whole thing has to clear SBA financing before the clock runs out. If that is roughly where you are, this is written for you.

Quick answer: To acquire a company in the $1M–$25M band in 2026, you line up SBA 7(a) financing (10% minimum equity injection under the current SOP 50 10 8 rules), sign an LOI with a 60-to-90-day exclusivity window (75 days in the running example here), and use that window to verify that the earnings you agreed to pay a multiple on are real — because first acquisitions do not die at the LOI price, they die in the gap between the handshake number and verifiable earnings. Your real job during exclusivity is closing that gap faster than the deal decays: hire a quality-of-earnings firm to confirm the SDE, run financial, customer, and legal diligence in parallel with SBA underwriting, and — because the seller is almost always disorganized — stand up the data room yourself so your QoE firm, attorney, and lender all pull from one clean, access-controlled place. Get the earnings verified and the financing closed inside the window, and you own a business.

Where this post sits. This is the first-time individual buyer's operating manual — the searcher, the self-funded operator, the person buying one company with SBA leverage. It is deliberately not the neutral corporate M&A process; for that institutional, phase-by-phase view, see the mergers and acquisitions process guide. It also is not a diligence deep-dive: I keep diligence here at the operating-plan level and hand off the item-by-item work to small business due diligence. What follows is the vocabulary and the sequence a first-timer actually needs — SBA, SDE, QoE, exclusivity, cash to close — and one move most guides miss entirely.

What do acquisitions actually look like in the $1M–$25M band?

They look like individuals buying real, unglamorous, profitable businesses — and there are more of them coming to market than at any point in a generation. On the small end, the marketplace data is concrete: BizBuySell reported 9,586 closed transactions in 2025, with a median sale price of $350,000 and a sale-to-asking-price ratio of 94%, at an average of about 2.6x cash flow (SDE). That is Main Street — roughly 80% of those deals are under $2M. Your $4.2M home-services deal sits a rung above it, in the lower-middle market, where the buyer pool shifts. Per the IBBA Market Pulse full-year 2025 data, individual buyers make up about 44% of lower-middle-market acquisitions (roughly 26% first-time and 18% serial), with private equity around 25% — so a first-time individual buyer is not an outlier here, they are the modal buyer. And it is a competitive market: in the Q1 2026 Market Pulse survey, 83% of deals above $5M drew three or more offers.

Two structural facts frame the moment. First, it is a seller's market in the lower-middle market heading into 2026, per IBBA — deals above $5M routinely draw three or more offers. Second, there is a demographic tailwind underneath it: McKinsey estimates that roughly 6 million US businesses will change hands by 2035, with about 1 million actually selling for a cumulative $5 trillion. (You will see much larger "$10–14 trillion" numbers quoted; treat them with caution, because they lump in millions of micro-businesses that will simply wind down rather than sell.) The takeaway for a buyer: supply is real and growing, but competition for the good ones is real too, which is exactly why losing a couple of LOIs before one sticks is normal, not a sign you are doing it wrong.

For the institutionally-financed search path specifically, the benchmarks come from Stanford. Per Stanford's 2026 Search Fund Study (data through the end of 2025), traditional multi-investor search funds have posted an aggregate pre-tax IRR around 33.9% and a return on invested capital near 4.75x across the funds tracked — with the important caveat that the study covers only traditional, multi-investor funds and explicitly excludes self-funded and SBA-financed searches, which are the most numerous form but have no rigorous public dataset. So do not anchor your own expected return to a search-fund IRR; anchor it to the specific earnings of the specific business in front of you.

How does the money get designed — SBA 7(a) under SOP 50 10 8?

The financing is designed around one government-backed instrument, and in 2026 the rules changed in ways that make older guides actively wrong. The SBA 7(a) loan is the workhorse for buying a business in this band: it funds acquisitions up to a $5,000,000 loan amount, amortizes over 10 years (up to 25 years if real estate is more than half the proceeds), and in FY2025 the program approved roughly $37.3 billion across about 78,000 loans. Business acquisition is among its largest use cases. For a first-time buyer with no operating history and a goodwill-heavy services target, a conventional acquisition loan usually is not available at all, which is why SBA leads.

The news is SOP 50 10 8, effective June 1, 2025, which largely reinstates pre-2021 underwriting discipline. Three changes matter most to your deal:

- A minimum 10% equity injection is back for changes of ownership. On a $4.2M deal, that is $420,000 of equity into the project, and the lender must verify its source — the old "do what you do" flexibility on sourcing the injection is gone.

- Seller notes count as equity only on full standby. To have a seller note count toward that 10%, it must be on full standby — no principal and no interest paid for the entire term of the SBA loan (typically 10 years) — and it can cover at most half of the required injection. The previous 24-month partial-standby pathway no longer counts. So a full-standby seller note can supply up to $210,000 of your $420,000 injection; the other $210,000 must be genuine, verified cash.

- Partial buyouts must be stock purchases. If you buy less than 100% of the company, the deal must be structured as a stock purchase, and every owner must personally guarantee for at least two years regardless of stake — which effectively kills SBA-financed seller rollover equity.

One more 2026 change to know: per SBA policy updates, 100% of all direct and indirect owners must now be US citizens or nationals — the prior 5% foreign-ownership allowance was rescinded, so even a small non-citizen stake can make the business ineligible. This area is still evolving, so confirm the operative rule with your lender.

Here is how the three financing routes stack up for a first-time buyer at this size:

| Financing route | Equity / down | Realistic for a first-timer? | Main trade-off |

|---|---|---|---|

| SBA 7(a) | 10% minimum injection (full-standby seller note covers up to half) | Yes — the default | Personal guarantee, 60–90-day underwriting |

| Conventional loan | Typically far more equity + hard collateral | Rarely — needs history and collateral you lack | Hard to qualify for a goodwill-heavy business |

| Seller-financing-heavy | Large seller note carries the price | Only if the seller agrees to carry the majority | Sellers seldom carry most of a multi-million price |

Is $1.1M SDE enough to service SBA debt and pay myself?

Yes, comfortably — and this is the calculation your lender runs, so run it yourself first. The metric is the debt-service coverage ratio (DSCR): cash available to service debt, divided by annual debt service. SBA lenders generally want a DSCR of at least about 1.15x. Work the example. As of July 2026, WSJ Prime is 6.75%; a strong-borrower 7(a) acquisition loan commonly prices around Prime plus 2.25% to 2.75%, so call it 9.25%. Finance $3.78M (the $4.2M price minus the 10% injection) over 10 years at 9.25%, and annual debt service is roughly $581,000.

Now the coverage. On the full $1.1M of SDE, DSCR is about 1.89x. But the bank knows you need to eat, so it looks at coverage after a reasonable owner's salary: net a $150,000 salary and DSCR is still about 1.64x — well above the 1.15x floor, leaving roughly $369,000 of cash after debt service and your pay. Here is where diligence connects to financing: if the QoE strips that bogus $60,000 add-back and true SDE is $1.04M, DSCR net of your salary falls to about 1.53x. Still bankable — but the exercise shows exactly how an inflated add-back quietly eats your cushion. Rates cutting over the back half of 2025 have helped; lower Prime means lower debt service and more coverage room than a buyer would have had at the 2023 peak. (This is illustrative math, not a rate quote — your lender's actual spread, fees, and salary assumptions will move the numbers.)

How do I verify the seller's SDE add-backs before I trust the multiple?

You verify each add-back against source documents and test whether the expense actually disappears under your ownership — because the multiple is only as honest as the earnings base underneath it. This is the single highest-leverage hour of diligence, and the place first-timers most often overpay. SDE (Seller's Discretionary Earnings) starts from net profit and adds back one owner's salary and benefits, interest, taxes, depreciation, and genuinely discretionary or one-time costs. The legitimate add-backs prove themselves on paper; the dangerous ones are recurring costs dressed up as one-time.

Work the example, because it is the whole lesson. A seller presents $1.1M of SDE built like this:

| Line item | Amount | Legitimate add-back? |

|---|---|---|

| Operating profit (base) | $820,000 | Base earnings |

| Add back: owner's salary and benefits | $180,000 | Yes — one owner, verified from payroll |

| Add back: owner's personal vehicle and travel | $40,000 | Yes — with receipts |

| Add back: "one-time consulting fee" | $60,000 | No — appears in three consecutive years |

| Seller's stated SDE | $1,100,000 |

Reconcile that consulting fee against the general ledger and it shows up every year — it is not one-time, it is a real recurring cost of running the business. Strip it and true SDE is about $1.04M. That one correction matters two ways: at the agreed 3.8x, the price you set on the headline number is really about 4.0x on the sustainable number, and (as the DSCR math above showed) your debt-service cushion shrinks. The discipline: reconcile the P&L to three years of federal tax returns line by line, demand documentation for every material add-back, and where the seller's financials and the tax returns diverge, trust the tax return — the seller had a reason to minimize what they told the IRS. This is exactly the work a QoE firm does professionally, which is why the next section says buy the earnings verification even when you run everything else yourself.

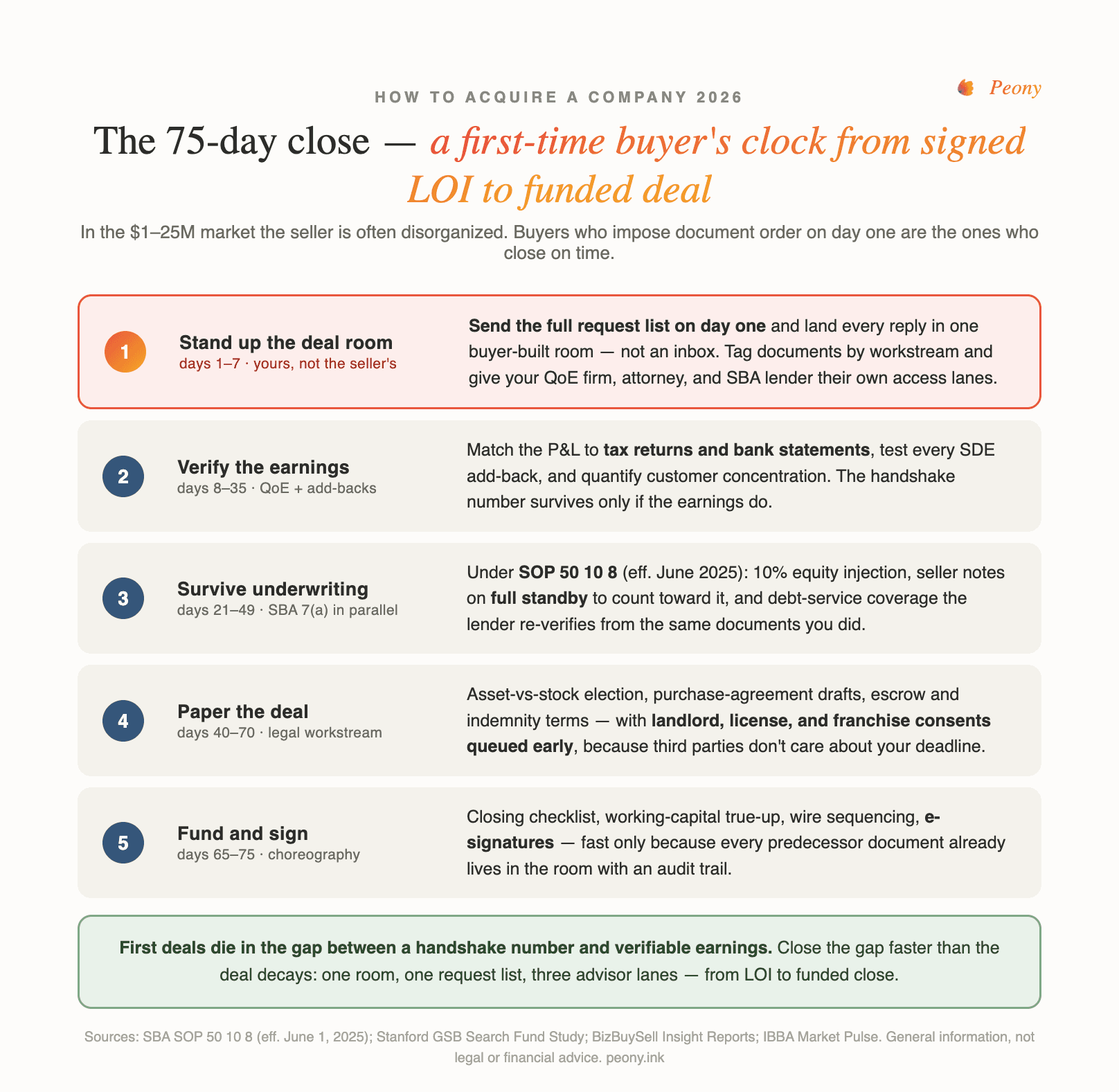

What does the 75-day exclusivity operating plan look like, week by week?

Exclusivity is not a waiting period — it is a countdown, and the deal decays a little every day you are in it. Your one job across these weeks is to close the gap between the handshake number and verifiable earnings before either the clock or the seller's patience runs out. The reason 75 days feels tight is arithmetic: SBA underwriting alone runs 60 to 90 days, so if you treat diligence and financing as sequential — finish diligence, then start the loan — you will blow the window. Everything below runs in parallel.

- Week 1 — start both clocks. Send the full document request list to the seller on day one, and submit your SBA loan application the same week. The lender's 60-to-90-day clock has to start now, not after diligence. Engage your QoE firm and your deal attorney.

- Weeks 2–5 — active diligence, everything at once. QoE fieldwork (itself a four-to-six-week process) runs alongside your customer, legal, and operational review, while the lender orders its appraisal and independent business valuation. Test customer concentration early, because it is a common deal-killer and you want the bad news in week two, not week seven.

- Weeks 6–8 — negotiate the agreement and clear conditions. With QoE findings in hand, negotiate the purchase agreement (and re-price if diligence proved the earnings base is smaller than claimed), and work through the lender's closing conditions.

- Final stretch — close. Working-capital true-up, final SBA sign-off, and the closing itself, executed by e-signature.

Two things break this timeline, and both are avoidable. The first is starting SBA underwriting late — fully in your control. The second is a disorganized seller who cannot produce documents fast enough, which is the single most common reason a first-timer runs out of exclusivity. That is what the next section is about, and it is the move most guides skip. In practice, plenty of $1M–$25M SBA deals take 90 to 120 days from LOI, so if your window is a firm 75, plan the parallel track from day one and be ready to ask for a short extension if the lender's timeline runs long.

How do I get financials from a disorganized seller? Build the data room yourself.

Here is the counterintuitive move that separates buyers who close from buyers who stall: in the $1M–$25M market, the seller is almost always disorganized, so the buyer stands up the deal workspace. This flips the usual assumption that the seller hosts the data room. In a big institutional deal, a sell-side investment banker runs a polished VDR and grants buyers access. In your deal, the seller has no advisor running a process, no room, and a filing system that is some email attachments, a shoebox, and one bank-statement folder. If you wait for them to get organized, you will lose the window. So you organize the chaos into one room — and it becomes the operational backbone of the whole close. 5,900+ companies run deals on Peony, and on the buy side the pattern that repeats is exactly this: the buyer builds the room.

Call it the buyer-built data room, and run it as a five-step protocol:

- Send the request list on day one. Do not ask for documents piecemeal as questions occur to you — that is how weeks disappear. Issue one structured request list covering all eight diligence categories (financial, customer, legal, tax, operations, HR, assets, corporate) at the start of exclusivity, so the seller has a single checklist and you have a single scoreboard of what is in and what is outstanding. Use a file-collection workflow so the seller uploads directly instead of emailing attachments.

- One room, not email. Every document lands in one access-controlled room, not scattered across inboxes. This kills version chaos (there is one current P&L, not five in a thread), and it gives you a timestamped record of exactly what the seller produced and when — which matters if a dispute ever arises about what was disclosed.

- Tag by workstream. Organize the room by diligence category so your QoE firm goes straight to the financials, your attorney to the contracts and corporate documents, and your lender to the tax returns and bank statements. Nobody wastes billable time hunting.

- Give your advisors their own access lanes. Your QoE firm, your deal attorney, and your SBA lender each get their own access — pulling from the same source of truth rather than waiting on you to forward files. On Peony, viewers are free and unlimited, so putting your lender, QoE analyst, and counsel in the room costs you nothing per seat, and page-level analytics show you who has actually reviewed what.

- Version discipline through close. As the seller produces updated statements or corrected schedules, the room holds the current version and the history, so at closing there is no argument about which numbers were final. Restrict, watermark, and (if needed) expire access so the deal's document set stays under your control right through the funding date.

Now the honest part, because a deal room is not always the answer. If the seller's entire document set is a dozen files and one bank-statement folder, a shared drive is genuinely fine — you do not need to stand up a room to hold twelve PDFs. A deal room earns its keep when you cross roughly 100 documents, multiple advisor lanes pulling in parallel, and a lender who needs a clean audit trail — which is exactly what a $1M–$25M acquisition with a QoE firm, an attorney, and an SBA underwriter becomes. Below that threshold, keep it simple. Above it, the room is what lets you run the 75-day clock without dropping a thread. (For what the pros put in a room, the due diligence data room checklist is the structure; how to prepare for due diligence is the readiness view.)

Should I hire a QoE firm, or can I do the earnings work myself?

Hire the QoE firm and do the rest yourself — and be honest that this is the one place where an advisor's judgment beats your organization and effort. You can and should personally run the operational, customer, and legal review: read the contracts, call the customer references, walk the shop floor, interview the key employees. What you should not do yourself is certify that the earnings you are paying 3.8x for are real. A quality-of-earnings firm reconstructs the seller's earnings from bank statements, tax returns, and the general ledger, performs a proof-of-cash, and tells you the number your equity and your lender are actually backing.

The reason to pay for it rather than DIY is pattern recognition: a QoE analyst who has read a hundred add-back schedules knows instantly which normalization is standard and which is a stretch, and that judgment cannot be replaced by organizing the files well. Organizing the files well is your job — it makes the QoE faster and cheaper. Reading the files correctly is theirs. On cost, the ranges are tiered by deal size:

| QoE tier (by target EBITDA/SDE) | Typical QoE cost | Legal (buy-side APA + SBA) | Notes |

|---|---|---|---|

| Under $3M | $15,000–$25,000 (boutiques lower) | $10,000–$25,000 | Where a ~$1.1M SDE deal sits |

| $3M–$10M | $25,000–$50,000 | $20,000–$40,000 | Heavier scope, longer proof-of-cash |

| $10M+ | $50,000–$75,000+ | $40,000+ | Institutional-grade |

A $38,000 quote on a $1.1M-SDE business sits above the typical band for that size, which is a fair thing to question — it usually signals extra scope (deeper concentration testing, a messier ledger). But scope is not waste, and $38,000 is under 1% of a $4.2M price. Set against the most common first-timer mistake — overpaying because SDE was inflated — the report is cheap insurance. Ask the firm to scope it to your specific risks; do not skip it to save the fee.

What kills SBA acquisition deals in underwriting?

Deals in this band die from a short list of predictable causes, and the pattern is consistent: of signed LOIs, roughly 30% to 50% fall apart in diligence and another chunk get re-traded, so only about a third close cleanly on the original terms. SBA-financed deals under $1M fail at rates of up to about 40% because the financing adds its own failure points. The recurring killers:

- Underwriting kills. The lender's independent business valuation comes in below the purchase price, the DSCR does not clear the ~1.15x floor after a reasonable owner's salary, or the equity injection cannot be verified to the source under SOP 50 10 8. This is why you run the DSCR math yourself before you are emotionally committed.

- Customer concentration. A single customer over about 20% of revenue draws valuation adjustments; above 25% to 30% it becomes deal-threatening, per advisor commentary on concentration risk. The specific trap is a change-of-control clause in a big customer's contract that lets them walk when ownership changes — the exact loss you were worried about, triggered by the deal itself.

- Tax-return mismatches. When the seller's financials do not reconcile to their filed federal tax returns, both your QoE firm and your lender will flag it, and the gap either re-prices the deal or ends it. Earnings and QoE discrepancies are among the most-cited deal-killers.

- Running out of exclusivity. The deal does not die from a finding — it dies because SBA underwriting was started too late and the window closed. Avoidable, and the reason the whole plan runs in parallel.

The through-line: none of these are exotic. A buyer who runs the DSCR early, tests concentration in week two, reconciles to the tax returns, and starts the loan on day one has removed most of the ways the deal dies. For the broader catalog of warning signs, due diligence red flags goes deeper than I do here.

How do the closing mechanics work — structure, escrow, and signing?

Closing comes down to how the deal is legally structured, how risk is held back after you pay, and how the documents get executed. On structure, most small acquisitions are asset purchases, and a first-time buyer should generally prefer one: you buy named assets, assume only named liabilities (leaving unknown liabilities behind with the old entity), and get a stepped-up tax basis that fuels future depreciation deductions. Sellers often prefer a stock sale for cleaner capital-gains treatment, so structure is negotiated. Two nuances at this size: SBA's SOP 50 10 8 forces a stock purchase for partial buyouts, and when the seller is an S-corporation (most lower-middle-market businesses are), an F-reorganization under IRC Section 368(a)(1)(F) is a common pre-sale restructuring that lets the seller sell LLC units for capital-gains treatment while you still get asset-sale tax treatment.

On holding back risk: at this deal size, risk is held back the old-fashioned way — through escrow, indemnification, and the seller note — not through representations-and-warranties insurance (RWI), which is largely uneconomical below roughly $10M–$20M in enterprise value and is not a standard SMB tool. In deals without RWI, a general indemnity escrow of around 10% of transaction value is a common reference point, though SMB terms vary widely and your seller note itself functions as security. Seller financing is near-universal at this size: per IBBA, seller notes appear in roughly 75% to 90% of transactions under $5M, and BizBuySell reports that most sub-$2M deals combine an SBA loan with a seller note.

Then you sign. E-signature is now the norm for SMB closings — the purchase agreement, ancillary documents, and much of the SBA loan package are executed electronically, with only a handful of instruments (certain notarized or recorded documents, the occasional wet-ink lender requirement) still needing ink. Peony includes e-signature so the same room that held diligence can carry the signing, keeping the executed set with the record of what was disclosed.

To put the cash together in one place, here is an illustrative cash-to-close stack for the $4.2M deal — your actual numbers will differ:

| Cash-to-close component | Illustrative amount | Notes |

|---|---|---|

| Equity injection (10% of $4.2M) | $420,000 | SOP 50 10 8 minimum |

| Less: full-standby seller note (counts up to half) | ($210,000) | Reduces your cash injection |

| Buyer cash injection (verified) | $210,000 | The real out-of-pocket equity |

| QoE report | ~$20,000 | Under-$3M band |

| Buy-side legal (APA + SBA) | ~$22,000 | Deal attorney |

| Title, filing, lien search, appraisal, misc. | ~$8,000 | Third-party closing costs |

| Illustrative buyer cash to close | ~$260,000 | Excludes SBA guaranty fee, often financed into the loan |

The SBA guaranty fee is a real cost but is commonly financed into the loan rather than paid out of pocket, so I have left it out of the cash figure — confirm how your lender handles it. The headline: on a $4.2M purchase, a first-time buyer's genuine cash to close lands in the low-to-mid six figures, not seven, precisely because SBA leverage and a full-standby seller note do most of the lifting.

When is a deal room overkill, and where do advisors beat software?

A deal room is overkill when the deal is genuinely tiny, and software never replaces judgment — I would rather say both plainly than oversell the tool. If the seller's entire document set is a dozen files and one folder of bank statements, a shared drive is fine; the room earns its keep once you cross roughly 100 documents, multiple advisor lanes, and a lender who needs a clean audit trail. And even in a room-worthy deal, the room organizes the diligence — it does not perform it. A QoE firm's judgment about which add-back is a stretch, a deal attorney's read on an indemnity clause, a lender's underwriting call: none of those are things you can substitute with good folder structure. The room makes the experts faster and gives you one clean, timestamped record; the experts still do the thinking. Buy the organization for what it is worth, and buy the judgment separately.

Across the 5,900+ companies that run deals on Peony, the buyers who close a first acquisition are not the ones with the fanciest room — they are the ones who paired a clean, buyer-built workspace with advisors whose judgment they actually paid for. The tool is leverage on the humans, not a substitute for them.

If you are a company buying repeatedly rather than an individual buying once, the discipline scales up into a program — see corporate acquisition strategy. And if the target is overseas, the diligence and structuring change materially; cross-border M&A covers that world.

This post is general information, not legal, tax, or investment advice — the specifics of your structure, your SBA eligibility, and your tax treatment are questions for your deal attorney, CPA, and lender.

Frequently asked questions

Should I hire a QoE firm or do due diligence myself as a first-time buyer?

Hire a quality-of-earnings (QoE) firm, and do the rest of diligence yourself. A first-time buyer can and should personally run the operational, customer, and legal review — reading contracts, calling references, walking the shop floor. What you should not do yourself is verify whether the earnings you are paying a multiple on are real. A QoE firm reconstructs the seller's earnings from bank statements, tax returns, and the general ledger, strips out add-backs that do not survive scrutiny, and tells you the number your lender and your own equity are actually backing. For a business with roughly $1.1M of SDE, a QoE runs about $15,000 to $25,000 (boutiques can be lower), against a purchase price in the low millions — the cost of the report is a rounding error next to the cost of overpaying because a $60,000 add-back turned out to recur every year. Where advisors genuinely beat software and self-effort is judgment: a QoE analyst who has seen a hundred add-back schedules knows which normalization is a stretch and which is standard, and that pattern recognition cannot be replaced by organizing the files well. Organize the diligence yourself; buy the earnings verification.

Is $38K for a quality of earnings report worth it on a $4.2M deal?

On a $4.2M deal, yes — though $38,000 sits at the high end for a business this size, and you should ask why. Published 2026 QoE pricing runs roughly $15,000 to $25,000 for targets under $3M of EBITDA/SDE, $25,000 to $50,000 for $3M to $10M, and $50,000-plus above that, per QoE-firm and M&A-advisory rate cards. A business with about $1.1M of SDE falls in the lower band, so a $38,000 quote likely reflects extra scope — heavier customer-concentration testing, a proof-of-cash over more months, or add-back work on a messy general ledger. That is not necessarily wrong; a disorganized seller makes QoE harder and the deeper look can be exactly what saves you. The way to judge it is against what the report protects: $38,000 is under 1% of a $4.2M price, and the single most common first-timer mistake advisors cite is overpaying because SDE was inflated or misunderstood. If the QoE catches one recurring expense misclassified as a one-time add-back, it pays for itself several times over. Ask the firm to scope it to your specific risks rather than accepting a flat quote, but do not skip it to save the fee.

How do I know if I'm overpaying for the business I'm buying?

You are overpaying when the price is built on earnings you cannot verify or a multiple borrowed from a different size class. Two errors drive almost every first-timer overpay. The first is trusting seller-provided financials over tax returns: reconcile the profit-and-loss statement to the filed federal returns line by line, and where they diverge, the tax return is the more conservative anchor because the seller had a reason to minimize it. The second is applying the wrong multiple to the wrong earnings base — pricing a business on an EBITDA multiple when it should be valued on SDE, or vice versa. Below roughly $1M to $2M of earnings, small businesses are priced as a multiple of SDE (Seller's Discretionary Earnings, which adds back one owner's salary and discretionary items); above that band, on adjusted EBITDA. Because SDE is a larger number than EBITDA for the same business, SDE multiples read lower — so never compare an SDE multiple to an EBITDA multiple head to head. The defense is a QoE report to confirm the earnings, a comparison to reported market multiples for your size and sector, and the discipline to re-price if diligence proves the earnings base is smaller than the seller claimed. If your lender's independent business valuation comes in below your purchase price, that is the market telling you the number is high.

Is 3.8x SDE a fair multiple for a home-services business?

For a home-services business with clean, verifiable earnings, 3.8x SDE is in a defensible range — well above the Main Street average, but a modest premium against the size-appropriate band for a business with seven-figure SDE — and the point of diligence is to confirm the business earns that premium. Reported marketplace data put the average small-business sale at roughly 2.6x SDE for 2025, with multiples rising with size and earnings quality; larger, cleaner businesses command more. A home-services business with about $1.1M of SDE is well past micro-business scale, so a multiple in the high-3x to low-4x range is credible if the earnings survive a QoE, customer concentration is low, the revenue is recurring or repeat rather than one-time project work, and the business does not depend entirely on the departing owner's relationships. The multiple is not fair or unfair in the abstract — it is fair if the earnings it multiplies are real and durable. If diligence shows a chunk of SDE came from a one-time contract or a single customer who may leave, then 3.8x on the headline number is really a higher multiple on the sustainable number, and that is your opening to re-price. Judge the multiple and the earnings base together, never separately.

SBA 7(a) vs conventional loan for buying a business — which should a first-time buyer use?

For a first-time buyer of a $1M to $5M business, the SBA 7(a) loan is almost always the right tool, because conventional acquisition lending rarely shows up for a buyer with no operating history and limited collateral. The 7(a) program is built for exactly this: it funds business acquisitions up to a $5,000,000 loan amount, amortizes over 10 years (up to 25 if real estate is more than half the proceeds), and requires a minimum 10% equity injection under the current SOP 50 10 8 rules effective June 1, 2025. A conventional loan will typically demand far more equity, hard collateral beyond the business itself, and a track record you do not yet have — so most first-timers cannot get one for a goodwill-heavy services business. The trade-offs of going SBA are a personal guarantee, a lien on your assets, mandatory SBA paperwork, and an underwriting timeline of roughly 60 to 90 days that eats most of your exclusivity window. A seller-financing-heavy structure can supplement the 7(a) but rarely replaces it at this size, since sellers seldom carry the majority of a multi-million-dollar price. The practical answer: lead with SBA 7(a), layer a seller note on top, and use conventional debt only if you have the collateral and history to qualify.

What are the SBA rules on seller notes — standby vs full standby?

Under SOP 50 10 8, effective June 1, 2025, a seller note counts toward your required 10% equity injection only if it is on full standby — no principal and no interest paid for the entire term of the SBA loan, typically 10 years — and it can cover at most half of the required injection. This is the change that trips up buyers reading older guides: the previous pathway, where a seller note on partial standby for just 24 months counted as equity, is gone. So on a $4.2M deal, the 10% injection is $420,000; a full-standby seller note can supply up to $210,000 of that, and you must fund the remaining $210,000 in genuine cash (or another approved source the lender verifies). A seller note that pays interest, or that starts amortizing before the SBA loan is retired, is still allowed as part of the overall deal structure — it just does not count toward the equity injection. The other SOP 50 10 8 trap: if you are buying less than 100% of the company (a partial change of ownership), the deal must be structured as a stock purchase and every owner must personally guarantee for at least two years regardless of stake, which effectively rules out SBA-financed seller rollover equity. Date every SBA claim you read to SOP 50 10 8, because the pre-2025 rules were materially looser.

How do I verify the seller's SDE add-backs are legitimate?

You verify add-backs by demanding documentation for each one and testing whether the expense truly disappears under your ownership. SDE starts from net profit and adds back the owner's salary and benefits, interest, taxes, depreciation, and genuinely discretionary or one-time costs. The legitimate add-backs are easy to prove: one owner's compensation (from payroll records), personal expenses run through the business (with receipts), and true one-time costs like a lawsuit settlement or a one-off equipment repair (with the invoice showing it was a single event). The add-backs to challenge are the ones that quietly recur. A classic example: a seller presents $1.1M of SDE built on operating profit plus a $180,000 owner salary add-back, a $40,000 personal-vehicle add-back, and a $60,000 'one-time consulting fee' — but the general ledger shows that consulting fee appearing in three consecutive years. It is not one-time; it is a real, recurring cost of running the business. Strip it and true SDE is about $1.04M, which means the price you agreed reflects a higher effective multiple than you thought. Cross-check every material add-back against the tax returns and the general ledger, and make the seller substantiate each line. This is precisely the work a QoE firm does professionally, and the reason a first-time buyer should not rely on the seller's own add-back schedule.

How much customer concentration is too much when buying a small business?

A single customer accounting for more than 20% of revenue is the classic red flag, and anything in the 10% to 20% range warrants real scrutiny. The zones advisors and lenders use run roughly like this: under 10% from any one customer is healthy; 10% to 20% is a caution flag that SBA lenders in particular tend to probe; over 20% draws valuation adjustments; and above 25% to 30% the concentration becomes deal-threatening, often producing valuation discounts in the 15% to 30% range, restructured terms such as a larger seller note or earnout, or a walk-away. Concentration matters because the risk transfers to you at close: if the biggest customer leaves after the owner who had the relationship departs, the earnings you paid a multiple on evaporate. Two things to check beyond the raw percentage. First, look for change-of-control clauses in any concentrated customer's contract — a clause that lets the customer terminate on a change of ownership is a specific trap that can trigger the very loss you fear. Second, assess whether the relationship is with the business or with the departing owner personally, because a relationship that walks out the door with the seller was never really an asset you were buying.

The seller keeps sending financials over email — is that a red flag?

It is a workflow problem, not necessarily a character red flag — most sub-$5M sellers are simply disorganized, and the fix is for you, the buyer, to impose structure rather than to walk away. In the $1M to $25M band, the seller often has no data room, no advisor running a formal process, and a filing system that is a mix of email attachments, a shoebox of paper, and one bank-statement folder. Financials arriving as email attachments create three real problems: version chaos (which P&L is current?), no audit trail (your lender and QoE firm cannot see a clean, timestamped record of what was produced when), and security exposure (sensitive financials scattered across inboxes). The move that separates buyers who close from buyers who stall is to stand up the deal workspace yourself: send the seller a structured request list, collect every document into one controlled room, and give your QoE firm, attorney, and SBA lender their own access to pull from the same place. A disorganized seller is not a reason to run — it is a reason for the buyer to own the room. That said, if the seller cannot produce basic records at all — no tax returns, no bank statements, no ability to substantiate revenue — that is a genuine red flag about the quality of the earnings, and a different problem from mere messiness.

What documents should I request during due diligence on a service business?

For a service business, request documents across eight categories, front-loading the financial and customer items because they most often kill deals. A comprehensive small-business diligence list runs 100-plus items, but the core request covers: (1) financial — three years of federal tax returns, monthly P&Ls and balance sheets, the general ledger, bank statements for a proof-of-cash, and the add-back schedule; (2) customer — a revenue-by-customer breakdown to test concentration, top-customer contracts, and retention or churn history; (3) legal and contracts — the corporate formation documents, all material customer and vendor contracts, any litigation history, and leases; (4) tax — federal and state filings and evidence there are no outstanding liens; (5) operations — the org chart, key-employee agreements, and standard operating procedures; (6) HR and benefits — payroll records, the employee census, and benefit plans; (7) assets — equipment lists, the vehicle fleet for a home-services business, and any intellectual property; and (8) corporate — licenses, permits, and insurance. The single highest-value document is the set of federal tax returns, because you reconcile everything the seller tells you back to what they told the IRS. For the full item-by-item checklist, work from a dedicated diligence list rather than improvising, and issue it as one structured request on day one of exclusivity so the clock is not lost chasing documents piecemeal.

Can I realistically close due diligence and SBA financing in a 75-day exclusivity window?

Yes, but only if you run diligence and SBA underwriting in parallel from day one — 75 days is enough for a clean deal and tight for a messy one. The reason it is tight is that SBA underwriting alone typically runs 60 to 90 days, so if you wait until diligence is finished to start the loan, you will blow the window. The workable sequence: in week one, send the full document request list and get your SBA loan application in simultaneously, so the lender's clock starts on day one rather than day thirty. Weeks two through five are active diligence — QoE fieldwork (itself a four-to-six-week process), customer and legal review, and the lender's appraisal and business valuation, all running at once. Weeks six through eight are for negotiating the purchase agreement and clearing lender conditions, and the final stretch is the closing itself. The two things that break the timeline are a disorganized seller who cannot produce documents quickly (which is why the buyer stands up the data room to speed collection) and starting SBA underwriting late. Most $1M to $25M SBA deals close in roughly 90 to 120 days from LOI in practice, so if your exclusivity is a firm 75 days, plan the parallel track from the first day and be ready to request a short extension if the lender's timeline runs long.

Asset purchase vs stock purchase for a small business — which one and why?

For most small acquisitions, an asset purchase is the standard structure, and it is the one a first-time buyer should generally prefer. In an asset deal you buy the specific assets and assume only the specific liabilities you name, which lets you leave unknown and undisclosed liabilities behind with the old entity, and you get a stepped-up tax basis in the assets you acquire — meaning larger future depreciation and amortization deductions. Sellers often prefer a stock sale because it can give them cleaner capital-gains treatment and a fully clean exit, so structure is a genuine negotiation. Two important nuances at this size. First, if you are buying less than 100% of the company with SBA 7(a) financing, SOP 50 10 8 forces a stock purchase — asset structure is no longer permitted for partial changes of ownership. Second, when the seller operates as an S-corporation (most lower-middle-market businesses do), an F-reorganization under IRC Section 368(a)(1)(F) is a common pre-sale restructuring that bridges the fight: it lets the seller sell LLC units for capital-gains treatment while the buyer still gets asset-sale tax treatment with the basis step-up. So the default is an asset purchase, but the right answer depends on ownership percentage, the seller's entity type, and the tax positions on both sides — which is a question for your deal attorney and CPA, not a template.

Related Resources

- Small Business Due Diligence — the item-by-item diligence deep-dive that sits under this operating plan

- Due Diligence Cost Breakdown — what QoE, legal, and the rest of the diligence stack actually cost

- Mergers and Acquisitions Process Guide — the neutral, phase-by-phase corporate and institutional process view

- Due Diligence Data Room Checklist — how to structure the room the buyer builds

- How to Prepare for Due Diligence — the readiness view before the request list goes out

- Due Diligence Red Flags — the fuller catalog of warning signs that kill deals

- Corporate Acquisition Strategy — if you are a company buying repeatedly rather than an individual buying once

- Cross-Border M&A Guide — if the target is overseas and the structuring changes

- Peony Pricing — Free, Business ($30 per admin per month), and Data Room ($52 per admin per month) plans, with unlimited free viewers for your lender, QoE firm, and counsel